How rising oil prices are pushing inflation and interest rates higher

Subscribe to Macro Musing

To stay up to date on the latest economic insights, subscribe to Macro Musing on LinkedIn.

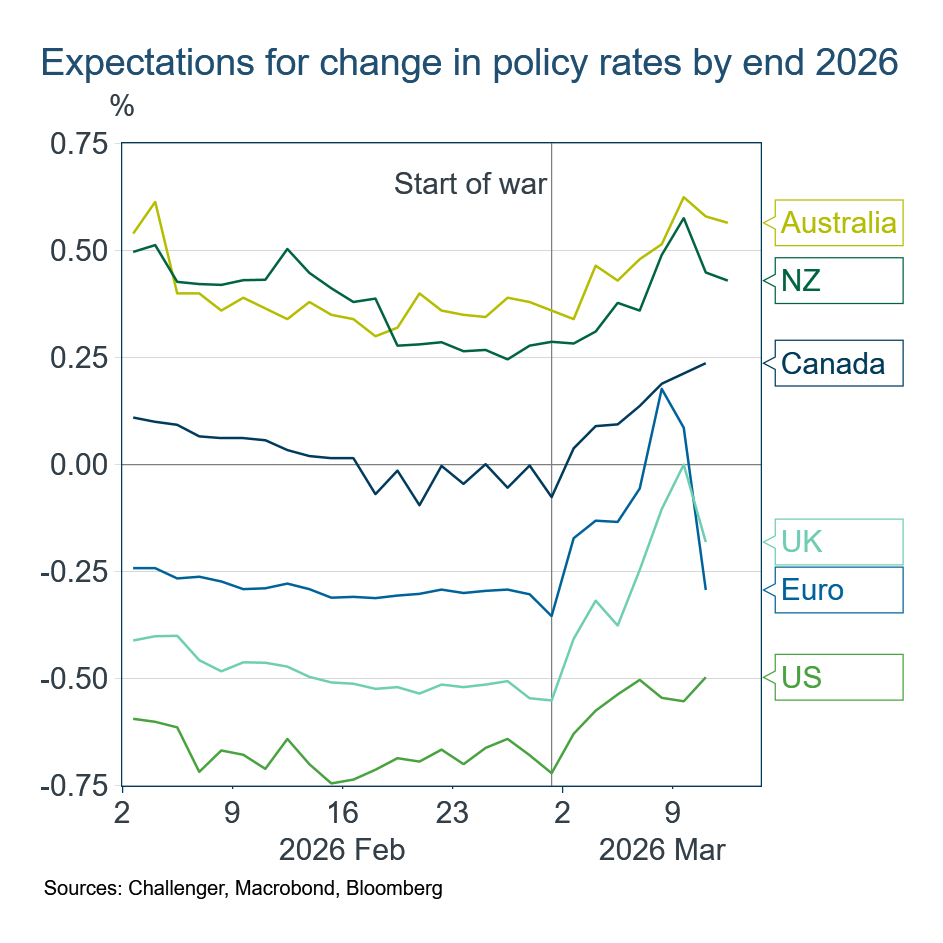

The US–Israel–Iran war has seen expectations for central banks’ policy rates move higher. Since the onset of the war, market pricing has changed to include one additional rate increase by the end of the year for Australia, New Zealand and Canada, and one fewer rate cut for the US and UK. Market pricing for Europe also moved higher – by almost 50 basis points – but this has reversed sharply over the past two days.

