Does an investment into a lifetime annuity today impact aged care funding in the future?

Does an investment into a lifetime annuity today impact aged care funding in the future?

Download the full article below.

A partial allocation to a lifetime income stream, such as Challenger’s lifetime annuities, in a retirement portfolio can be a powerful tool to help retirees achieve key income objectives and address key risks in retirement.

However, clients may be concerned about whether an investment into a lifetime income stream can impact their ability to fund aged care costs in the future if the need should arise.

In this month’s article, we use a case study to explore the impacts a lifetime income stream can have on a particular retiree couple’s ability to fund future aged care costs.

Our case study is based on a particular retiree couple’s financial position and objectives. It is also based on certain assumptions around investment returns (detailed at the end of this paper) and that current social security and aged care rules remain unchanged into the future. Different client circumstances, investment return assumptions and changes in legislation can change the outcomes illustrated in this case study.

Brenda and Bob

Brenda and Bob are a 67-year-old couple and have recently retired. They’ve worked hard and are now looking forward to having a whole lot more time to do the things they love. They are active, interested and involved in living their best life from here on in.

Brenda and Bob own their home (worth $1,000,000) and are free of debt. They have $500,000 each in superannuation that they are considering transferring to account-based pensions to start funding their retirement income. Their super (and any future account-based pension) is invested in accordance with their 50/50 growth/defensive risk profile. They also have $50,000 in cash and term deposits and $20,000 worth of personal assets.

Brenda and Bob would like to live comfortably for as long as possible and estimate that $90,000 p.a. would be sufficient to meet this goal. They accept that they can’t achieve this lifestyle forever (nor do they expect to be able to!) but would like peace of mind that at least their essentials of $1,000 per week or $52,000 p.a. can be met for as long as they live.

Strategy 1: Account-based pensions

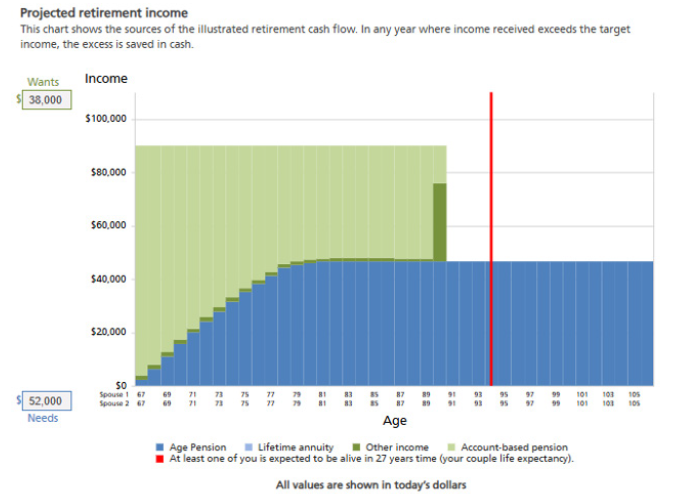

As a starting point, their adviser projects their retirement income based on their initial thoughts of simply rolling over their superannuation to account-based pensions and investing in accordance with their 50/50 risk profile. Their adviser’s analysis of this

strategy, drawing $90,000 p.a. (adjusted for inflation) from all sources, sees their account-based pensions projected to last for approximately 22 years, 5 years before reaching a 67-year-old couple’s life expectancy (red line in the chart below).

At the point where their account-based pensions are eventually depleted, Brenda and Bob would be dependent on the Age Pension alone (current maximum rate for a couple combined is $47,070 p.a.) for all their spending requirements and would not be able to meet their essential expenses of $52,000 p.a. This is shown in the graph below.

Source: Challenger Retirement Illustrator. Assumptions are detailed at the end of this paper.

