Australian growth: still looking for the right mix

Subscribe to Macro Musing

To stay up to date on the latest economic insights, subscribe to Macro Musing on LinkedIn.

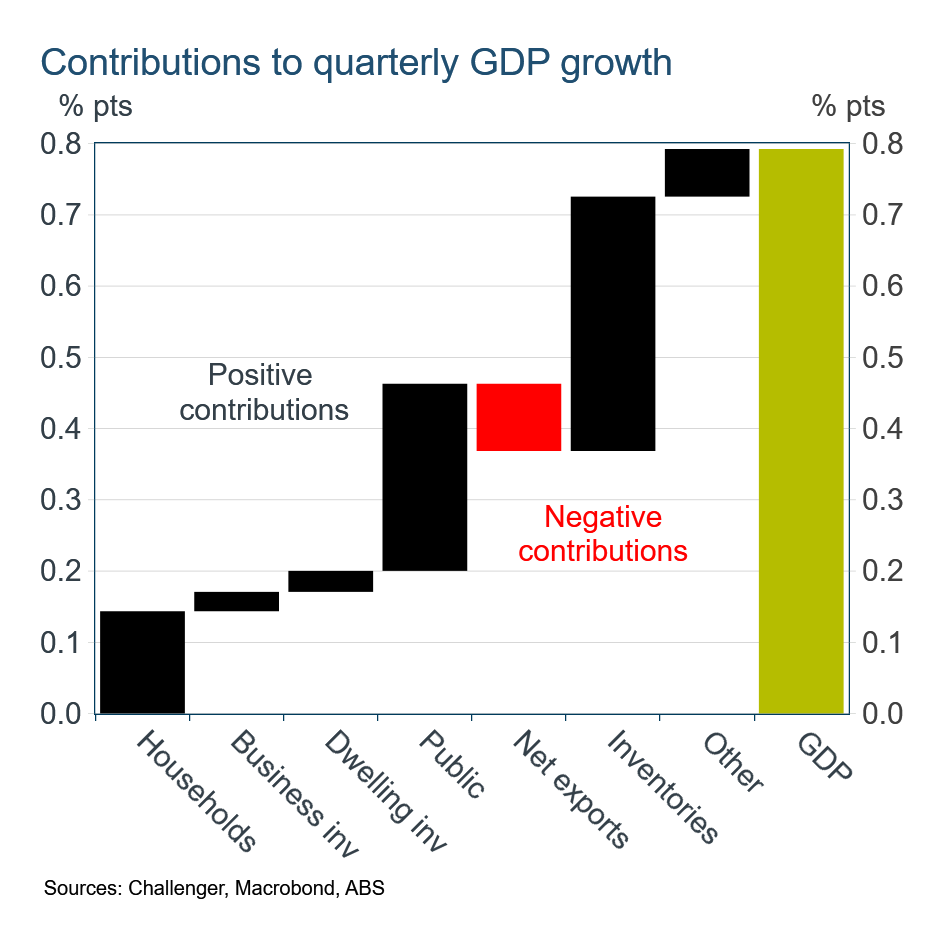

Australian GDP grew 0.8% in the December quarter and 2.6% over the year. While growth was relatively strong, the composition was disappointing with private demand growth easing in the quarter. Household spending increased by only 0.3%, although this was partly suppressed by the measured fall in spending on electricity due to rebates, which increase government spending. Lower spending by households saw a tick-up in their saving rate. Growth in business and dwelling investment was disappointing making little contribution in the quarter.

Government spending made a strong contribution to growth in the quarter, with government consumption and investment both up 0.9%. National defence spending increased 2.1%, with the ABS noting strong defence recruitment over the year. Exports grew 1.4%, as iron ore exports held up despite weaker steel production in China. However, imports growth was stronger at 1.8%, meaning net trade made a small subtraction from growth. Changes in inventories made a large contribution to growth, in part reflecting a rebuilding of coal inventories.