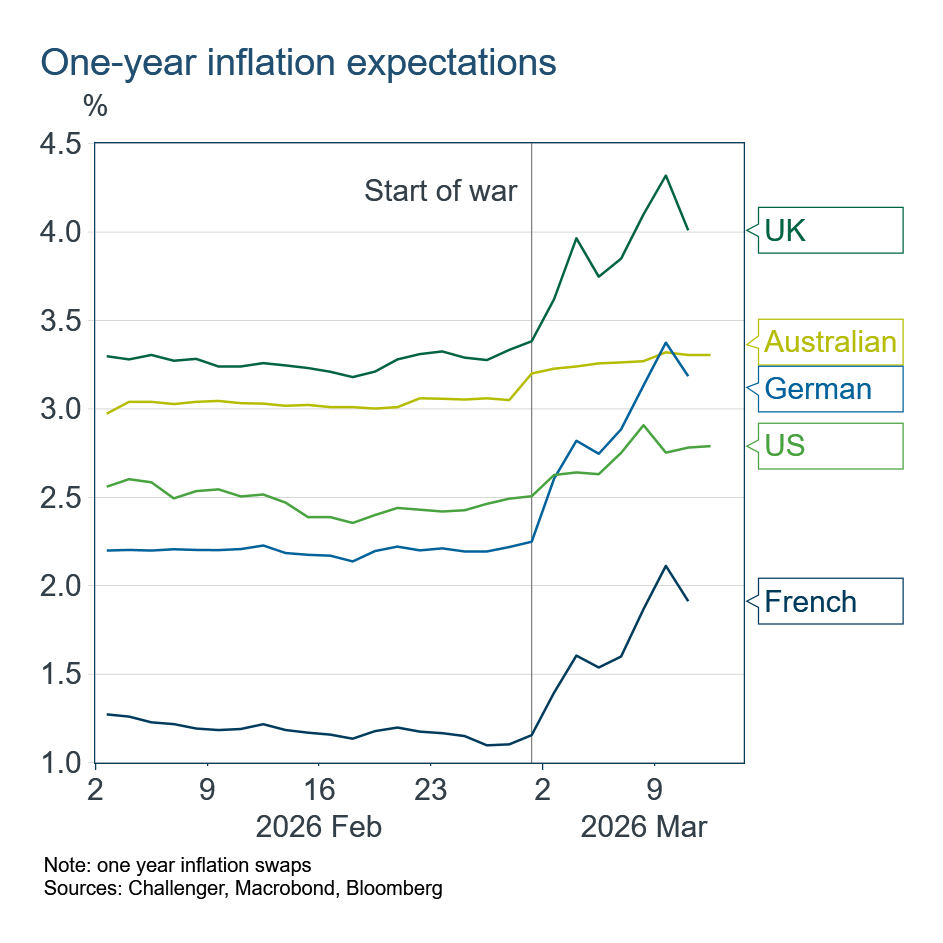

Expectations for higher policy rates reflect higher projected inflation resulting from the increase in oil prices. The standard prescription for central banks is to ‘look through’, i.e. ignore, short-lived supply shocks such as the sharp change in oil supply and prices. A negative supply shock, like a jump in oil prices, increases inflation but lowers economic growth and employment, pushing deviations from a central bank’s targets in opposite directions. In such circumstances, the usual policy response is to do nothing.

However, following several years of inflation well above target, central banks are seen as more sensitive to the risk that high inflation could push inflation expectations higher. Persistently higher inflation expectations would require policy rates to remain higher for longer. Recent increases in short-term inflation expectations have therefore led markets to price-in higher central bank policy rates.