Strategy 2: Partial allocation to a lifetime annuity

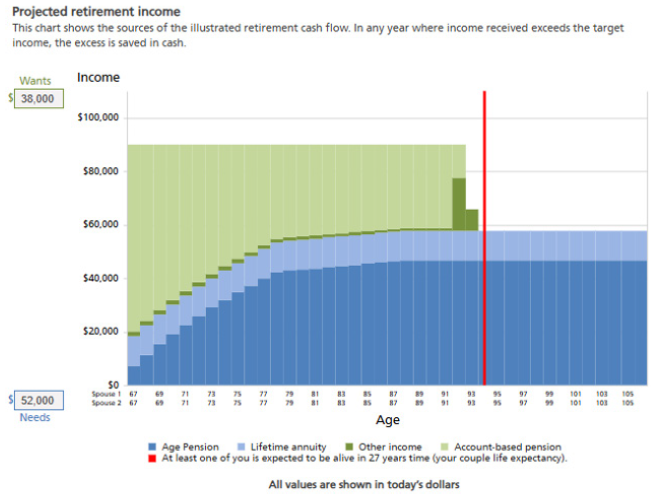

To provide Brenda and Bob the peace of mind they desire around meeting their essential spending needs for life, their adviser recommends a 20% allocation to a Challenger lifetime annuity ($100,000 each from their respective superannuation savings with each other as a reversionary) providing total lifetime income of $11,056 p.a. indexed to CPI. Their adviser views the lifetime annuity as a defensive asset and recommends rebalancing their remaining account-based pensions to a 63%/37% growth/defensive split.

Their adviser’s analysis of this strategy sees their remaining account-based pensions projected to last 24 years, 2 years longer than their initial strategy, allowing them to enjoy their desired retirement lifestyle for longer.

At the point where their account-based pensions are depleted, they will have $11,056 p.a. (in today’s dollars) from their two lifetime annuities in addition to their Age Pension entitlement ($46,7891 p.a. in today’s dollars) to meet their $52,000 p.a. essentials. This is shown in the graph below.

Source: Challenger Retirement Illustrator. Assumptions are detailed at the end of this paper.

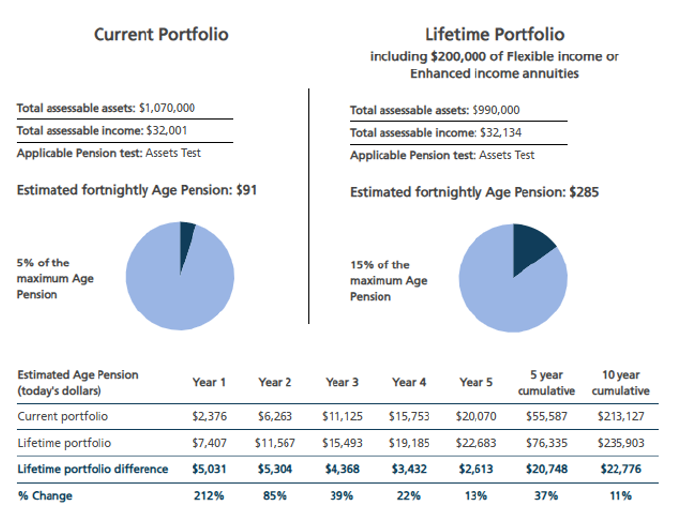

In addition to helping Brenda and Bob achieve peace of mind around meeting their essential expenses and increasing the longevity of the account-based pensions, the adviser also highlights that the Challenger lifetime annuity will also increase their Age Pension entitlement due to the annuity’s concessional assets test assessment2.

Brenda and Bob’s Age Pension entitlement is expected to increase by $5,031 p.a. in the first year and $22,776 over 10 years, highlighted in the chart and table below.

Source: Challenger Retirement Illustrator. Assumptions are detailed at the end of this paper.

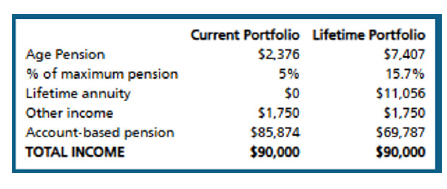

A comparison of Brenda and Bob’s cashflow in the first year is summarised in the table below. ‘Current Portfolio’ represents strategy 1 with retirement savings invested in account-based pensions only and ‘Lifetime Portfolio’ representing strategy 2 where 20% of their retirement savings is invested in a Challenger lifetime annuity:

Brenda and Bob are approved for Government funding under the Support at Home Program

Fast forward 21 years, Brenda and Bob are now age 88 and they feel content. They have enjoyed their retirement and have achieved most of the things they had set out to achieve.

Unfortunately, Bob’s health has deteriorated and although Brenda is able to support Bob with certain things, she is also frail and needs help with other tasks around the home.

After completing their aged care assessment, they have been allocated a classification 5 for Government funding under the Support at Home program. Classification 5 provides government funding of $39,697 p.a. per person (rounded to $40,000 p.a. for illustrative purposes) that Brenda and Bob can each use towards services to assist them at home.

