Australian inflation remains elevated: CPI details send mixed signals to RBA

Subscribe to Macro Musing

To stay up to date on the latest economic insights, subscribe to Macro Musing on LinkedIn.

CPI inflation was 3.8% for the year to January, and 0.5% in the month. This was a touch higher than expected. On the surface, inflation isn’t slowing and that is a problem for the RBA. However, diving into the details there are some mixed messages.

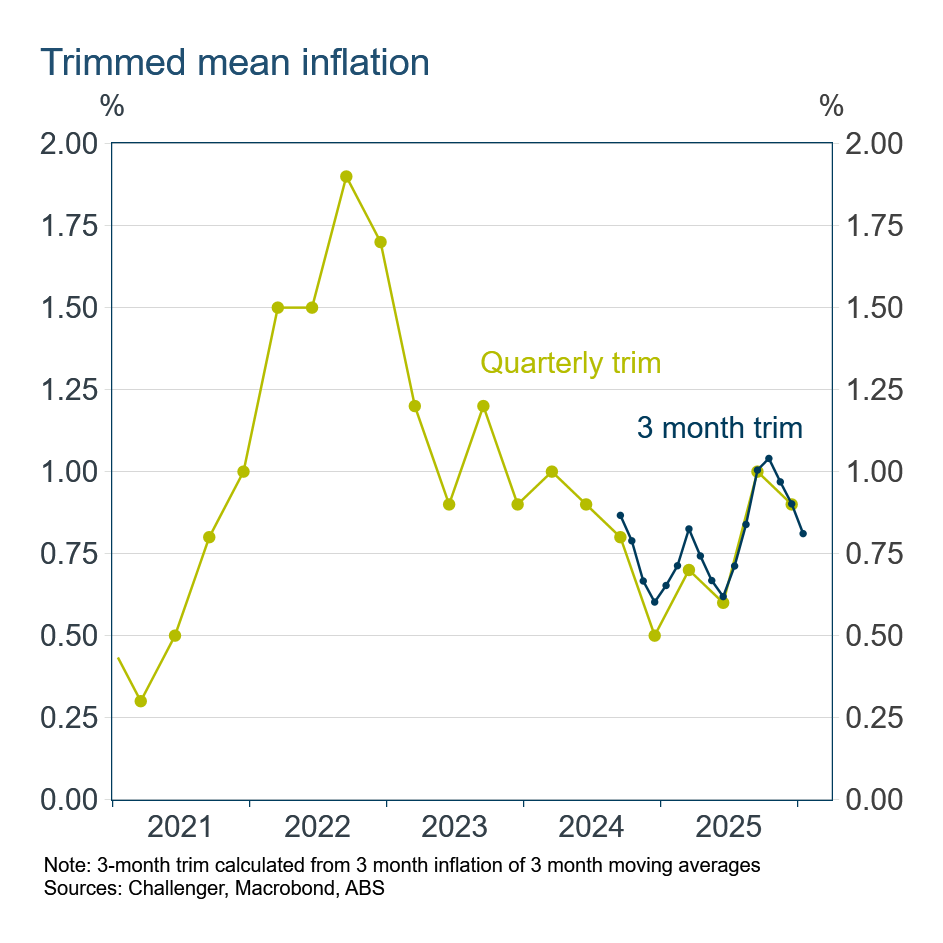

The (slightly) good news is that a measure of trimmed mean inflation slowed. I calculate trimmed mean inflation using the three month movements in prices to be consistent with the long-history of the quarterly trimmed mean inflation, the series the RBA understands well and is central to policy decisions.

This measure of trimmed mean inflation slowed in January to 0.8% from 0.9% in December. This suggests there has been some slowing in underlying price pressure.

