Aged care reforms and the former home

Aged care reforms and the former home

Download the full article below.

The 1 November 2025 aged care reforms did not change the assessment of the former home after a person moves into residential care. However, decisions involving the former home remain important with the changes to the calculation of ongoing costs. In this month’s article, we will look at the assessment of the former home and the calculation of ongoing costs. We will use case studies to demonstrate the impact on cash flow of keeping and renting or selling the former home.

Assessment of the former home

For Centrelink purposes, the former home will be exempt under the Assets Test for 2 years from the date the person leaves. Where the person is a member of a couple, the former home will be exempt for as long as their spouse continues to live there. If their spouse leaves the former home, it will be exempt for 2 years from the date their spouse leaves. While the former home is exempt, the person and their spouse will be considered homeowners.

For aged care purposes, the value of the former home will be exempt where it is occupied by a protected person. Where the former home is not occupied by a protected person, the home will be assessed up to the home exemption cap (currently $210,5551). A protected person includes:

- spouse or dependent child;

- carer eligible for an income support payment living in the home for the past 2 years; or

- close relative eligible for an income support payment living in the home for the past 5 years.

For Centrelink and aged care purposes, where the former home is rented out, the rental income will be assessed. Assessable income for Centrelink and aged care purposes is the same as assessable income for tax purposes with some exceptions. Certain tax deductions are not allowed for Centrelink and aged care purposes including capital depreciation, construction costs and borrowing costs.

Calculation of ongoing costs

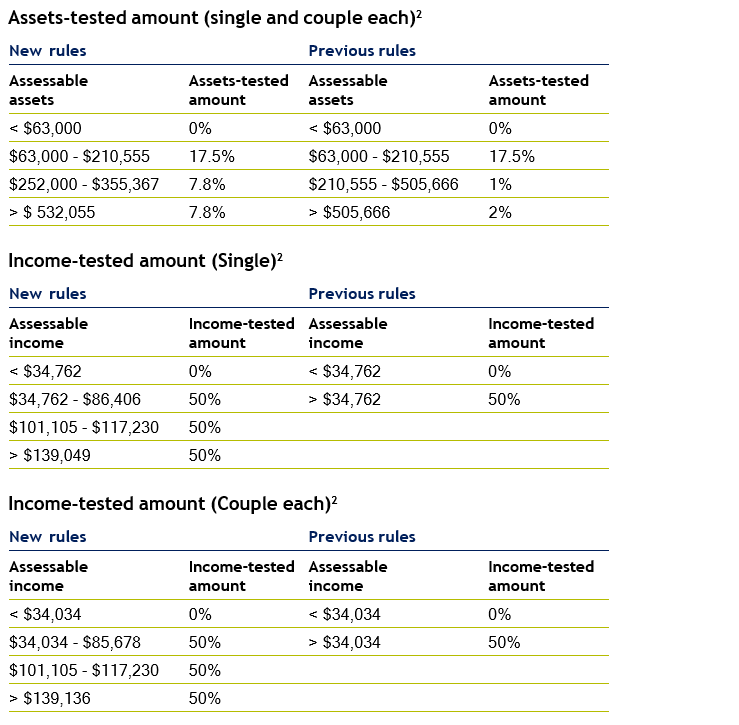

The hotelling contribution (HC) and non-clinical care contribution (NCCC) replaced the means-tested care fee (MTCF) under the new rules. The HC is subject to a daily cap of $22.15 and the NCCC is subject to a daily cap of $105.30 and a lifetime cap of $135,318.692.

The means-tested amount (MTA) continues to be compared to the maximum accommodation supplement (MAS) to determine the HC and NCCC. The assessment of assets and income remains the same however, the calculation of the MTA has changed.

HC = MTA - MAS

NCCC = MTA - (MAS + Maximum HC)

MTA = Assets-tested amount + Income-tested amount

The higher taper rate for the assets-tested amount under the new rules means the HC and NCCC increase at a faster rate than the MTCF as assessable assets increase. The maximum HC and NCCC will be payable when assessable assets reach $1,023,460 whereas the maximum MTCF was payable when assessable assets reached $2,115,1002.