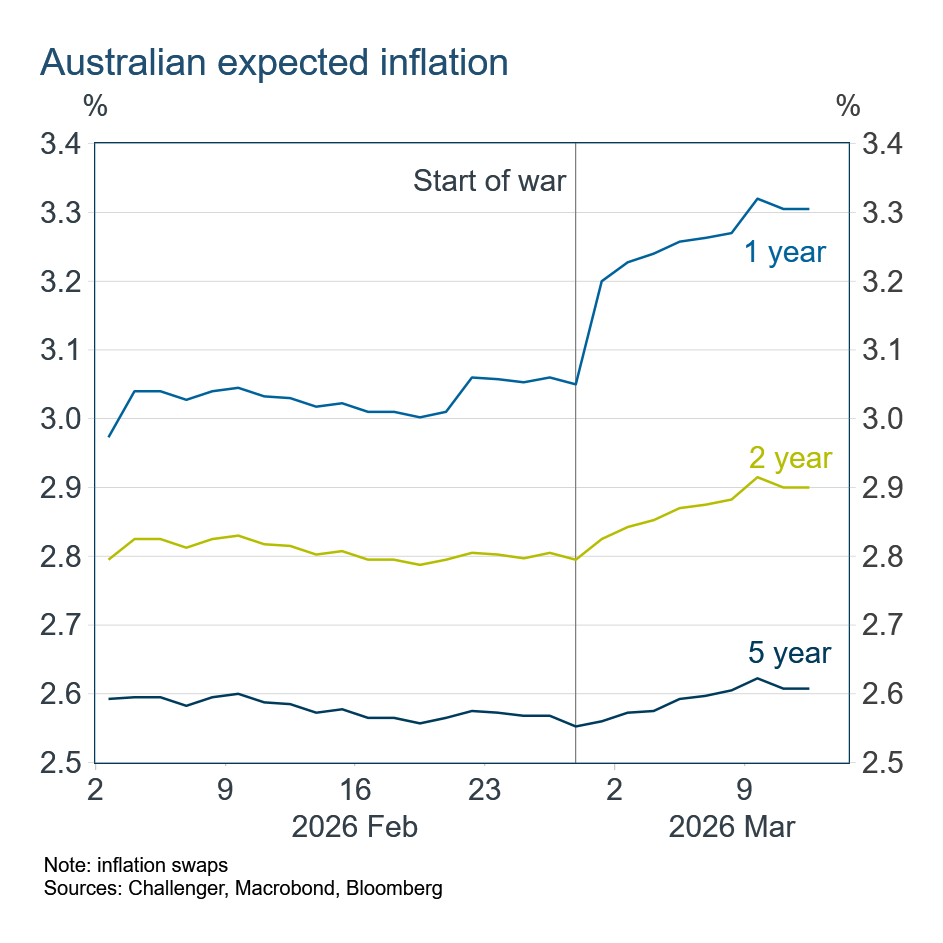

Markets nevertheless expect the boost to inflation to fade over time. In Australia, one-year inflation expectations – based on swaps – are around 0.25 percentage points higher, while two-year inflation expectations are only about 0.1 percentage points higher. Given higher inflation in the first year, this implies little change to inflation in the second year.