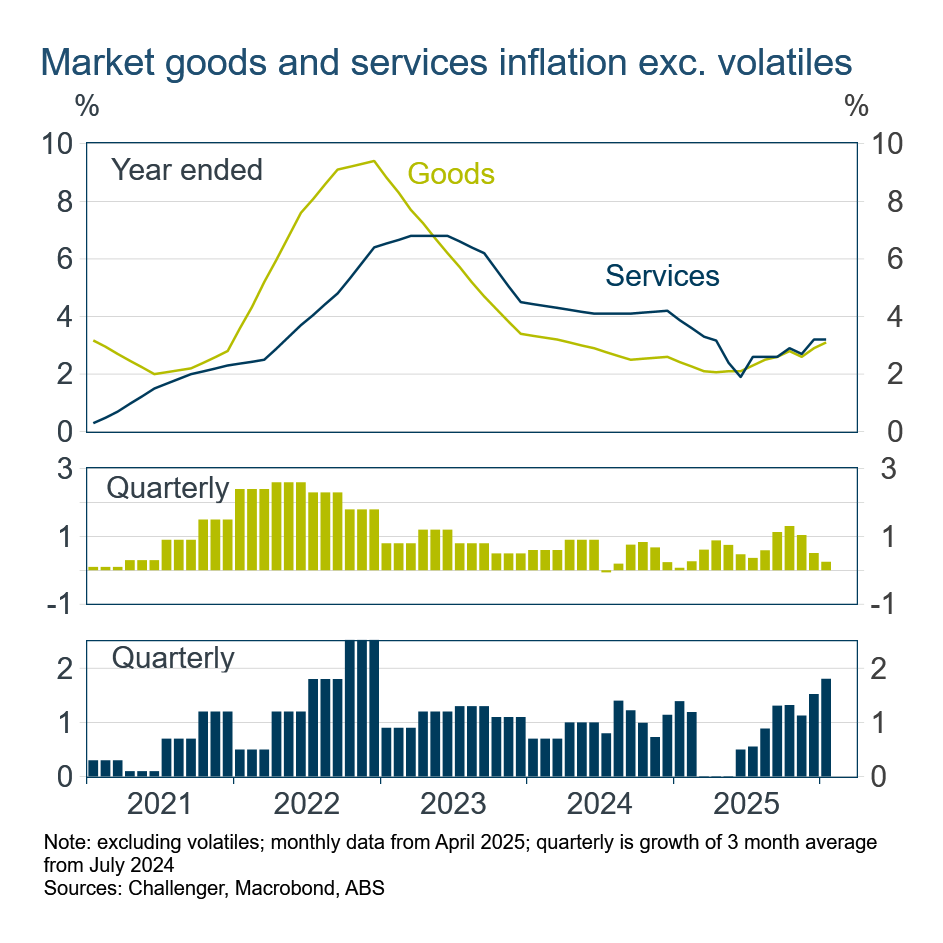

There is also, unfortunately, some less good news in the CPI details. Market services inflation (excluding volatile items) has also been a focus for the RBA. Most services are domestically produced and so their prices reflect domestic price pressures, particularly when items with volatile prices are excluded.

There is a clear upward trend in inflation for market services excluding volatiles. In contrast, the past few months have seen slowing inflation for market goods excluding volatiles.

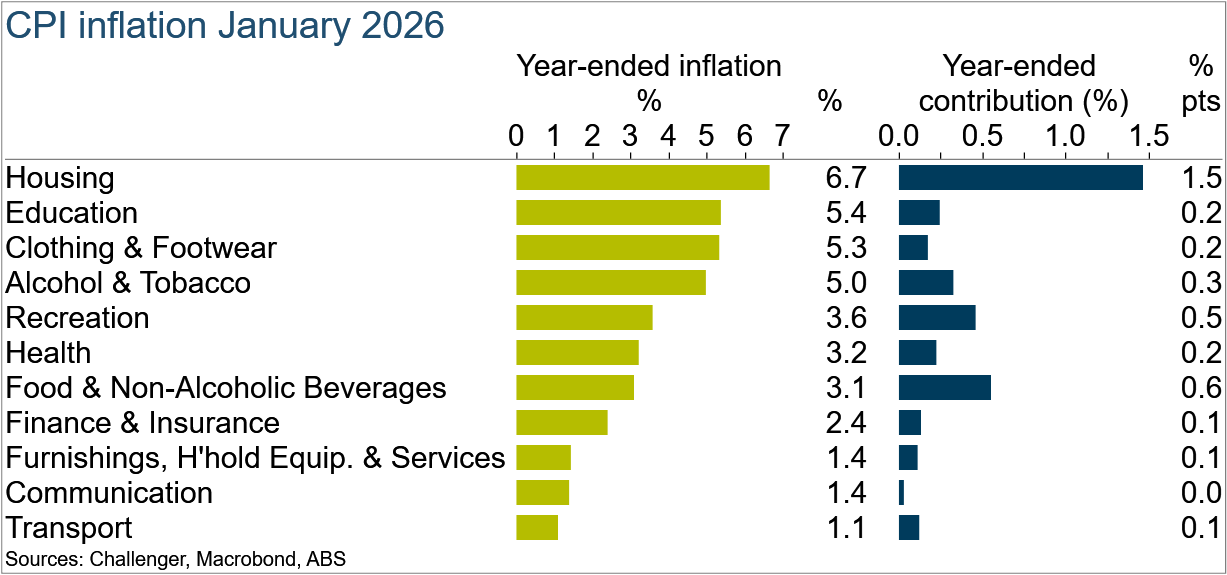

Inflation is above the RBA’s 2.5% target in most categories. The largest contribution to year-ended inflation has come from the housing group.

