Implications of the Middle East war

Subscribe to Macro Musing

To stay up to date on the latest economic insights, subscribe to Macro Musing on LinkedIn.

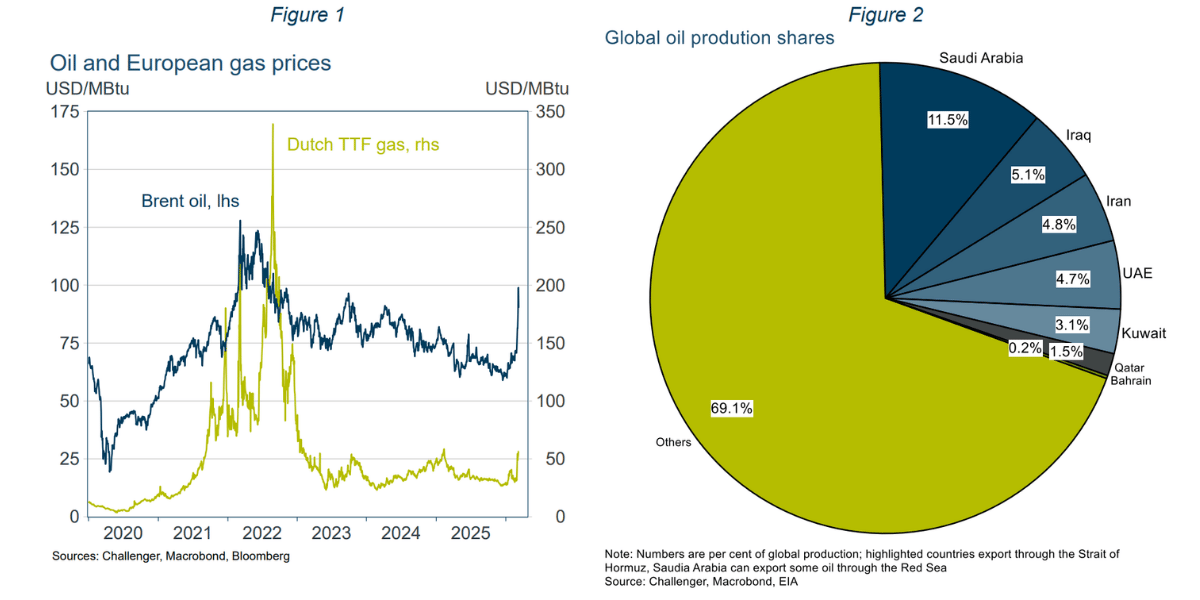

While the attack on Iran by the United States and Israel was not unexpected, the scale has taken analysts by surprise, leading to a significant jump in the price of oil.

There was a small risk premium built into the oil price in anticipation of an attack but given the larger-scale assault Brent oil jumped from $72 per barrel to around $80 a week ago with the onset of the conflict. The oil price drifted higher through the week to close last week just over $93. This week markets were jolted from their slumber with oil jumping sharply on Monday and trading as high as $118 intraday before falling back to around $90 in overnight trading (Figure 1).

The European gas price, Dutch TTF, jumped 70% after gas facilities in Qatar were attacked, however, this jump pales in comparison with the six-fold increase seen when Russia invaded Ukraine in 2022.

The sharp market reaction is because countries surrounding the Persian Gulf (also called the Arabian Gulf) account for around 30% of global oil production (Figure 2). Around 20% of global production – 20 million barrels per day (mbpd) – is shipped through the narrow Strait of Hormuz between Iran and Oman.

Because the Strait is narrow and close to Iran, ships travelling through the Strait are vulnerable to attack from Iran or from sea-mines. Iran has not declared the Strait closed, but insurance companies have increased costs or are refusing to insure ships travelling through the Strait. Effectively, there is now a complete standstill in shipping through the Strait, with only two recorded ships passing through the Strait over the past week (Figure 3).

Cutting off oil supply from the Persian Gulf countries today is a smaller shock than in earlier years. Much of the expansion in oil production over the past 15–20 years has come from other parts of the world, particularly the United States, but also Canada and Brazil (Figure 4). The increase in US production has shifted the United States from being a net importer of 12.5 mbpd in 2005 to now being a net exporter of around 2.5 mbpd. This significantly reduces the negative impact that the war in the Middle East will have on the US economy.

There are also some options to bypass the Strait of Hormuz which will reduce the impact of the war on oil markets. Saudi Arabia has its 1,200 km ‘East–West’ pipeline across the country which has been used to move around 2 mbpd to the western side of the country to export through the Red Sea. This is less than the pipeline’s capacity of 5 mbpd (which can be extended to 7mbpd by temporarily converting natural gas lines to carry crude oil). The UAE also has a pipeline that extends to Oman, bypassing the Strait of Hormuz, with a maximum capacity of around 2 mbpd. These pipelines may allow some oil to be exported despite the Strait being closed to shipping, so long as production is not impeded.

