A Sobering Outlook: Higher Rates, Higher Inflation, Slower Growth

Subscribe to Macro Musing

To stay up to date on the latest economic insights, subscribe to Macro Musing on LinkedIn.

Given the pick-up in inflation in the second half of 2025 the RBA increased the cash rate by 25 basis points this week, just 175 days after cutting the rate in August last year. This was a quick turn-around in policy, just pipped for the fastest switch from cutting to hiking of 154 days in May 2002.

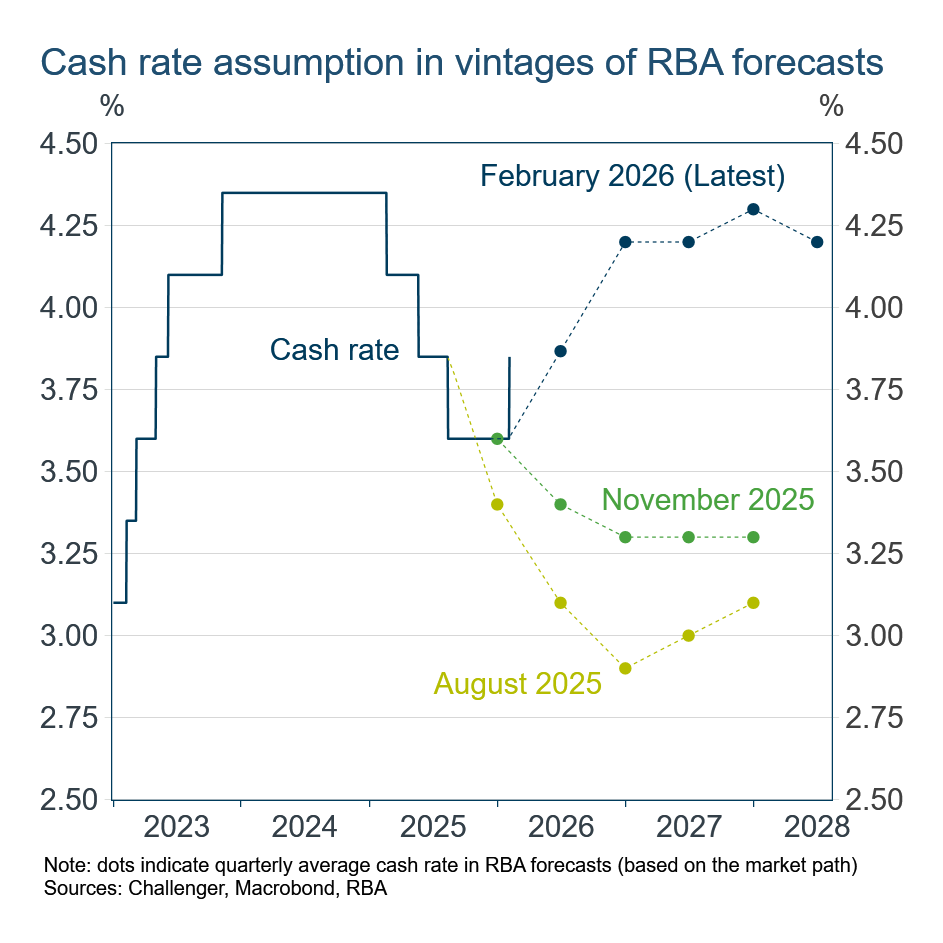

High and persistent inflation led to a significant upward revision in expected interest rates. The RBA bases its forecasts on a cash rate path derived from market expectations. In August, the path used by the RBA had the cash rate being cut to 2.9% by the end of this year. In its latest forecasts the RBA used a path for the cash rate that has it rising to around 4.25%.

You might expect using a cash rate that is 130 basis points higher than in August to have a significant impact on the forecasts. On that front you may be surprised, or disappointed.