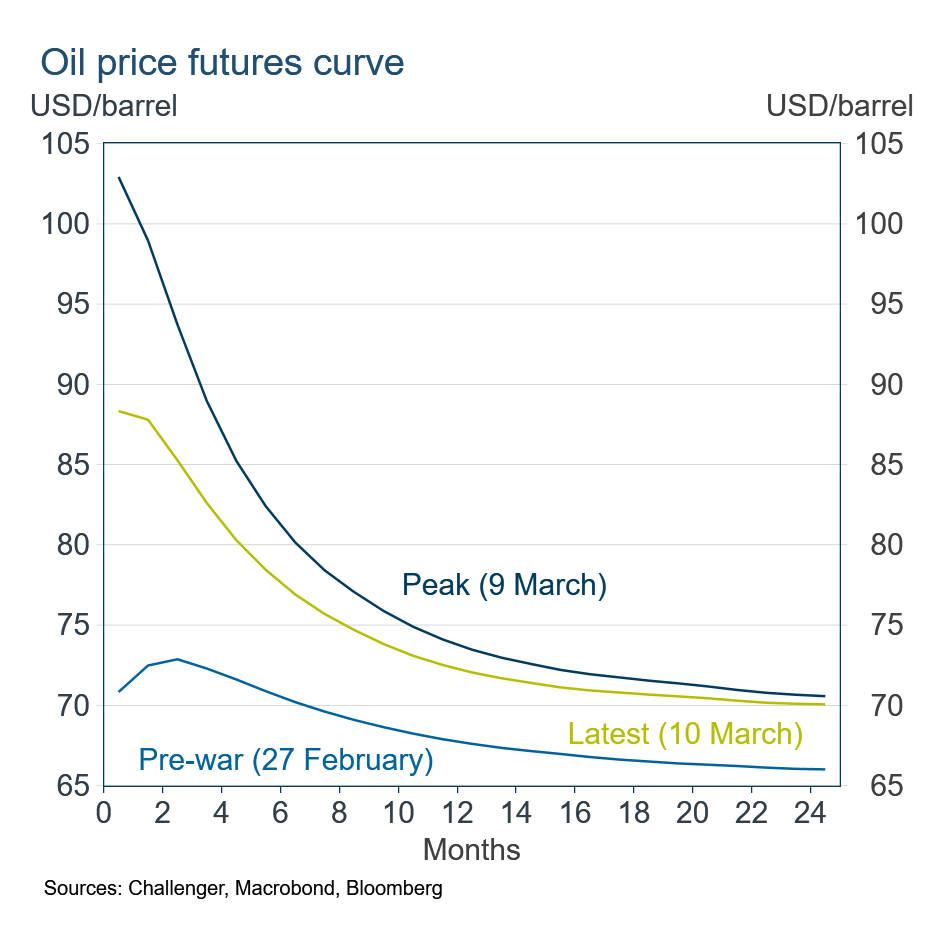

The expectation that inflation pressures will be temporary is broadly consistent with oil futures prices. However, for storable commodities such as oil, futures prices cannot be interpreted simply as the market’s expectation of the future spot price. If the futures price exceeds the spot price by more than the cost of storage, oil can be stored today to profitably meet future demand. By contrast, when the spot price is higher than the futures price, future supply cannot be brought forward to meet current demand. The current downward-sloping (‘backwardated’) futures curve indicates that demand is high now relative to supply. At the same time, the slope of the curve suggests that the market expects the supply shortage will be largely resolved over the coming months.