While oil exports from other Gulf countries will likely recover quickly if oil assets continue to be spared attacks, Iranian oil production infrastructure will take longer to repair, cutting off Iranian oil exports for longer. Iranian exports have fluctuated over the past 15 years as the country has been subject to sanctions. In the past few years Iranian production and exports have recovered to around their pre-sanction levels (Figure 5). Iranian oil, like Russian oil, has sold at a discount. China will be particularly affected by the cessation of oil exports from Iran. China has purchased 90% of Iran’s oil, accounting for around 13% of China’s oil imports or almost 7% of China’s total oil consumption (Figure 6).

The longer oil from the Persian Gulf countries is blocked from the world market the larger the price effect will be. The jump this week reflects the realisation of how long oil exports may be impeded and how long it will take for Persian Gulf exports to return to their pre-war levels.

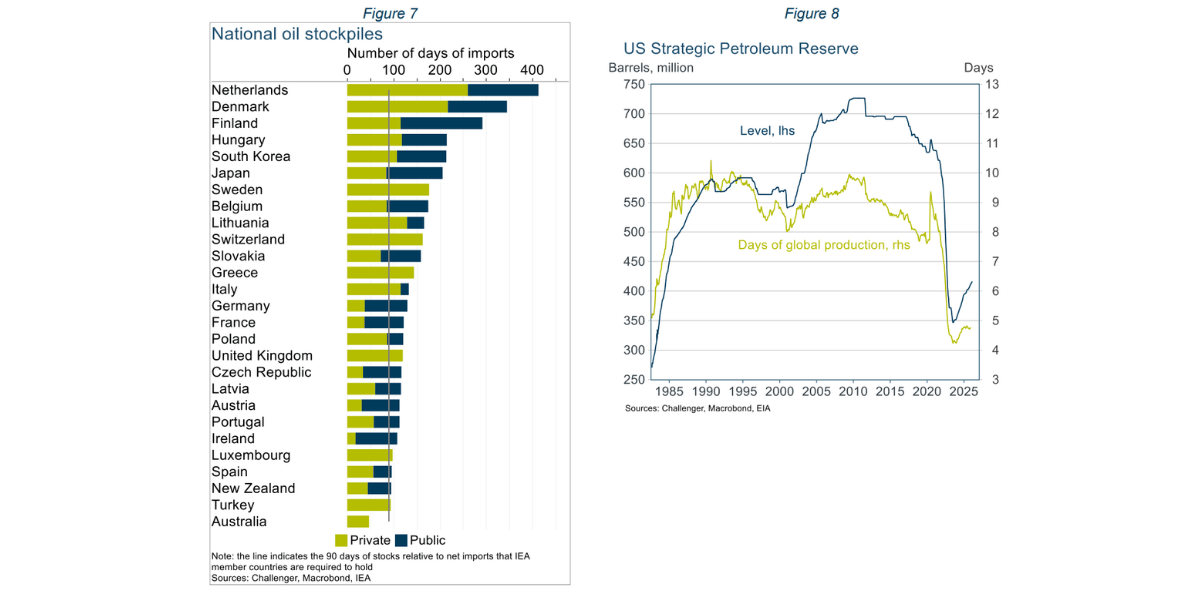

For some time, the price impact could be cushioned by supplies of oil in transit and privately and publicly held stocks. Member countries of the International Energy Agency (IEA; the group of developed, OECD, economies that are mostly oil importers) are required to hold stocks equivalent to at least 90 days of oil imports (Figure 7). There have been discussions but no agreement on IEA members releasing some of their strategic oil reserves.

In the latest available data, from November, Australia is reported as having oil stocks equivalent to just 54 days of imports. Australia was the only country reported as not meeting the 90-day requirement and had stocks significantly smaller than the Netherlands and Denmark which each hold more than one year of imports. This is despite Australia having a policy on fuel security which includes leasing some capacity in the US Strategic Petroleum Reserve; however, this is obviously a long way from Australia. The security consequences of holding Australia’s strategic oil reserve offshore have been widely criticised. It has been reported that as of 3 March Australia’s strategic reserve comprised 36 days of petrol, 32 days of diesel and 29 days of jet fuel. The small stockpile can lead to concerns about shortages, and so the queuing and hoarding by individuals and businesses we’ve seen this week.

The United States government released close to half of its Strategic Petroleum Reserve in 2022 to reduce the impact on oil prices when Russia invaded Ukraine (Figure 8). As a result, the US now has lower stocks than it has had for decades, and so would be less able to release reserves to limit the current price rise.

Other implications

The Middle East war also has the potential to affect food availability and prices. Roughly one-quarter to one-third of the raw materials used to manufacture fertiliser globally pass through the Strait of Hormuz. Some fertiliser prices have jumped 25%, although these are less liquid markets than oil and so the price impact is much more uncertain.

