IMF forecasts warn global growth hit by Middle East war

Subscribe to Macro Musing

To stay up to date on the latest economic insights, subscribe to Macro Musing on LinkedIn.

The International Monetary Fund’s latest forecasts show the negative economic impact of the Middle East war.

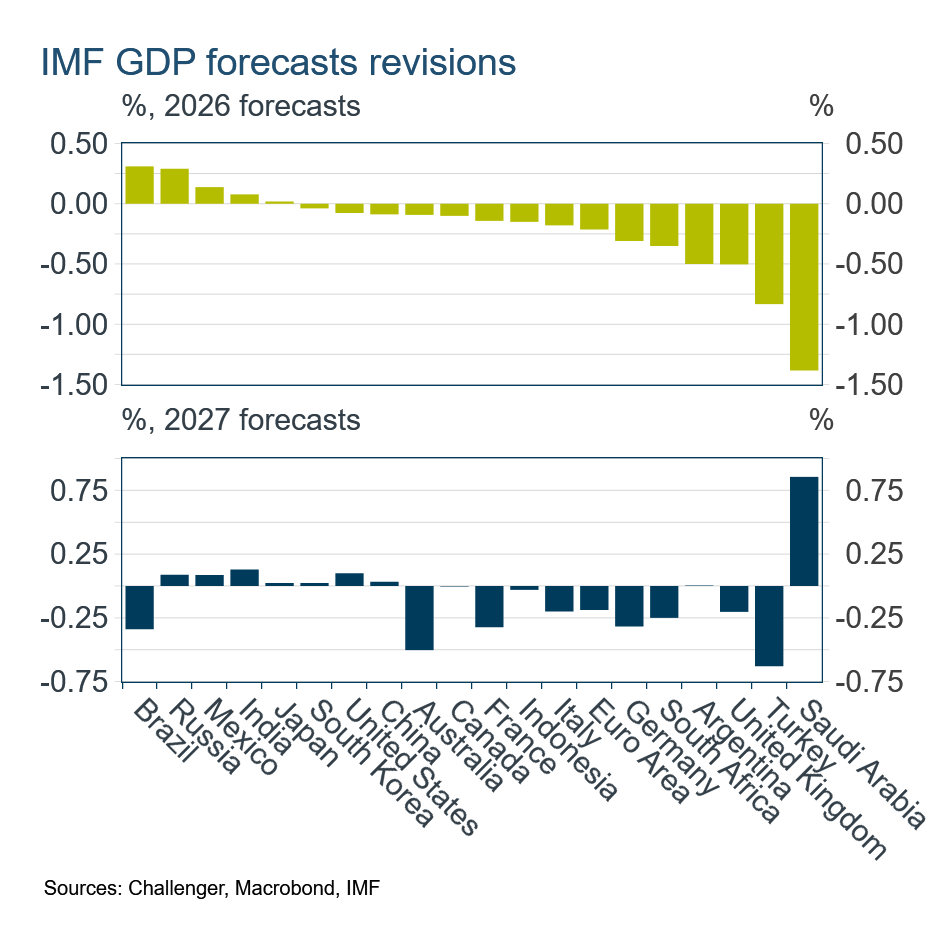

Prior to the onset of the war, the IMF was intending to revise up its forecast for global growth in 2026 to 3.4%, given improved economic momentum. Instead, the higher oil price and flow-on effects from the Middle East war have pushed growth down by 0.3 percentage points to 3.1%. The impact on growth is greatest in emerging market economies, particularly oil importers, but small for most advanced economies.

However, the IMF noted that the outlook is uncertain, depending heavily on when the war ends and whether oil prices rise further. Its baseline forecasts assume that the conflict does not escalate and that the oil price slowly falls to average of US$82 per barrel in 2026. However, if the war escalates and the oil price averages around $110 in 2026, global growth would be about 0.6 percentages point lower. In other words, an escalation would be damaging but not catastrophic for the global economy. Of course, the more significant an escalation the larger the hit to growth.