Under the pre-1 November aged care rules, the former home was often sold to pay for accommodation as a lump sum instead of daily payments. This was because the increase in the MTCF was often more than offset by the reduction in daily payments after the home was sold. This was particularly in situations where there were minimal assets outside of the former home to pay the lump sum.

Case study - Minimal assets outside of the former home

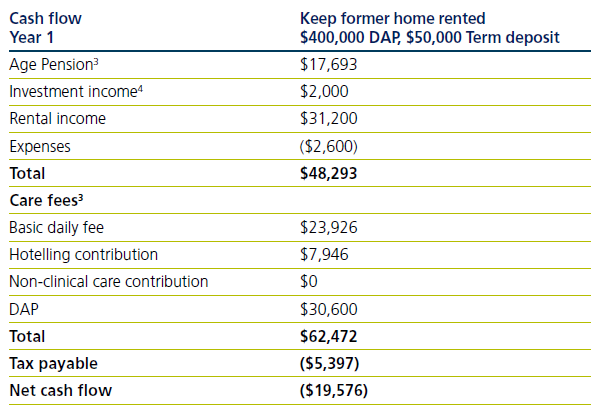

Susan is single, 85 years old and has been approved for residential care and her chosen aged care facility has an advertised accommodation price of $400,000. She lives alone in her home worth $900,000, has $50,000 invested in term deposits and $10,000 of personal contents.

Susan seeks financial advice explaining she would like to keep and rent her former home after she moves into residential care. Her financial adviser determines her cash flow where she pays the entire accommodation price as a DAP and rents out her former home for $600 per week.

Susan will have a cash flow deficit of $19,576 in the first year if she keeps and rents out her former home. Susan also needs to consider the impact on cash flow when her home is no longer exempt under the Assets Test for Centrelink purposes after 2 years.

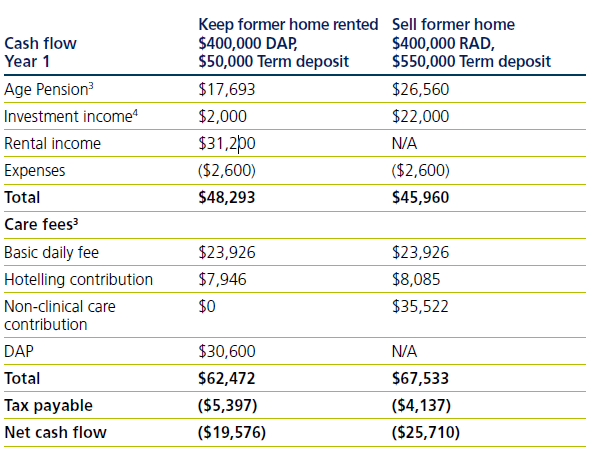

Susan considers selling her former home and paying the entire accommodation price as a RAD with the remaining proceeds invested in term deposits. Her financial adviser compares her cash flow where her former home is sold.

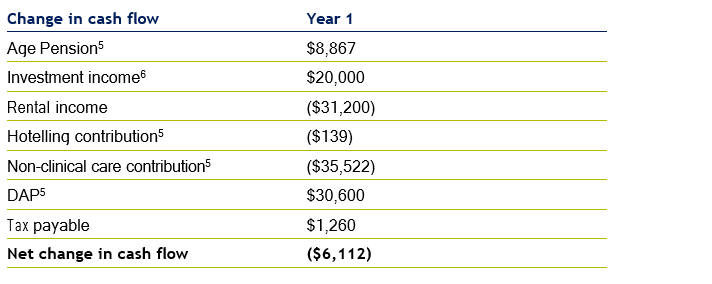

Susan’s cash flow deficit has increased with the non-clinical care contribution becoming payable and without the rental income. This has been offset by the increase in Age Pension, the DAP no longer being payable and the increase in investment income. Although her cash flow deficit has increased, she has more assets which can be drawn down after selling her former home.