Their Service Agreement with their chosen provider shows they each intend to access services from the following categories:

- $10,000 towards clinical supports (including care management)

- $15,000 towards independence services

- $15,000 towards everyday living services

While the Government provides funding, Brenda and Bob will need to contribute towards these costs based on their assessable income and assets.

Brenda and Bob’s financial position at age 88

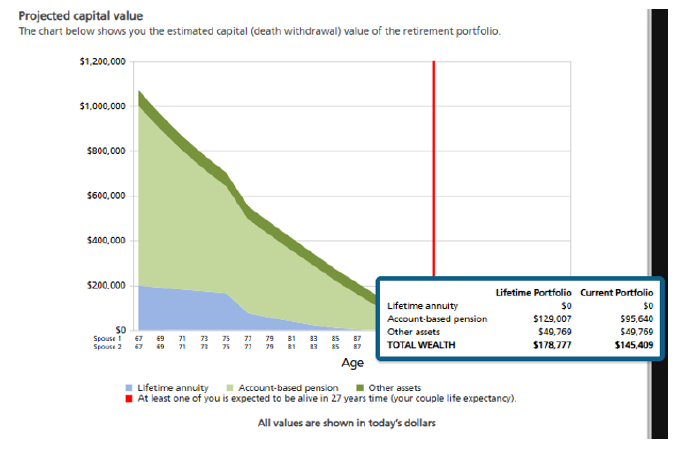

Using projected capital values from the Retirement Illustrator (see chart below), Brenda and Bob’s projected account-based pension balances (in today’s dollars) at age 88 is expected to be $129,007 where they incorporate lifetime annuities into their retirement portfolios, and $95,640 if they simply invested in account-based pensions. Assuming their personal assets remain at $20,000 in real terms, their savings in the bank is expected to be $29,769 in today’s dollars (total other assets of $49,769 less $20,000).

Where Brenda and Bob invest 20% ($200,000 combined) of their portfolio into a Challenger lifetime annuity, their annuity’s assessable asset and income value for social security and aged care purposes would be $60,000 (30% of $200,000 from age 85) or $35,723 in today’s dollars, and $6,634 p.a. (60% of $11,056 p.a.) respectively.

Source: Challenger Retirement Illustrator. Assumptions are detailed at the end of this paper.

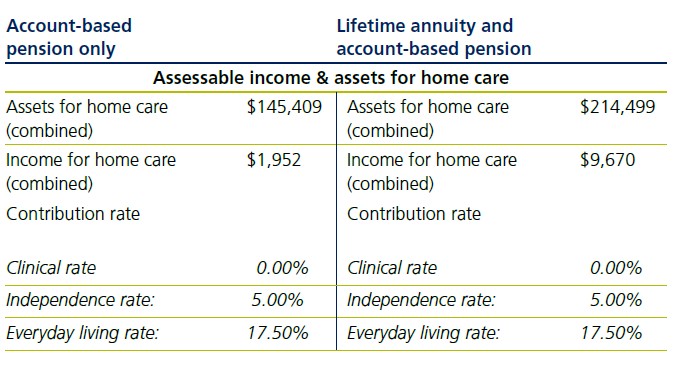

A comparison of total assessable income and assets for social security and aged care along with calculated contribution rates for their Support at Home funding is summarised in the below table.

The strategy incorporating a lifetime annuity resulted in higher assessable assets and income for social security and aged care means testing due to higher account-based pension balances, an ongoing 30% asset test assessment for the annuity, and

higher income received from the lifetime annuity. Despite higher assessable assets and income, it did not impact their Age Pension entitlement and aged care costs compared to the scenario where they don’t invest in lifetime annuities.

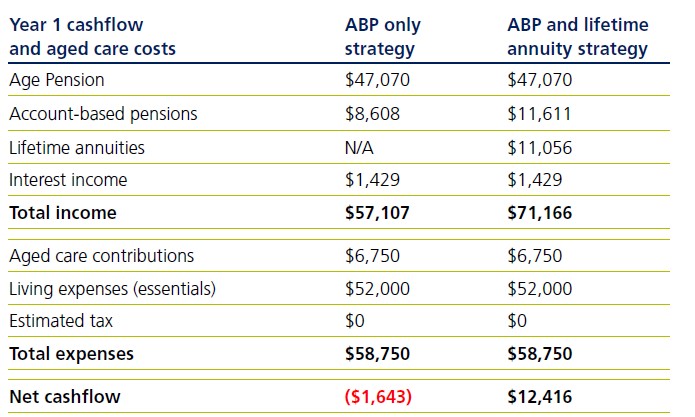

As the annuities provide Brenda and Bob with income for life, they have significantly higher cash flow to help with funding aged care costs - $11,056 p.a. additional income from the annuities in today’s dollars.