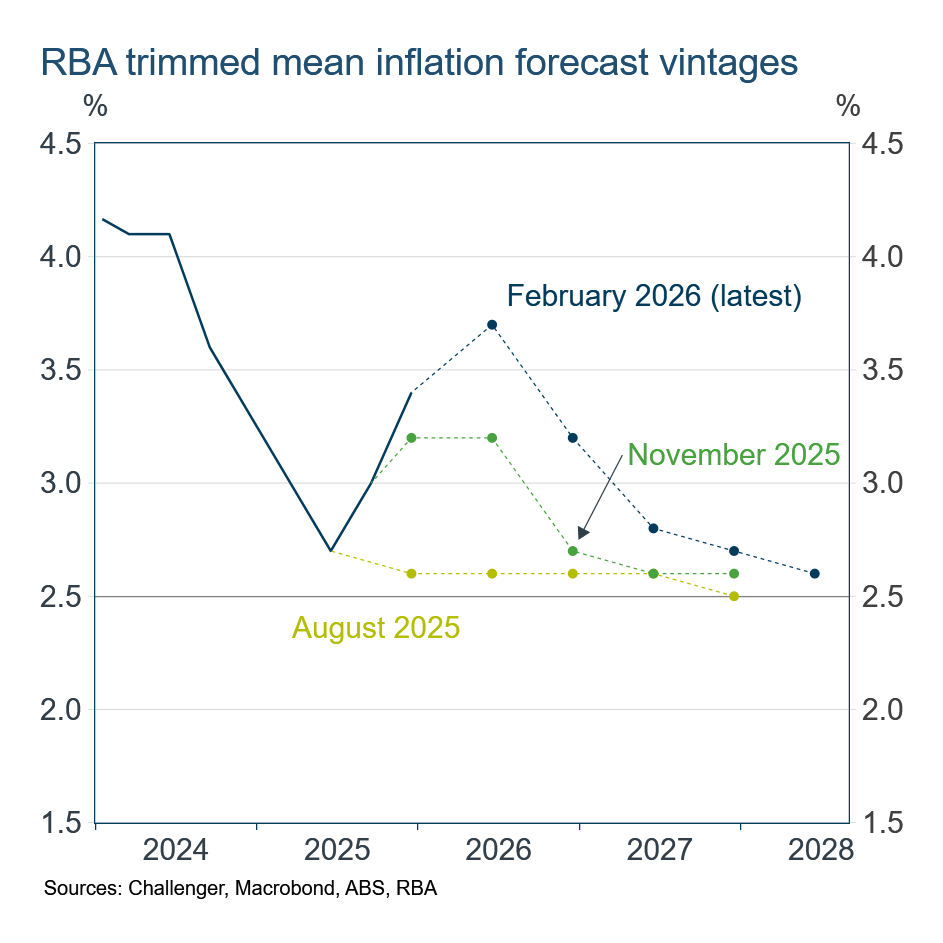

Forecasts for the RBA’s preferred measure of inflation, trimmed mean, have been revised significantly higher. That is exactly why the RBA is increasing the cash rate. In August last year the RBA expected inflation to be 2.6% by now, whereas now the RBA expects inflation to peak at 3.7% in the middle of this year. This is a very substantial upward revision to forecast inflation, highlighting that the inflation pressures in the second half of 2025 took the RBA by surprise. If it weren’t for the higher cash rate used to produce the forecasts, the peak in inflation would have been a little bit higher, but probably still less than 4%.

Based on a core RBA model, a 100 basis point higher cash rate reduces the level of GDP by around 0.8%, raising the unemployment rate by 0.3 percentage points and lowering trimmed mean inflation by just 0.1 percentage points. Different models show a slightly smaller or larger sensitivity of inflation to the cash rate, but the impact is fairly moderate in all.