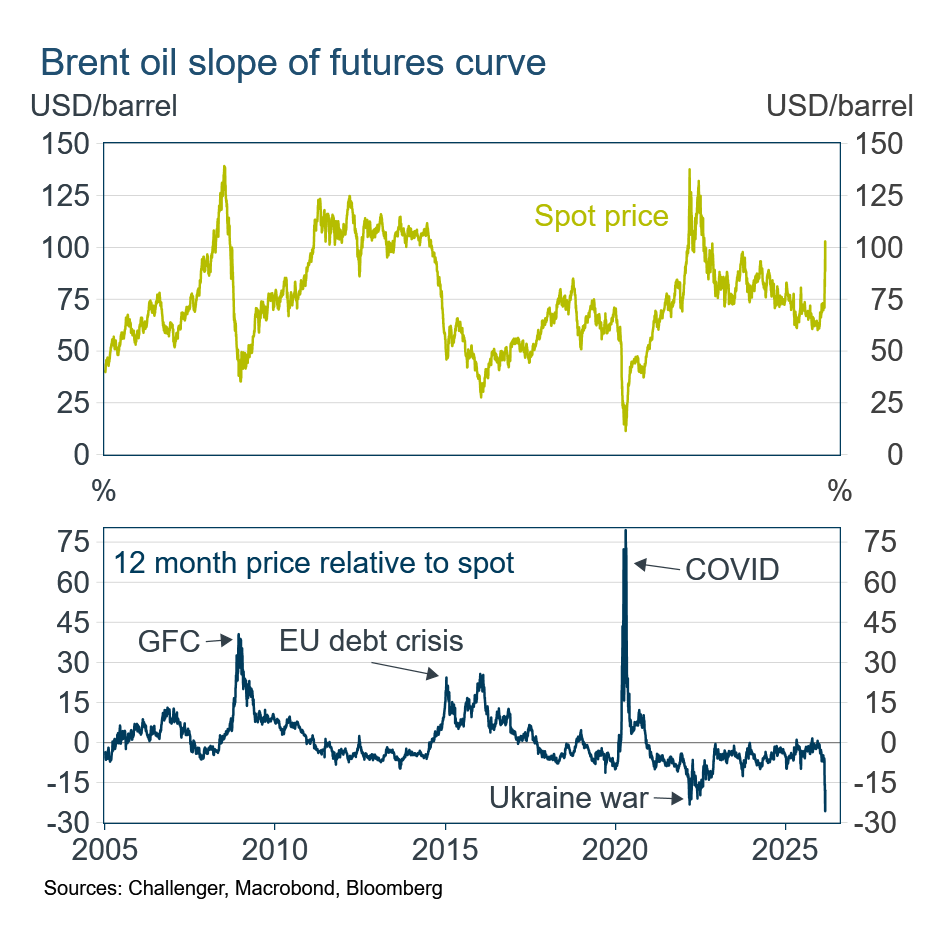

The slope of the oil futures curve – measured as the 12-month futures price relative to the spot price – moves sharply in response to major events that affect the spot price. Periods of sharply weaker demand – such as during the Global Financial Crisis, the European debt crisis, and COVID-19 – saw the futures curve steepen significantly. In contrast, episodes of sharply weaker current supply, such as Russia’s invasion of Ukraine, are associated with a pronounced downward-sloping futures curve. The current degree of backwardation is steeper than with Russia’s invasion of Ukraine, highlighting a larger near-term contraction to supply.

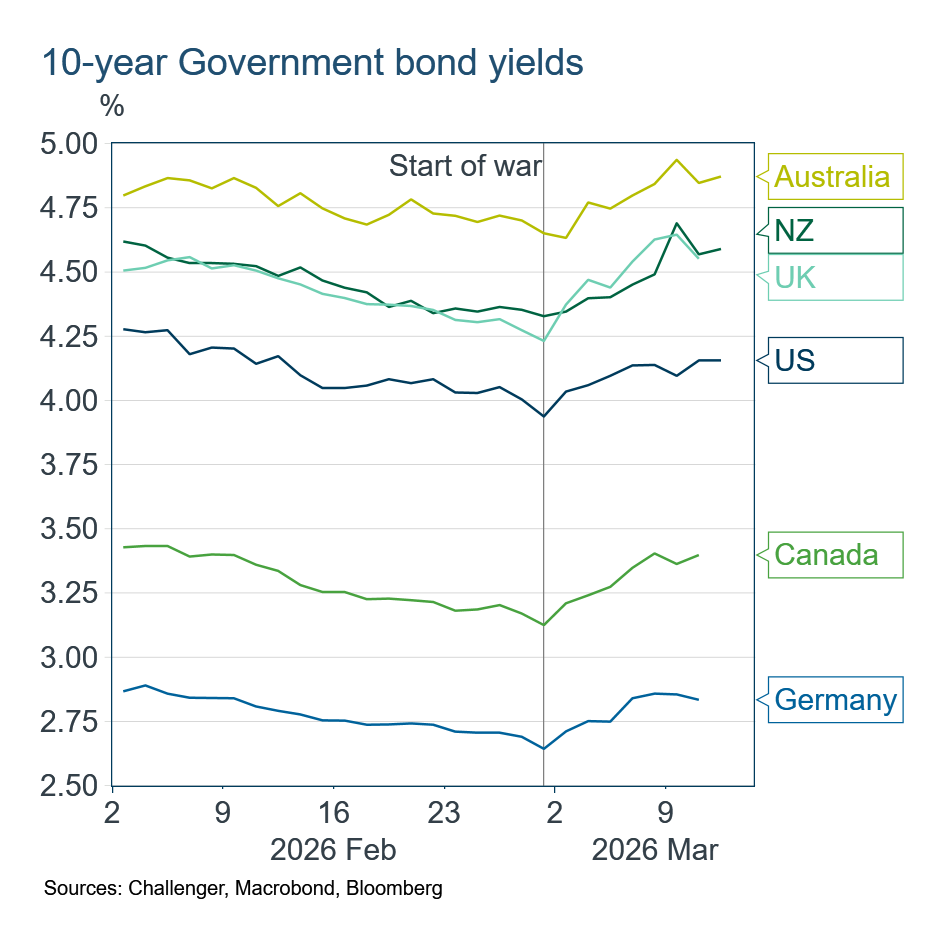

Higher – but likely short-lived – expected inflation, combined with increased uncertainty, have pushed bond yields higher across a range of countries since the onset of the Middle East war.

While near-term oil flows remain uncertain, war in the Middle East has certainly pumped up interest rates.