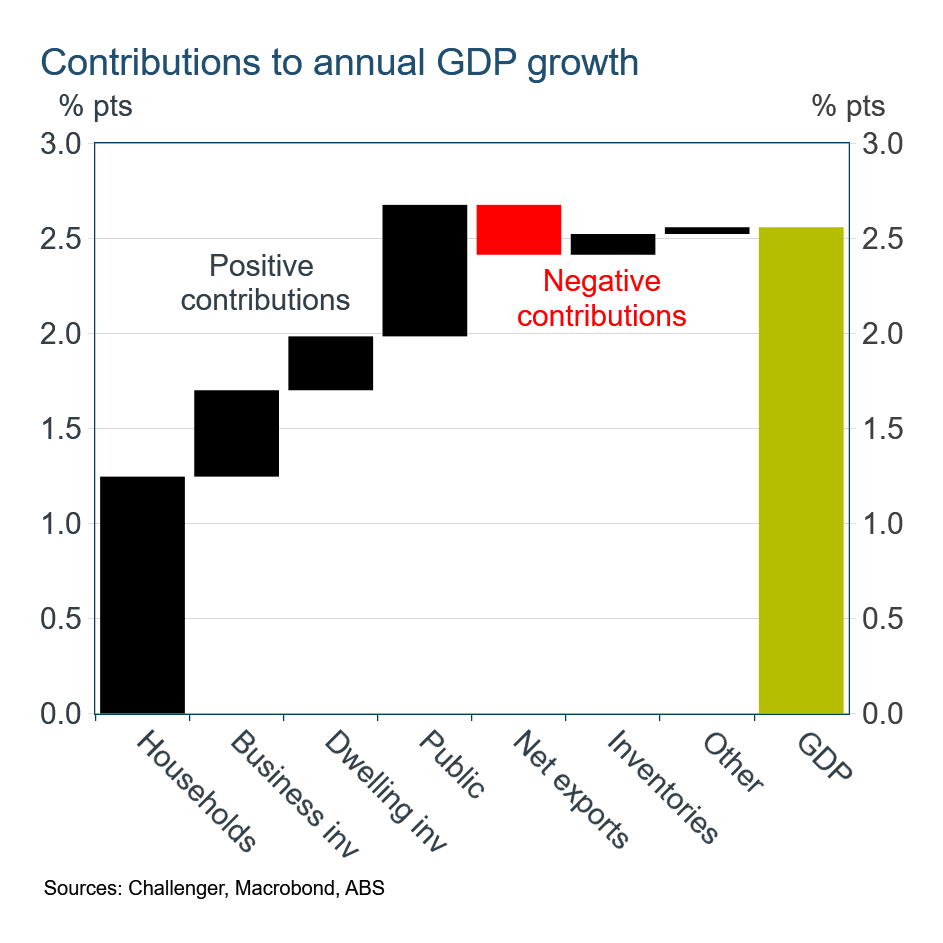

Over the year, the composition of growth was more balanced. However, it also highlights the problem that stronger private demand from household consumption and investment has only been partly offset by slower public spending. The result is growth that appears to exceed the underlying increase in the economy’s productive capacity, and that’s not good for inflation.