A comparison of Brenda and Bob’s year 1 cash flow and aged care costs with and without a lifetime annuity is expected to be as follows:

Source: Challenger Aged Care Calculator assuming minimum pension payments from the account-based pensions and 4.8% interest on savings.

Brenda enters residential aged care

Unfortunately, Bob shortly passes away unexpectedly. Without Bob, Brenda is unable to cope at home by herself and considers entering residential aged care. Upon receiving an approval for residential care, Brenda finds a suitable aged care home and

agrees to a price of $600,000 for her room.

Brenda decides to sell their former home ($1,000,000) to pay for her room, investing the remaining sale proceeds in term deposits earning 4.8% interest.

After paying for her accommodation, she has $429,769 in savings and term deposits as well her and Bob’s income streams (as a reversionary beneficiary). She also has other miscellaneous expenses outside of her aged care fees of $100 per week.

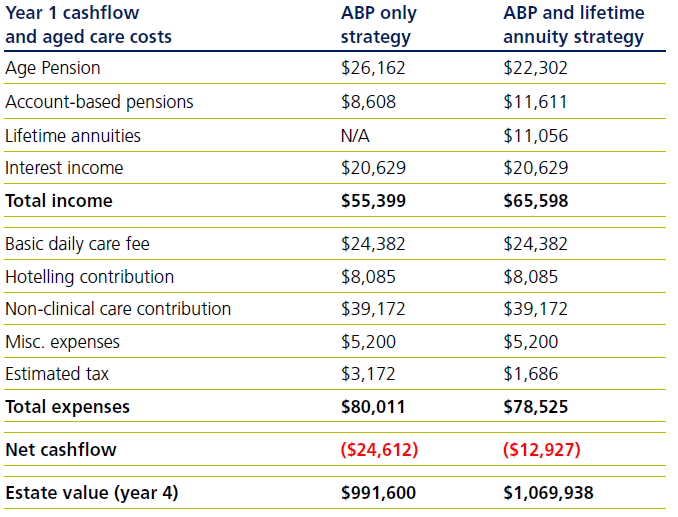

A comparison of Brenda’s year 1 cash flow and aged care costs with and without a lifetime income stream is expected to be as follows:

Source: Challenger Aged Care Calculator assuming minimum pension payments from the account-based pensions and 4.8% interest on savings.

Brenda’s Age Pension entitlement is lower under the lifetime annuity scenario due to her being a single homeowner and income test sensitive due to additional income from the annuity being assessed. However, the lower Age Pension entitlement is more than offset by the reduction in tax (lower taxable income due to lower Age Pension) and an additional source of income from the annuity, resulting in $11,685 p.a. higher net cash flow in year 1.

Brenda would need to draw down from her $429,769 in savings to fund her expected cash flow shortfall under each scenario, however, after four years, Brenda would reach the non-clinical care contribution lifetime cap and would not be required to pay this cost for the remainder of her time in care. Her cash flow position would no longer be in deficit at that time.

However, due to lower capital drawdowns from her savings, Brenda’s estate value at the end of year 4 is $78,338 higher under the lifetime annuity scenario.

Improving outcomes further for Brenda

Brenda can further improve her financial position in residential care by considering investing some of her $429,769 in savings into Challenger CarePlus. CarePlus is designed specifically for clients like Brenda – those who are residing in residential

aged care or have been approved for Government funded aged care services.

CarePlus provides a competitive payment rate for life that can help Brenda better fund aged care costs and pays the entire3 investment amount back to her nominated beneficiary or estate on death. Regular payments from CarePlus are also tax effective,

as they are subject to a deductible amount that help reduce the amount assessable for tax purposes.

Additionally, the concessional assessment of CarePlus under the social security and aged care means tests can help reduce Brenda’s aged care costs and increase her Age Pension entitlements.