The non-clinical care contribution increased because the value of the former home was capped however, the sale proceeds are fully assessed. The Age Pension increased because the rental income was assessed however, the sale proceeds used to pay the RAD are not deemed.

Case study - Significant assets outside of the former home

John is single, 85 years old and has been approved for residential care and his chosen aged care facility has an advertised accommodation price of $550,000. He lives alone in his home worth $1,200,000, has $600,000 invested in term deposits and $10,000 of personal contents.

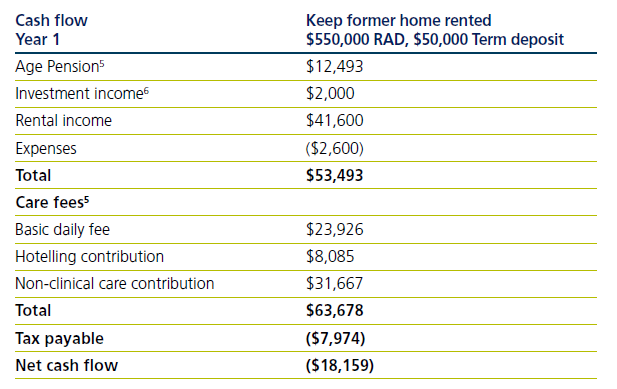

John seeks financial advice explaining he would like to keep and rent his former home after he moves into residential care. His financial adviser determines his cash flow where he pays the entire accommodation price as a RAD and rents out his former home for $800 per week.

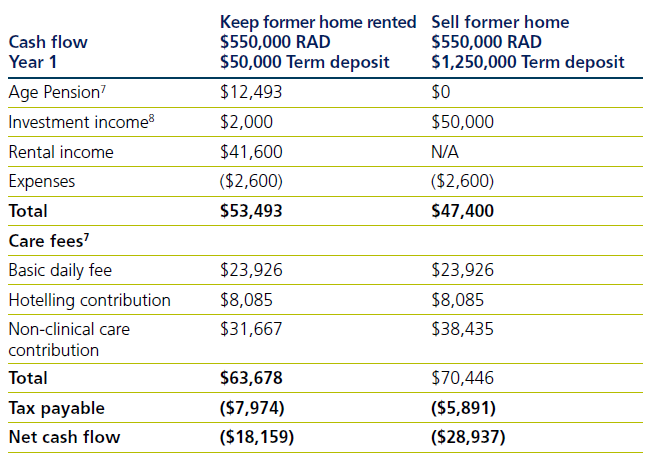

John will have a cash flow deficit of $18,159 in the first year if he keeps and rents out his former home. John also needs to consider the impact on cash flow when his home is no longer exempt under the Assets Test for Centrelink purposes after 2 years.

John considers selling his former home and investing the proceeds in term deposits. His financial adviser compares his cash flow where his former home is sold.

John’s cash flow deficit has increased with the reduction in Age Pension, increase in the non-clinical contribution and without the rental income. This has been offset by the increase in investment income and reduction in tax payable.

The Age Pension decreased because the former home was exempt however, the sale proceeds are fully assessed. The non-clinical care contribution increased because the value of the former home was capped however, the sale proceeds are fully assessed.

Decisions involving the former home remain important under the new rules particularly with the higher taper rate for the assets-tested amount. Regardless if there are minimal assets to pay for accommodation as a lump sum, selling the former home may not improve cash flow.

Where the former home is sold and there are proceeds remaining after accommodation has been paid as lump sum there are investment solutions which can improve cash flow.

Challenger CarePlus - Investment solution for residential aged care

Challenger CarePlus (CarePlus) is a combined lifetime annuity (CarePlus Annuity) and life insurance policy (CarePlus Insurance) which can be purchased by clients who receive or plan to receive Government subsidised aged care services. CarePlus Annuity provides guaranteed regular payments for life and CarePlus Insurance provides a guaranteed death benefit, up to 100% of the amount invested, payable to nominated beneficiaries or the estate in the event of the client’s death9.