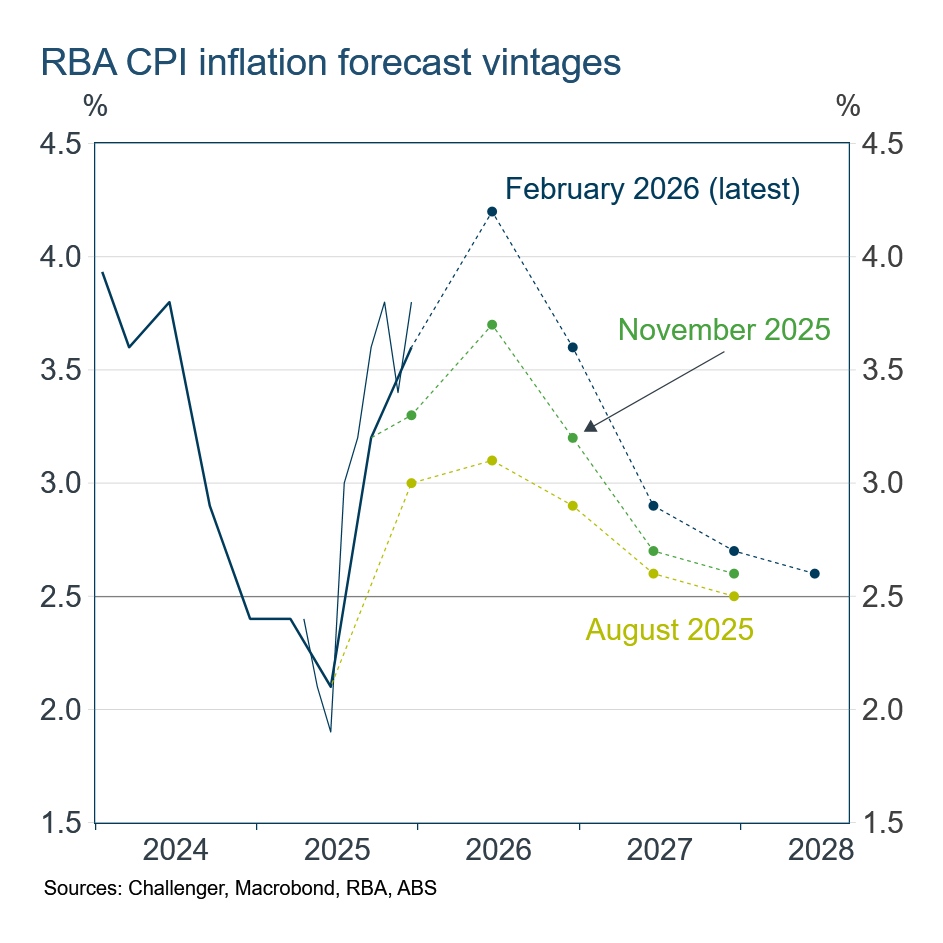

The upward revision to CPI (headline) inflation was similar. The RBA had expected CPI inflation to rise, largely reflecting the expiration of energy subsidies. Higher inflation will reduce households’ real incomes, making us all feel a bit less well-off and reducing spending.

