Inflation beats forecasts - a rate rise now looks likely

Subscribe to Macro Musing

To stay up to date on the latest economic insights, subscribe to Macro Musing on LinkedIn.

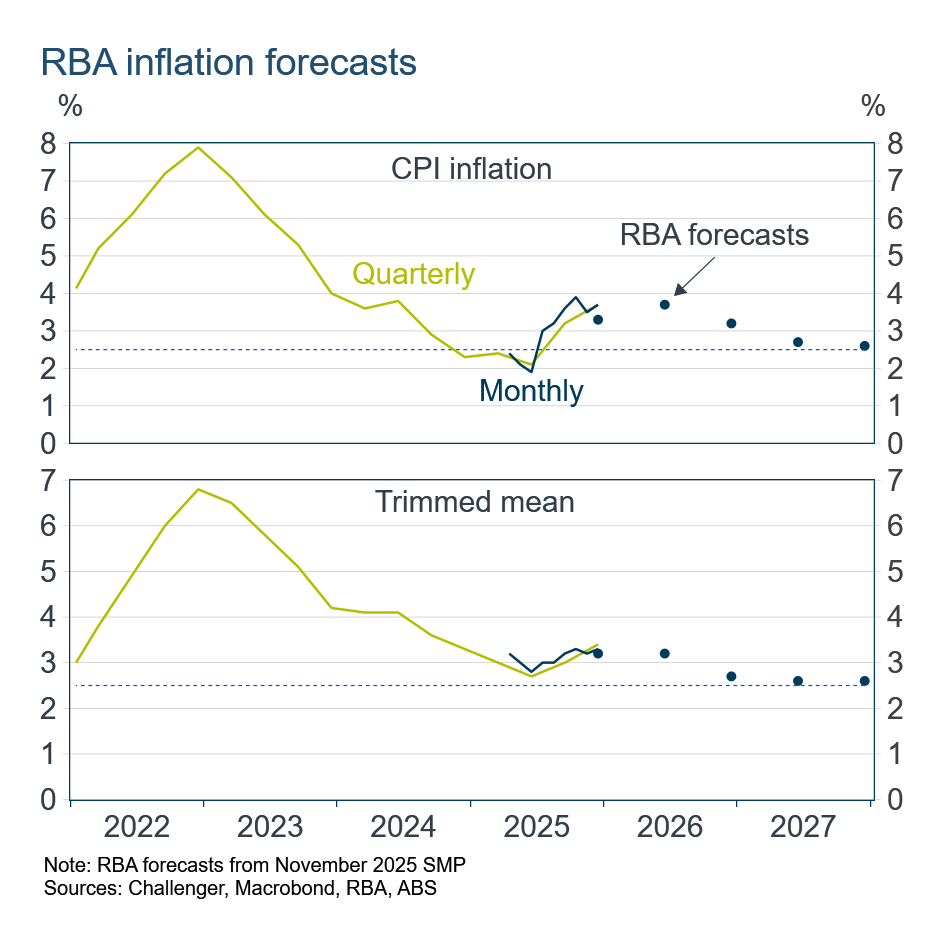

The monthly inflation data confirmed price pressures are stronger than the RBA had previously expected and should see the RBA increase rates next week. CPI inflation over the year to December was 3.7%, higher than the RBA’s forecast of 3.3%. If the RBA wanted to hold rates, they could point to trimmed mean inflation being 3.3% only just above their 3.2% forecast. But as RBA Deputy Governor Hauser noted recently in an interview, the RBA does not operate on a rule based on a single number but focuses on the details of inflation pressures.

