Retiring in 2026? Four smart moves to protect your lifestyle

How to start planning for retirement

Everybody has a different starting point in retirement. Whether you’re fortunate enough to retire on your own terms, or if you have to retire earlier or later than expected, a key to retiring with confidence is knowledge.

Over one-quarter of a million Australians will start their retirement in 2026. Many more are looking ahead to the time when they can swap their 9-5 roles for the freedom of retirement. Getting the planning right will be critical for helping people to enjoy the retirement that they deserve.

One of the biggest fears for retirees is whether their savings will last1.

The good news is that there are ways to manage this risk. As we head into 2026, here are the key areas new retirees should focus on.

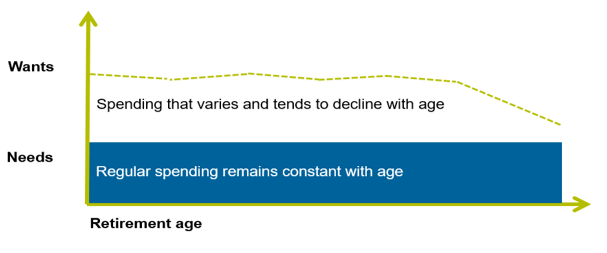

1. Plan to maintain your lifestyle

While some costs may drop in retirement, like commuting or work-related expenses, retirees will likely spend more on travel and activities they’ve been waiting to enjoy.

Over time, the discretionary costs will naturally decline when retirees move into the passive and frail stages. Health costs will increase, but for most, these increases are offset by government subsidies and reduced spending in other areas2.

Understanding how spending evolves over time can help retirees plan with confidence, rather than cutting back too early and unnecessarily limiting their lifestyle.

2. Don’t miss out on your entitlements

Many retirees miss out on Age Pension benefits simply because they don’t understand the rules3. This can be costly and impact the lifestyle you can enjoy in retirement.

The process can take time so remember to apply for the Age Pension before you are 67.

Self-funded retirees might not receive a part pension, but if their income is below $101,105 a year4 they can receive the Commonwealth Seniors Health Card. This dramatically reduces costs for many retirees.

3. Manage risk with longevity

As retirement approaches, many people reduce investment risk to minimise market volatility. While this can help smooth short-term fluctuations in capital, it doesn’t address a more fundamental challenge: how long their income will last.

With Australians now living well into their 80s on average - 81.1 years for men and 85.1 years for women - retirement income often needs to stretch far longer than many people initially plan for5.

Retirees therefore need to strike a careful balance - maintaining enough exposure to growth assets so their capital base and income can keep pace with inflation, while managing one of the greatest retirement fears of all: running out of money.

4. Spend freely while maximising what you leave behind

After more than 30 years of compulsory super, many retirees now have the savings they need to enjoy the lifestyle they’ve worked for. With the right strategies, retirees can make the most of their income today while still planning for tomorrow.

It’s worth exploring options carefully. Retirees can check the lifetime income streams offered by their super fund or speak with a financial adviser about other strategies to help them create their happiest retirement lifestyle.

Some lifetime income streams also include guaranteed death benefits, payable for a period linked to life expectancy (up to a maximum of 27 years). This means beneficiaries may receive a lump sum if the retiree does not live as long as expected.

Importantly, these products can provide a reliable income base, often include inflation protection, and complement the Age Pension - giving retirees the confidence to spend more freely while maintaining financial security throughout retirement.