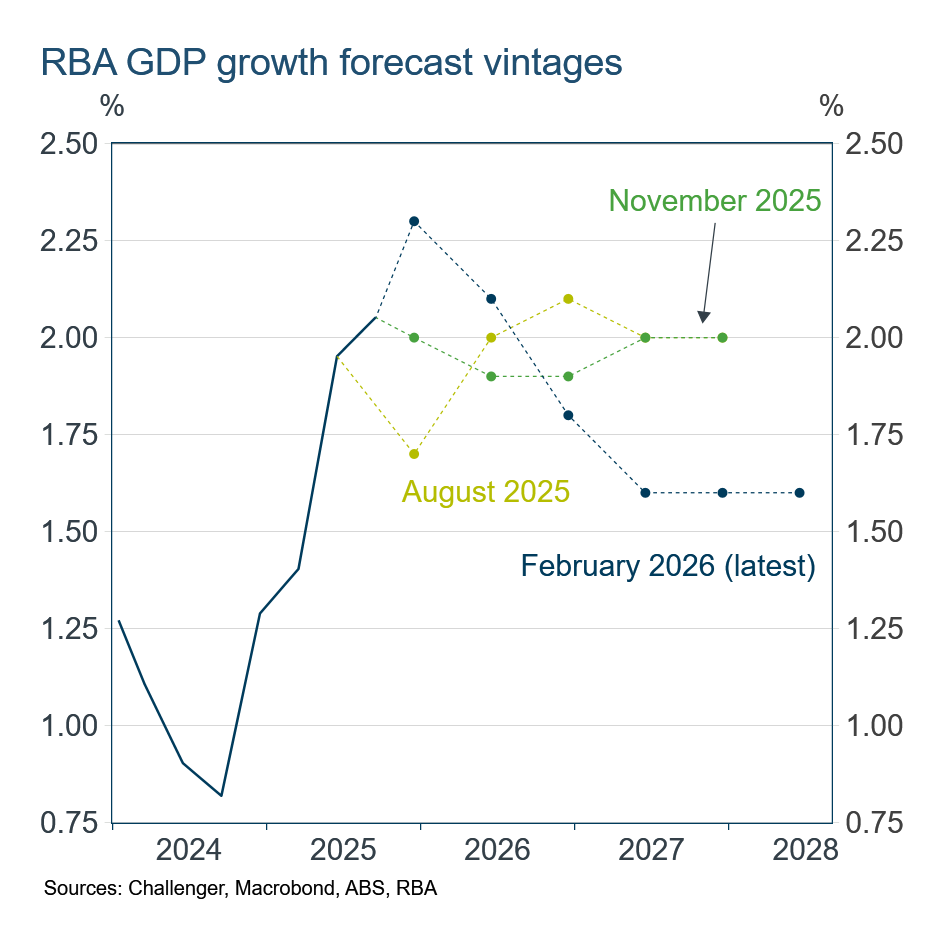

The higher path for the cash rate will slow economic growth. GDP growth is inherently noisy and so not surprisingly forecasts also move around. Growth has been stronger than the RBA had expected, but with the higher cash rate and higher inflation acting as a restraint on spending, the economy is projected to slow substantially later this year and into next year. The RBA forecasts growth next year to be 1.6%, implying there will be next to no growth in per capita GDP, the main driver of higher living standards.