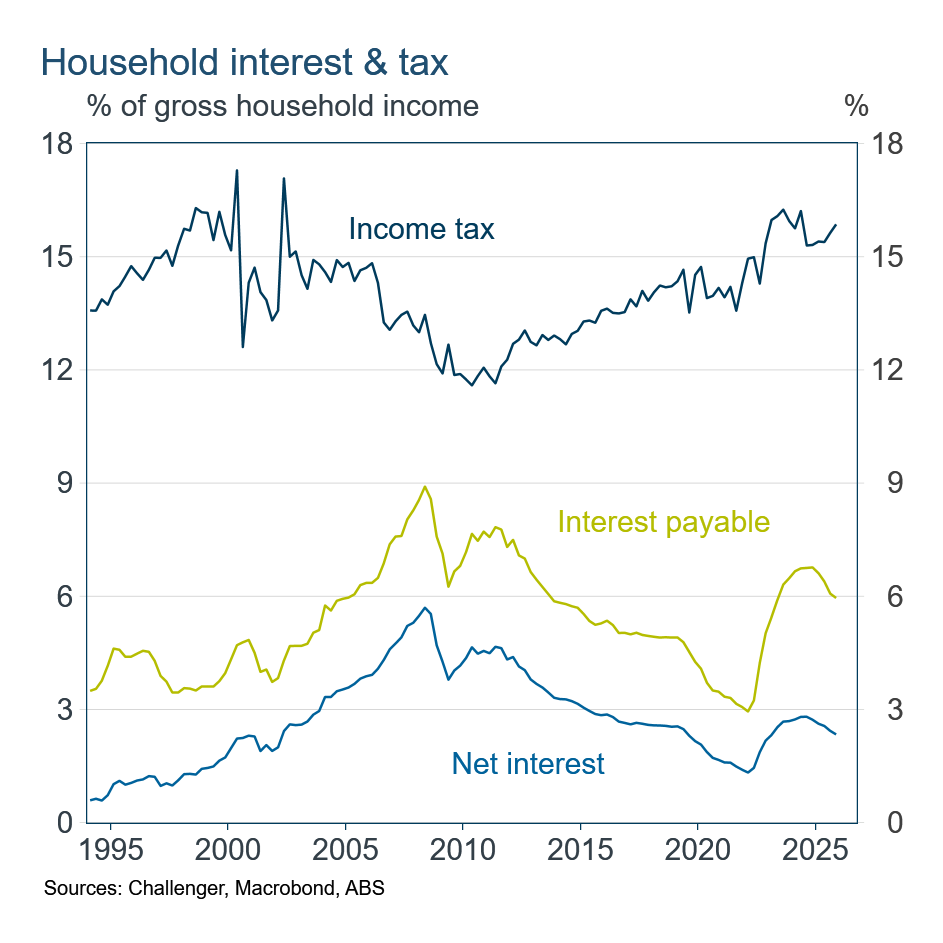

In the last part of 2025, households were still benefiting – in net terms – from the decline in interest rates with the total interest payable falling by more than the total interest received (although it’s important to remember it’s mostly different households who benefit and lose from lower rates). In contrast, income tax continued to increase reflecting labour market strength and bracket creep.

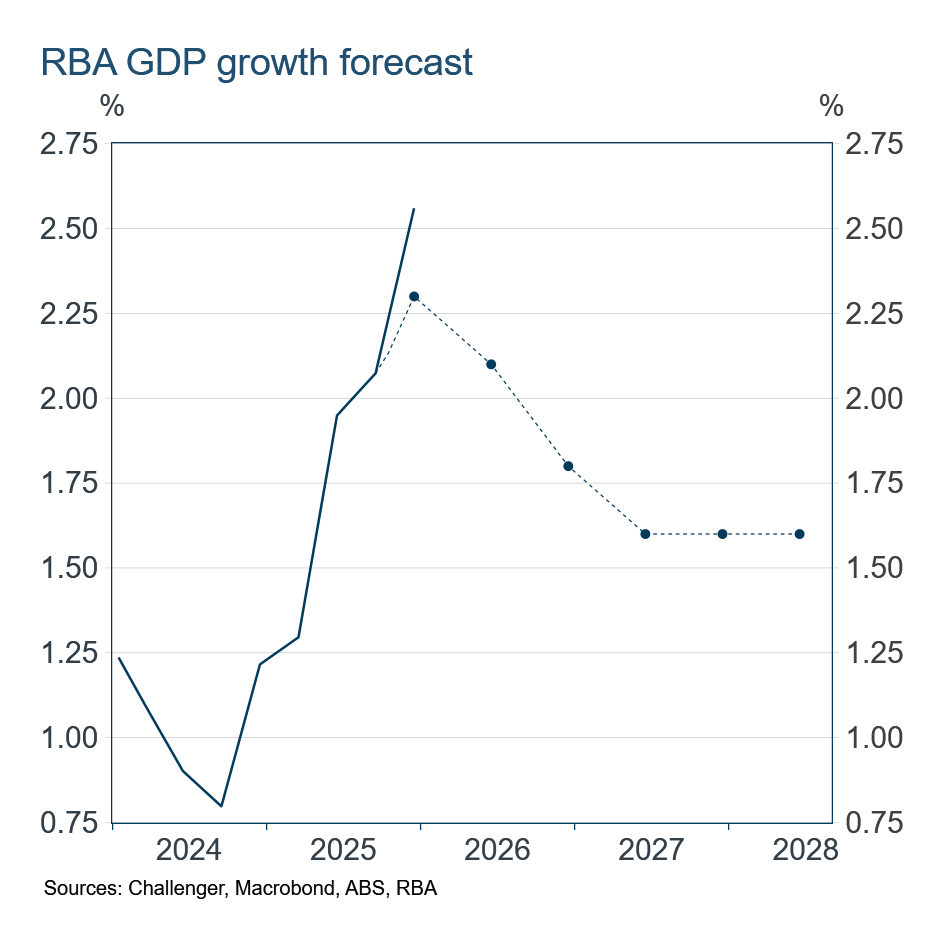

GDP growth for the year of 2.6% was stronger than the RBA’s 2.3% forecast. This suggests that supply capacity was even tighter, and so more inflationary, than the RBA was expecting. However, the good news is that part of that stronger growth over the year came from business investment, where growth of 3.9% exceeded the RBA’s forecast of 2.5%. That might go some way to improving weak business investment which has been a constraint in expanding the economy’s capacity.