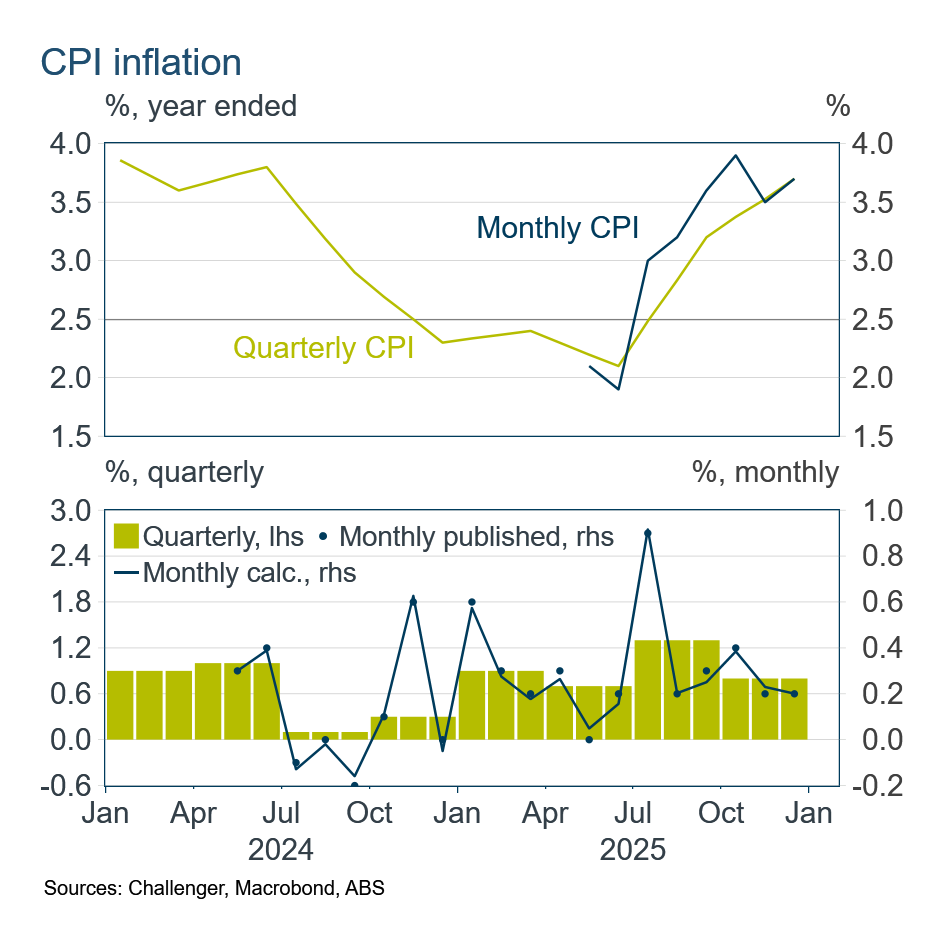

Published CPI inflation was 0.2% in the month of December and 0.7% for the December quarter. Inflation is being driven by housing (5.5% over the year), education (5.4%) and alcohol & tobacco (4.8%). Price pressures are broad based. Inflation exceeds the RBA’s target of 2.5% in 11 of the CPI groups.

The RBA focuses on trimmed mean inflation as it better captures demand and supply pressures by excluding extreme price changes. If you wanted to make a case for holding rates constant you’d point to published monthly trimmed mean inflation slowing to 0.2% from 0.3%. However, much of the slowdown reflects rounding. Unrounded trimmed mean inflation was 0.24%, similar to the previous month.

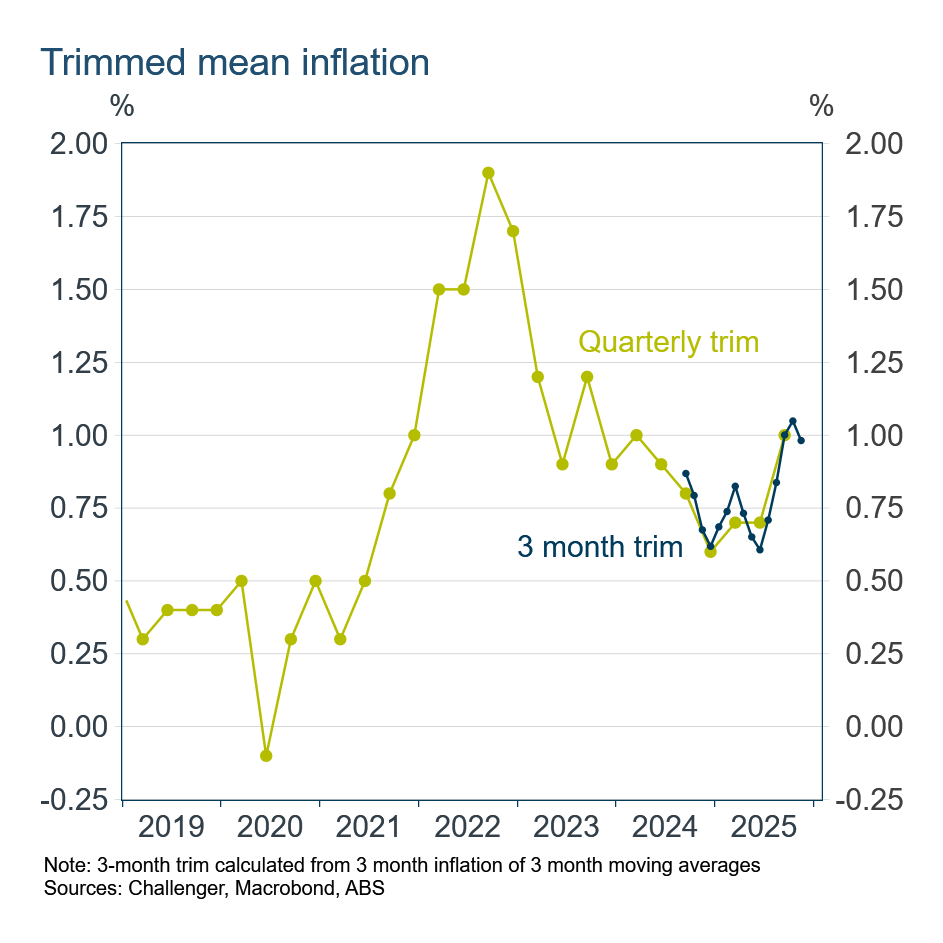

The RBA has also said that given uncertainties in the measurement of the new monthly inflation they will continue to focus on quarterly inflation data. Quarterly trimmed mean inflation was 0.9%. Annualising this quarterly figure gives 3.6% inflation, well above the RBA’s 2.5% target.