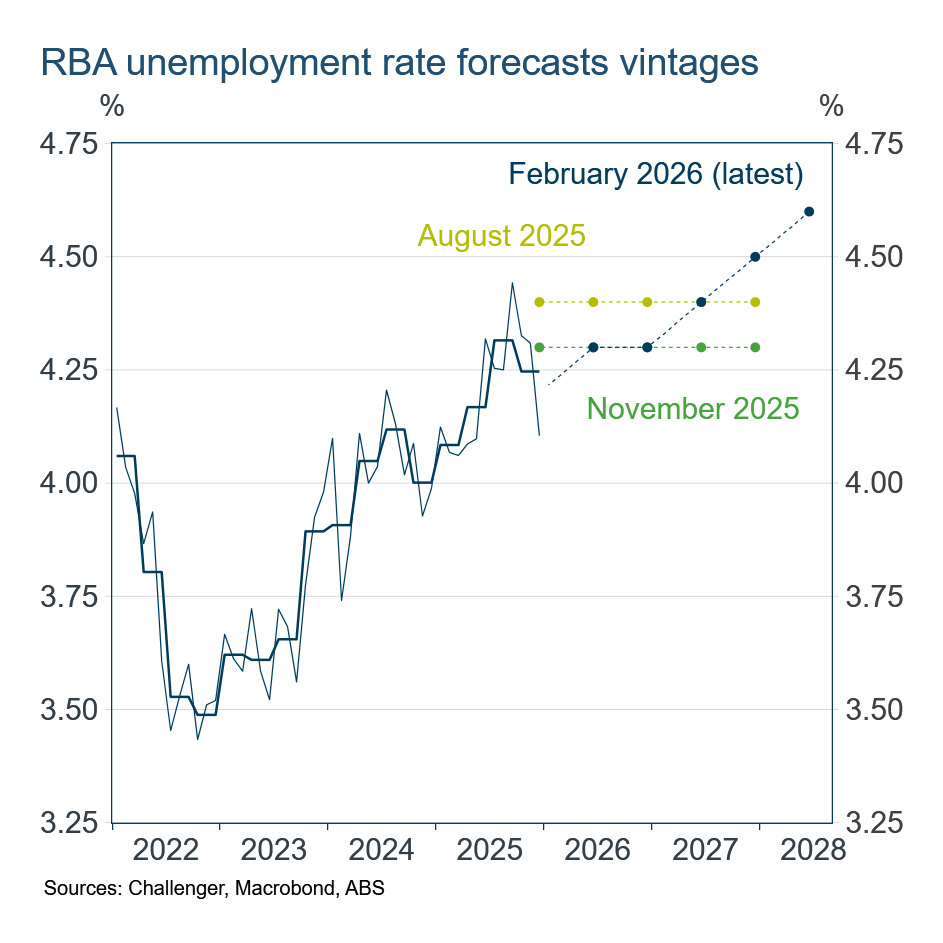

Slower growth in GDP will feed through to slower employment growth and a pick-up in the unemployment rate to around 4.6%. That’s still lower than most of the past 50 years. Given the RBA has highlighted that there is little spare capacity in the labour market – i.e. it’s fairly easy to get a job and hard for businesses to find qualified workers – this increase in unemployment is needed to slow wages growth and inflation.

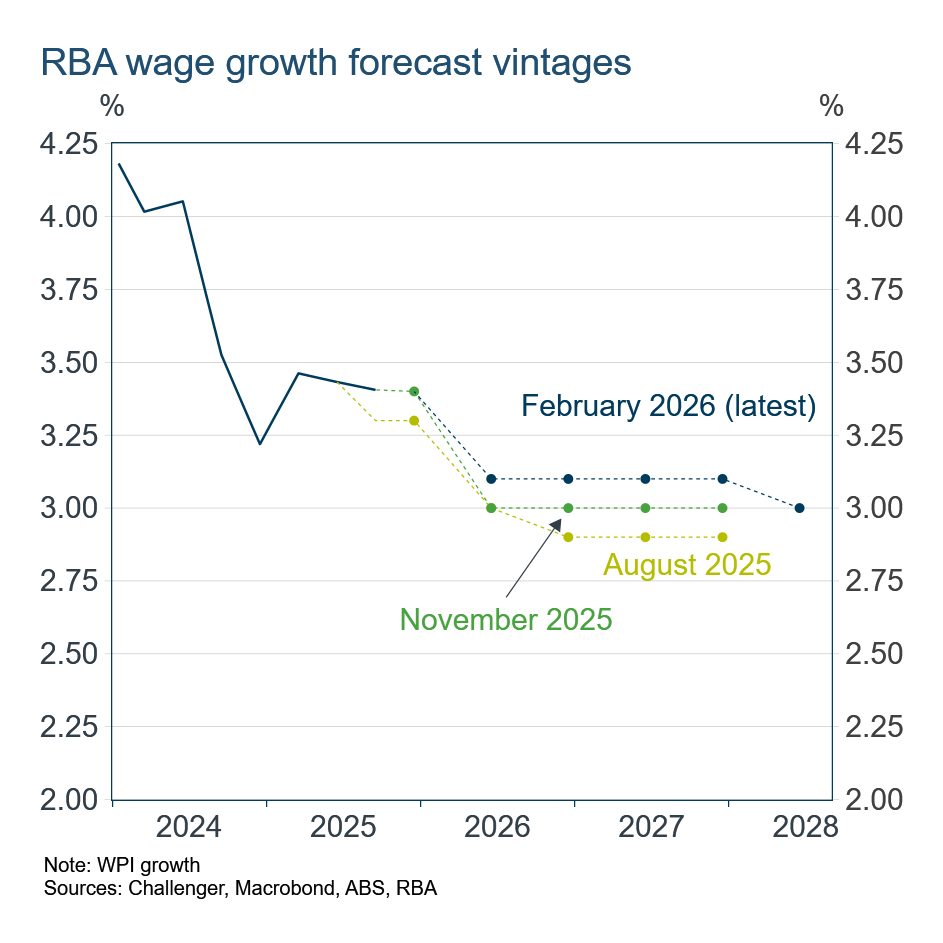

However, the RBA’s forecasts have slightly increased the expected rate of wages growth. Higher inflation, and a still tight labour market, mean wages growth won’t slow as much as previously expected.

All up it’s a fairly sobering set of forecasts. The biggest risk is that a cash rate of 4.25% won’t be sufficient to reduce inflation from 3.7%. This risk is highlighted by the relatively moderate projected increase in the unemployment rate, and wages growth that is now expected to be slightly stronger than in previous forecasts. If anything, these forecasts point to a significant chance that the RBA will have to increase the cash rate by more than the two rate hikes in the cash rate path used in its forecasts.