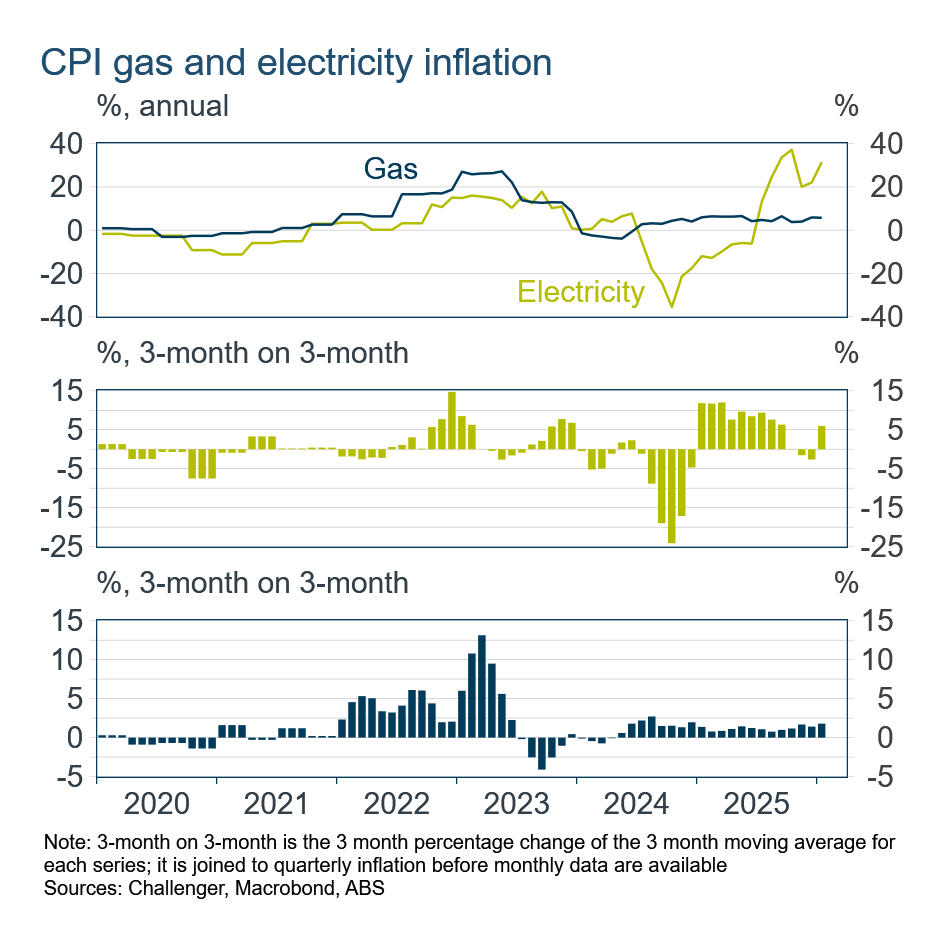

However, the contribution to inflation from housing is somewhat misleading as this group includes electricity which has been significantly impacted by government subsidies over the past couple of years.

Russia’s invasion of Ukraine four years ago precipitated large increases in energy prices. There was some lag in Australia, but gas prices increased strongly through 2022 and early 2023. Gas prices haven’t been subject to rebates, and so after that initial surge, inflation in gas prices has stabilised.

In contrast, the imposition, expansion and expiration of multiple electricity rebates by the national and state governments has caused wild swings in electricity inflation. The good news for economists is that almost all of these rebates have expired and so electricity inflation should be more stable going forward. The RBA will look through the impact on inflation of electricity rebates and other one-off factors.

The other major components of the housing group are rent and the cost of purchasing new dwellings (not including the land). Year-ended rent inflation, which tends to be very persistent, is running at 3.9%. Inflation for new dwelling purchases, which has been impacted by the unwinding of earlier discounts, was 3.5% in January.

All up the January CPI data had some slightly positive news and some less good news that won’t provide a clear direction for the RBA.