CarePlus works effectively with Centrelink and aged care means testing to reduce assessable assets. 60% of the CarePlus Annuity purchase price is assessed until age 85 (with a minimum of 5 years) and then 30% is assessed thereafter. If the client is Age Pension age or over at the time of investment, the greater of the CarePlus Insurance premium and surrender value is assessed.

CarePlus works effectively with tax to reduce assessable income. CarePlus Annuity receives a deductible amount which reduces assessable income from the regular payments. The deductible amount is calculated as the CarePlus Annuity purchase price divided by the client’s life expectancy at the time of investment.

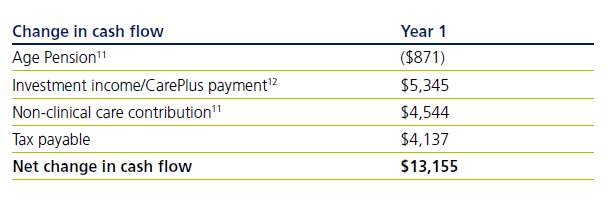

After selling her former home and paying $400,000 as a RAD, Susan has $550,000 invested in term deposits. She considers investing $500,000 in CarePlus with $50,000 remaining in term deposits. CarePlus will make regular payments of $25,345 per annum10 and pay a death benefit of $500,000. Her financial adviser compares her cash flow where $500,000 is invested in CarePlus.

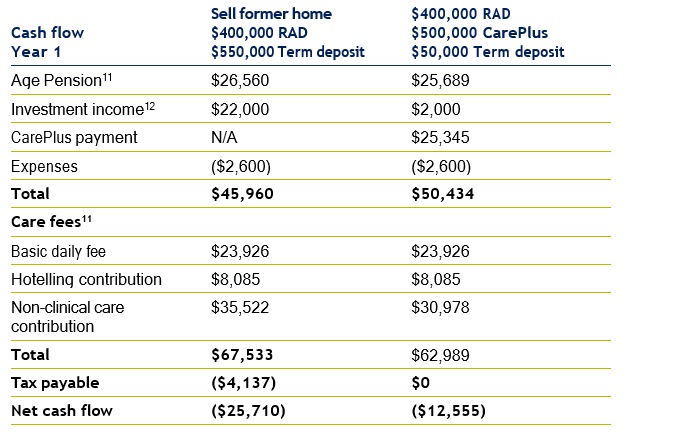

Susan’s cash flow deficit has reduced with the reduction in the non-clinical care contribution and tax no longer being payable. There has been a reduction in Age Pension however, this has been offset by the regular payment from CarePlus.

The non-clinical care contribution decreased because the investment in CarePlus has reduced assessable assets. The tax payable decreased because the regular payment from CarePlus receives a deductible amount which has reduced assessable income.

1. Aged care rates and thresholds as at 1 January 2026.

2. Aged care rates and thresholds as at 1 January 2026.

3. Centrelink and aged care rates and thresholds as at 1 January 2026.

4. Term deposit and bank account assumed interest rate of 4%.

5. Centrelink and aged care rates and thresholds as at 1 January 2026.

6. Term deposit and bank account assumed interest rate of 4%.

7. Centrelink and aged care rates and thresholds as at 1 January 2026.

8. Term deposit and bank account assumed interest rate of 4%.

9. Stamp duty (1.5% of CarePlus Insurance premium) will be deducted from the death benefit for SA residents.

10. Challenger Aged Care Calculator 19/01/2026, 85 year old female, NSW resident, nil adviser fees.

11. Centrelink and aged care rates and thresholds as at 1 January 2026.

12. Term deposit and bank account assumed interest rate of 4%.

Related content

Stay informed

Sign up to our free monthly adviser newsletter, Tech news containing the latest technical articles, economic updates, retirement insights, product news and events.