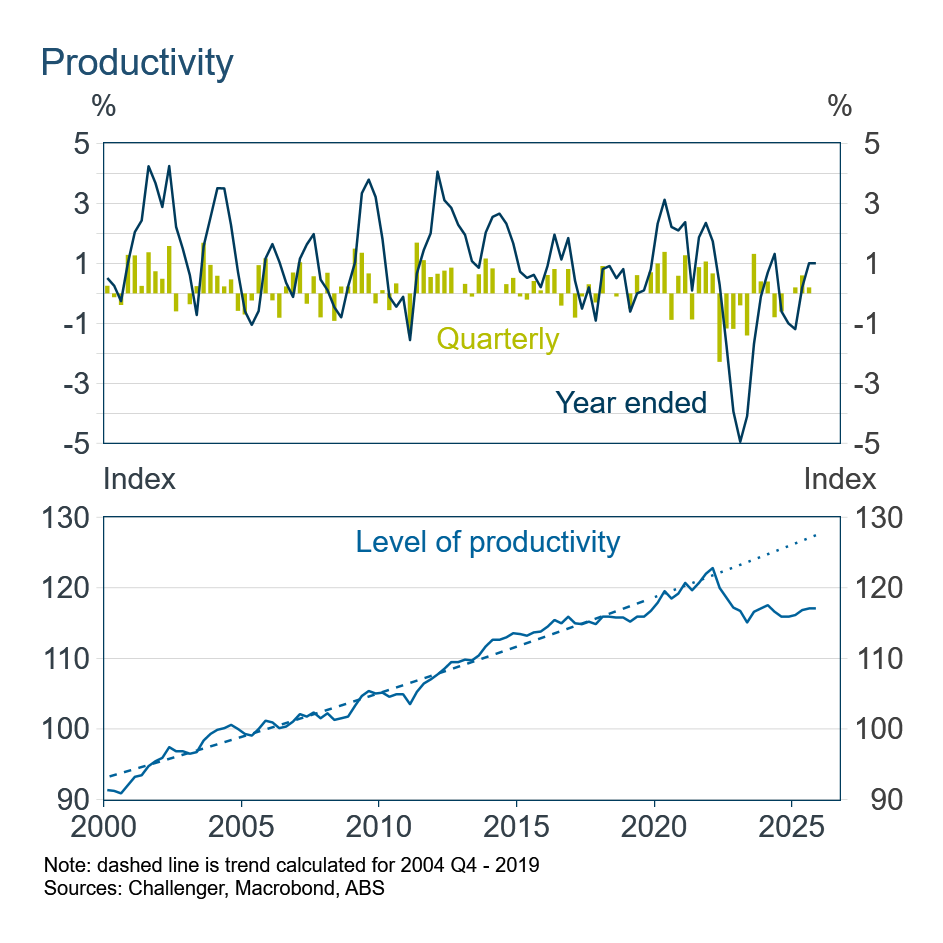

Stronger GDP growth over 2025 pushed productivity growth to 1% over the year, even though there was no growth in productivity in the December quarter. While this growth rate is around the historical average, the level of productivity remains low relative to the trend seen before the pandemic.