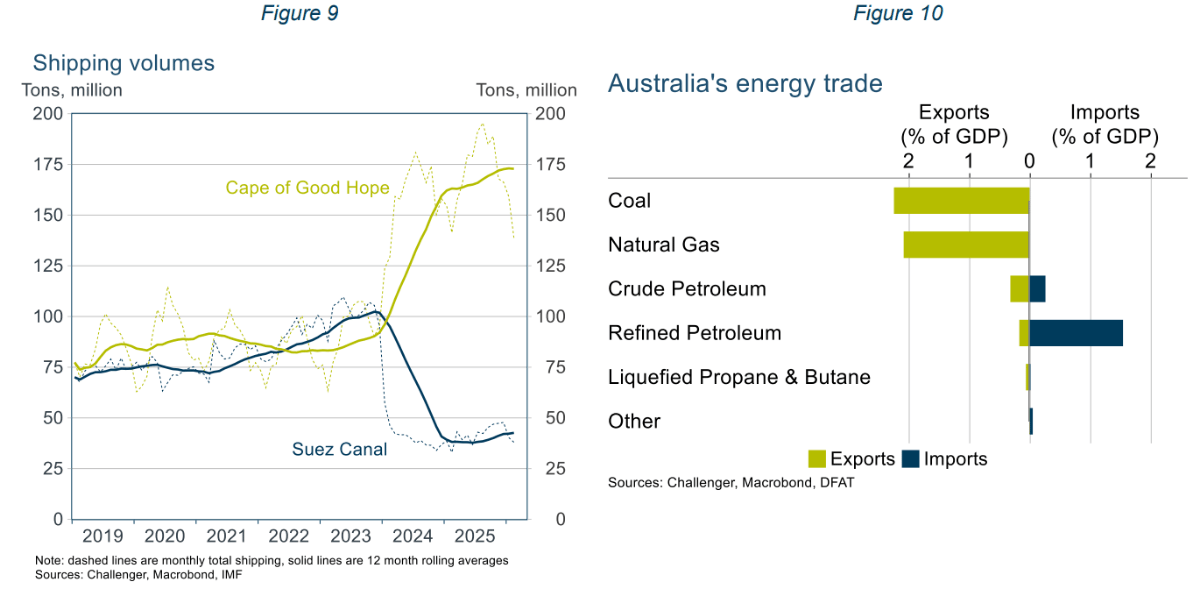

Shipping could also be disrupted in the Red Sea. The Houthis in Yemen, declaring their support for Iran, have stated that they would attack ships in the Bab-el-Mandeb Strait as they head to the Suez Canal. However, to date there have been no new attacks on ships. In any case, this route has become less important to global trade as shipping volumes have not recovered from the fall in 2024 when attacks commenced (Figure 9).

Since the war began, there have been virtually no flights through Middle Eastern hubs, with reportedly 30,000 flights in the region cancelled. Around half of international flights to Europe from Australia transit through the Middle East. However, while disruptive the aggregate impact will be small as only a small share of tourists to Australia come from Europe, and most Australians travelling overseas go to non-European destinations. In 2025, only 19% of tourists came from Europe, and only 16% of Australians travelling overseas went to Europe.

Australia is a net energy exporter however it will not benefit from this energy price shock. This shock is specific to the supply and price of oil and gas. While Australia exports gas, the gas market is more segmented than the oil market and has longer-term contracts. Australia’s other key energy export is coal, which has very limited substitutability with oil. As a result, the cost of Australia’s energy imports will increase significantly relative to its energy exports (Figure 10).

Economic implications

The jump in the oil price will increase inflation globally and reduce growth in oil-importing countries. Within and across countries, the increase in the oil price reallocates income from oil consumers to oil producers. Oil producers, or their owners, tend not to increase their spending as much as consumers reduce theirs, hence the decline in economic growth. Oil exporters outside the Middle East will benefit from the higher oil price (Figure 11). However, China, India and most European countries are net oil importers who will experience weaker economic growth.

The higher oil price will directly increase petrol prices in Australia and indirectly increase other prices through transportation costs and higher input prices. If the oil price stays at $90 then the petrol component of the CPI will jump around 15%, directly adding around 0.5 percentage points to inflation in the first month (Figure 12). Including indirect effects, the total impact on inflation could be around 0.75 percentage points. If the Strait of Hormuz remains closed for longer than a month, the oil price – and inflation – will increase further. GDP growth is likely to be reduced by around 0.2 percentage points.

While the RBA ordinarily looks through the direct impact of an oil shock on inflation it will need to be cautious about doing so given the high inflation of recent years. The RBA will be very mindful of oil-induced higher inflation leading to higher inflation expectations. Higher inflation expectations would make it harder for the RBA to return inflation to its 2.5% target, meaning the cash rate would be higher for longer. The oil price shock has come at a very awkward time for the RBA given that it was already forecasting inflation to remain above target for a further two years.