This was a slight slowdown from the 1% in the September quarter. As I noted last week, 1% quarterly trimmed mean inflation has only occurred in four episodes in the RBA’s inflation targeting history and all have been when the RBA had or was tightening policy.

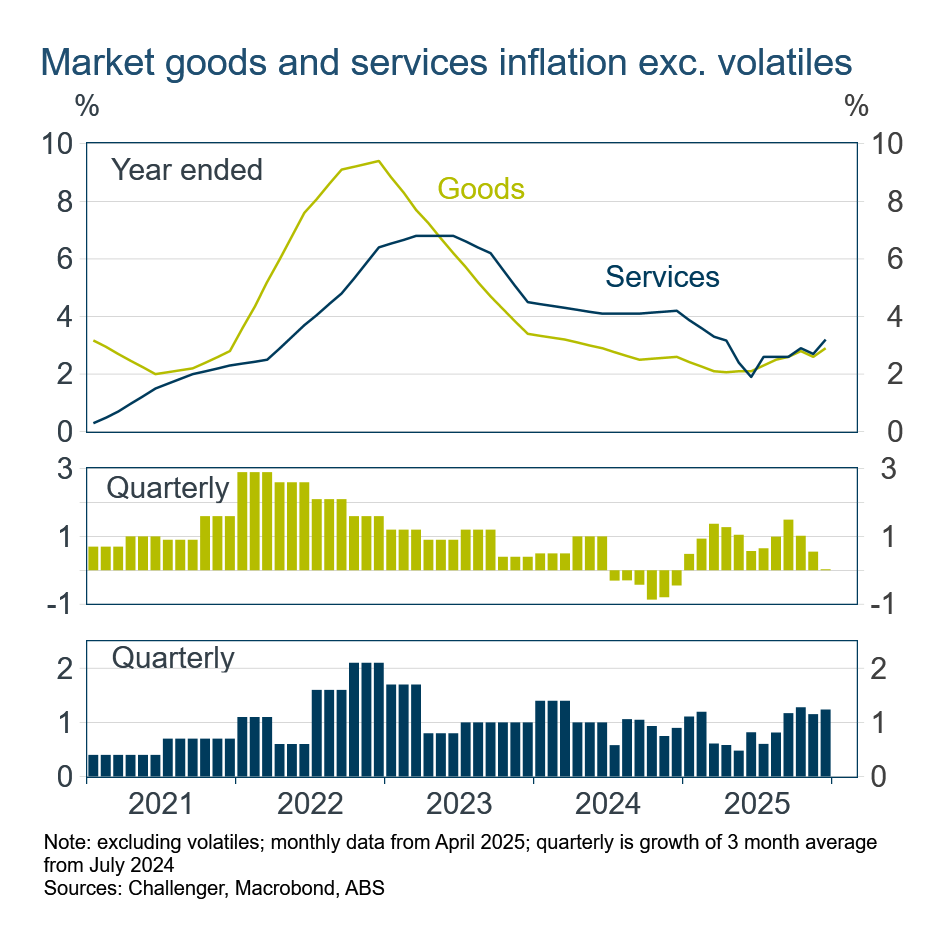

The RBA has also highlighted market services inflation, excluding volatile items, as an important measure of domestically driven price pressures. On a quarterly equivalent basis, this measure of inflation has been over 1% for several months, picking up to be 3.2% on a year-ended basis.

Price pressures are currently inconsistent with the RBA’s inflation target. So what could stop the RBA from tightening?

The RBA has noted they are forward looking and aren’t backward looking responding to past inflation. However, the most recent data highlight current price pressures and forward looking indictors do not suggest that pressure is easing. The labour market is still relatively tight and other measures suggest there is no spare capacity in the economy. The rate of economic growth if anything indicates that spare capacity is tightening, not easing.

There remains uncertainty about the global economy given tariffs and other shocks to international trade, however the global economy has proved to be remarkably resilient over the past year despite these shocks. If the RBA waited for a global slowdown, rising domestic inflation would destroy the credibility of an inflation target already damaged by the post pandemic inflation surge.

Hiking would also put the RBA on a different trajectory to the Fed who will be cutting. However, that’s not unusual, the RBA has frequently been on a different path to the Fed based on domestic conditions.

However, rate rises are not always like cockroaches. One rise does not necessarily mean a second is definite, even if it is likely. Expect little forward guidance from the RBA and an emphasis on data dependency.