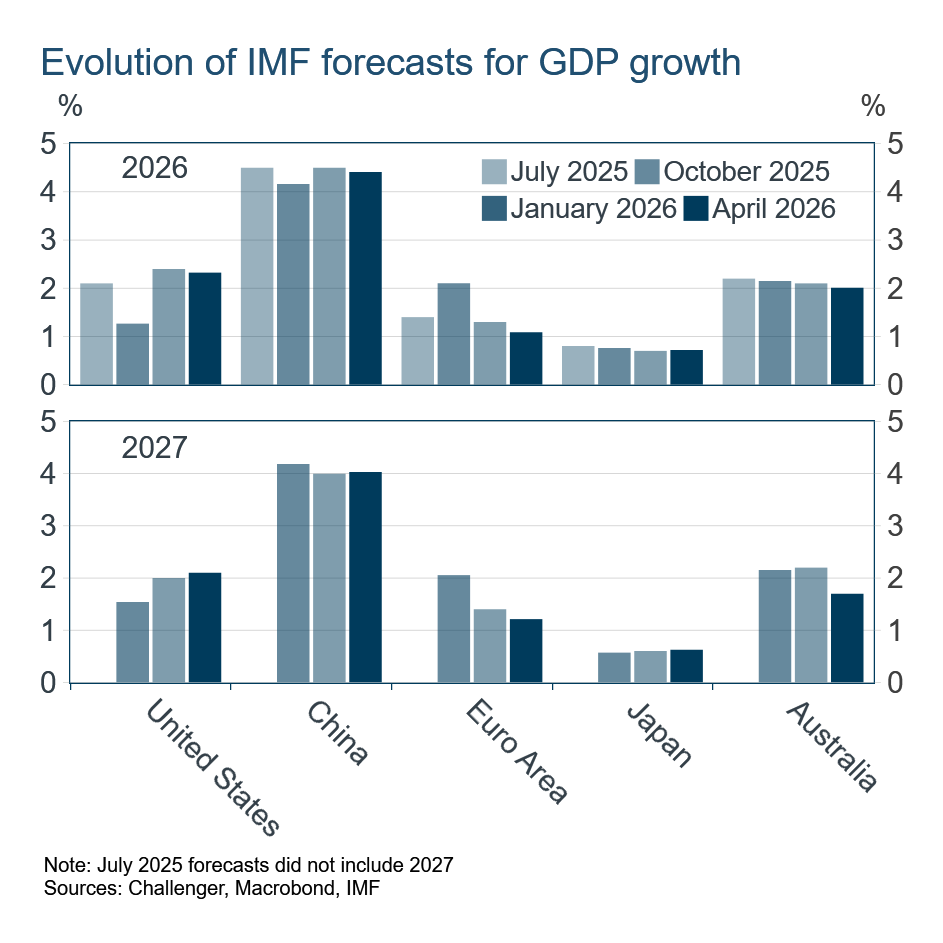

Growth forecasts for Australia were revised down more than in other advanced economies reflecting pre-existing higher domestic inflationary pressures and the impact of tighter monetary policy. Forecasts were also revised down slightly for the Euro area but were fairly steady for the United States, Japan and China.