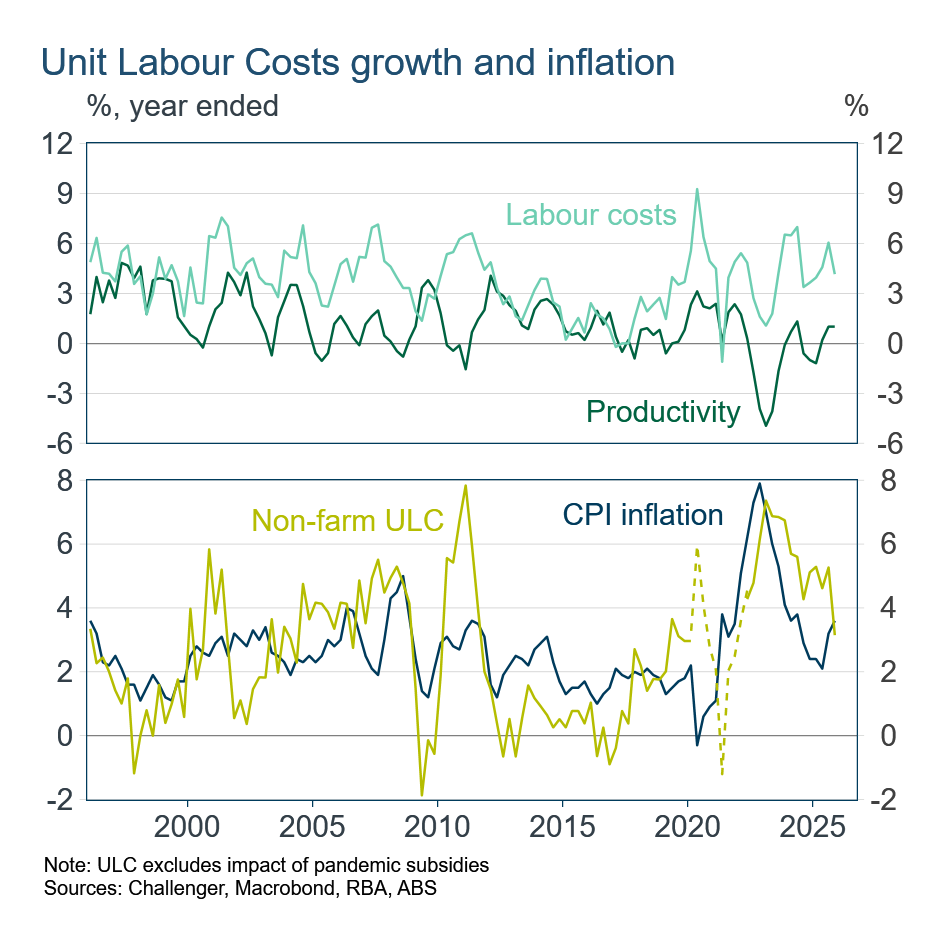

Stable productivity growth, combined with a dip in labour costs, saw a slowing in the crucial measure of ‘unit labour costs’ (the labour costs business face after adjusting for workers’ increased output). Given the importance of unit labour costs in driving inflation, this will give the RBA some comfort.

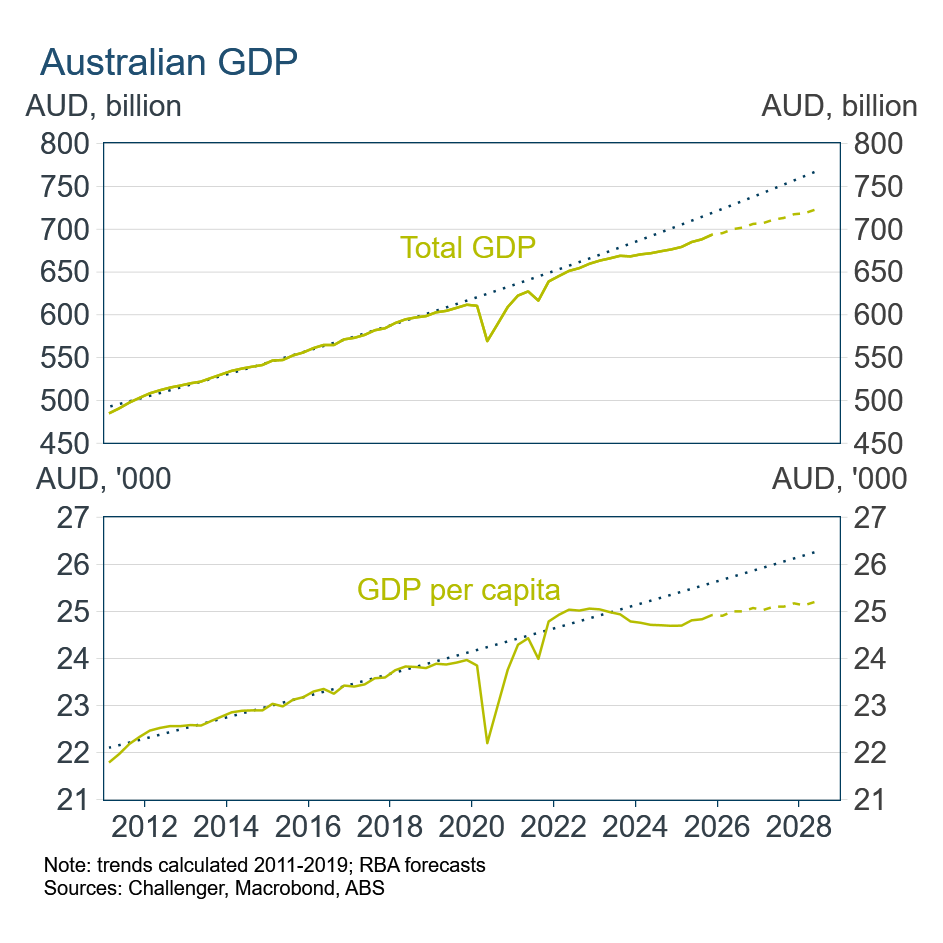

However, while the RBA may take some comfort from productivity growth, the low level of productivity highlights the challenges facing Australia. The total size of the Australian economy, as measured by GDP, and GDP per capita, are well below their pre-pandemic trends and it looks like that’s a gap we’re not going to make up.