For more information on CarePlus and how it may improve outcomes for clients like Brenda, please speak to your Business Development Manager.

Challenger Retirement Illustrator assumptions: Challenger annuity rates are as at 28 May 2026. Centrelink rates and thresholds are as at 20 March 2026. Projections were performed on Challenger’s Retirement illustrator based on 67 year old male/female homeowner couple. $500,000 each available for investment via account-based pension and partial (20%) allocation to a Challenger Liquid Lifetime annuity with CPI indexation. Superannuation asset allocation of 50% growth/50% defensive with assumed returns of 4% p.a. for defensive assets and 7.5% p.a. for growth assets before fees. $50,000 cash and term deposits earning 3.5% p.a. interest. Personal assets of $20,000. $90,000 p.a. desired

income. Amounts shown are in today’s dollars and CPI assumed to be 2.5% p.a. See Challenger Retirement Illustrator for all assumptions.

Challenger Aged Care Calculator assumptions: Social security and aged care rates are as at 20 March 2026. Savings and term deposit interest assumed to be 4.8% and account-based pensions assumed to earn 6% p.a. Pension payments from account-based pensions are assumed to be at the SIS minimum level.

1 The energy supplement is not subject to indexation and as such it’s real value declines over time.

2 60% of their investment amount is assessed until they turn age 85 and then 30% is assessed thereafter.

3 Stamp duty of 1.5% is deducted for residents of South Australia

The information in this article is current as at 1 June 2026 unless otherwise specified and is provided by Challenger Life Company Limited ABN 44 072 486 938, AFSL 234670 (Challenger, our, we), the issuer of the Challenger annuities (Annuity(ies)), the issuer of CarePlus Annuity and CarePlus Insurance, together referred to as Challenger CarePlus and Challenger Retirement and Investment Services Limited ABN 80 115 534 453, AFSL 295642 (CRISL). The information in this article is general information and is intended solely for licensed financial advisers or authorised representatives of licensed financial advisers, and is provided to them on a confidential basis. It is not intended to constitute financial product advice. This information must not be distributed, delivered, disclosed or otherwise disseminated to any investor, without our express prior approval. Investors should consider the applicable Annuity Target Market Determination (TMD) and Product Disclosure Statement (PDS) available at challenger.com.au and the appropriateness of the applicable product to their circumstances before making an investment decision. This information has been prepared without taking into account any person’s objectives, financial situation or needs. Neither Challenger and/or CRISL, nor any of its officers or employees, are a registered tax agent or a registered tax (financial) adviser under the Tax Agent Services Act 2009 (Cth) and none of them is licensed or authorised to provide tax or social security advice. Before acting, we strongly recommend that prospective investors obtain financial product advice, as well as taxation and applicable social security advice, from qualified professional advisers who are able to take into account the investor’s individual circumstances. Each person should, therefore, consider its appropriateness having regard to these matters and the information in the TMD and PDS for the applicable Annuity before deciding whether to acquire or continue to hold the product. A copy of the TMD and PDS is available at challenger.com.au or by contacting our Adviser Services Team on 13 35 66. Any examples shown in this article are for illustrative purposes only and are not a prediction or guarantee of any particular outcome. Age Pension benefits described in this article will not apply to all individuals. Age Pension outcomes depend on an individual (or couple’s) personal circumstances and may change over time. This article may include statements of opinion, forward looking statements, forecasts or predictions based on current expectations about future events and results. Actual results may be materially different from those shown. This is because outcomes reflect the assumptions made and may be affected by known or unknown risks and uncertainties that are not able to be presently identified. Challenger and CRISL relied on publicly available information and sources believed to be reliable, however, the information has not been independently verified by Challenger and CRISL. While due care and attention has been exercised in the preparation of this information, Challenger and CRISL gives no representation or warranty (express or implied) as to its accuracy, completeness or reliability. The information presented in this article is not intended to be a complete statement or summary of the matters to which reference is made in this article. To the maximum extent permissible under law, neither Challenger, CRISL, nor its related entities, nor any of their directors, employees or agents, accept any liability for any loss or damage in connection with the use of or reliance on all or part of, or any omission inadequacy or inaccuracy in, the information in this article.

Related content

Stay informed

Sign up to our free monthly adviser newsletter, Tech news containing the latest technical articles, economic updates, retirement insights, product news and events.