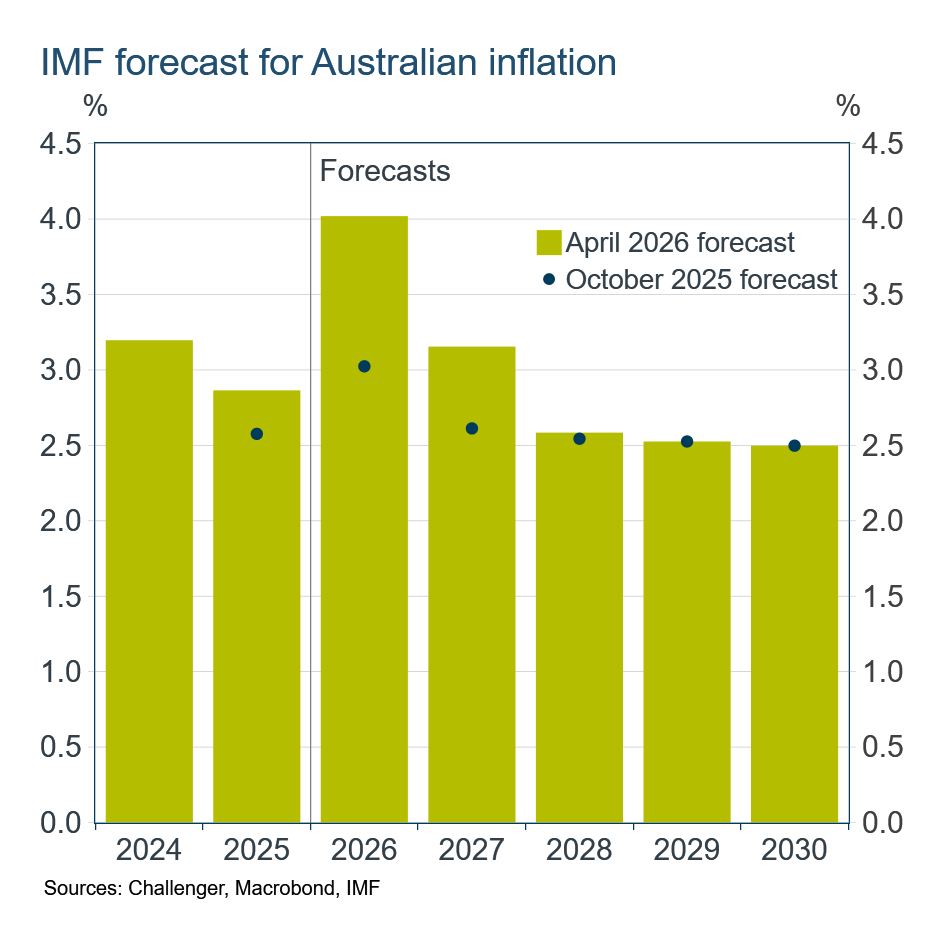

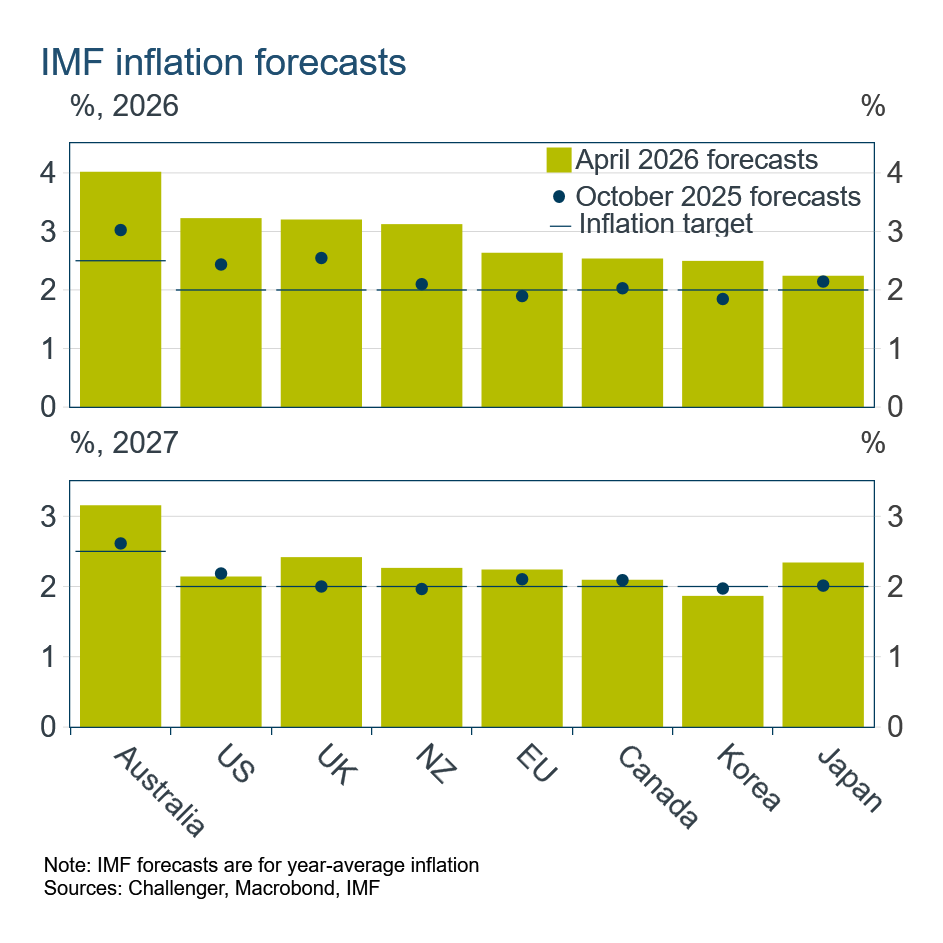

The more pervasive impact of the oil price shock is on inflation. Forecasts were revised higher across the board. The upward revision was large for Australia, reflecting the domestic inflation pressures that pre-date the war. The IMF expects Australian inflation to be 4% for 2026 and to still be above the RBA’s 2.5% target over 2027. By contrast, for most other countries the inflation shock is expected to be short-lived, with inflation back around central banks’ targets in 2027. That suggests the RBA policy rate should remain higher for longer than in other economies, contributing to a higher Aussie dollar.

The problem for the RBA and Australia is that the oil price shock came at the wrong time. Inflation was already picking up and even in October – when the full extent of Australia’s inflation resurgence was yet to be revealed – the IMF was forecasting inflation to peak at 3% in 2026. With higher oil prices and domestic capacity constraints, inflation is expected to peak higher and be more persistent. The good news is the IMF still has faith that the RBA will get inflation back to its 2.5% target by 2028, although if it didn’t we should be truly worried.