Inflation may be easing but underlying price pressures remain persistent

Subscribe to Macro Musing

To stay up to date on the latest economic insights, subscribe to Macro Musing on LinkedIn.

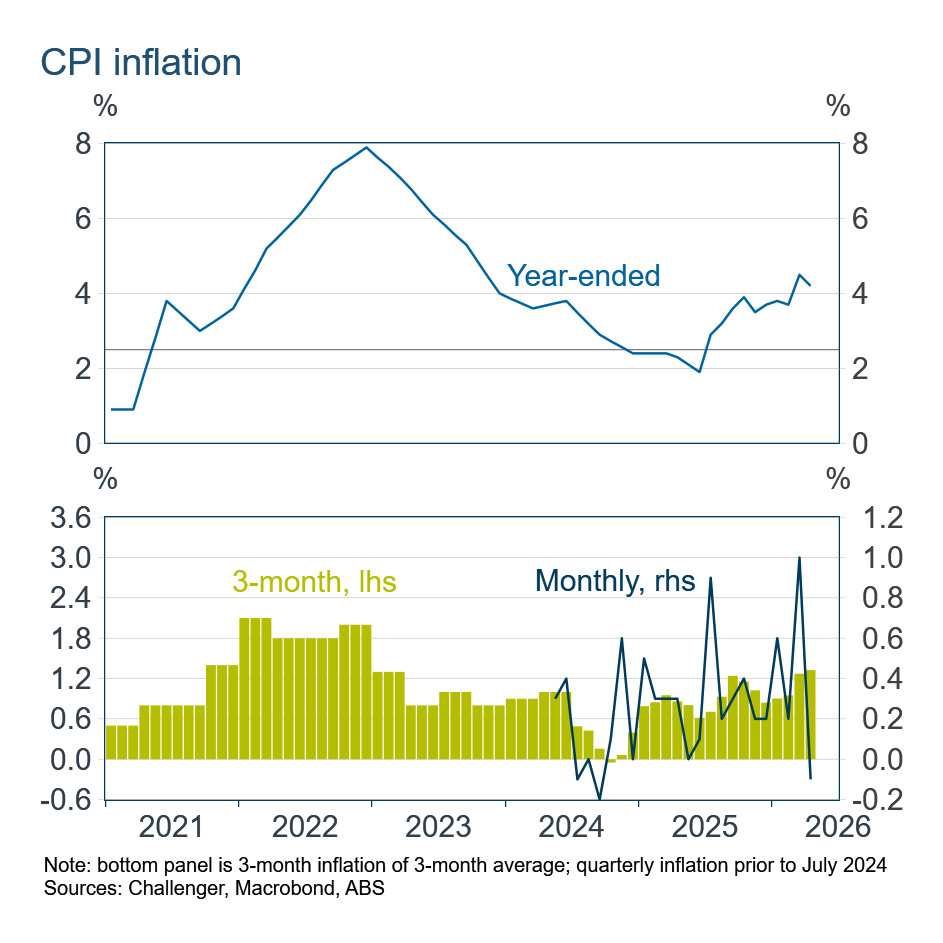

CPI inflation was 4.2% over the year to April a bit softer than survey expectations and a fall from 4.6% over the year to March. Monthly inflation continues to be volatile even when seasonally adjusted. Three-month inflation – which is smoother and equivalent to quarterly inflation, but more timely – was 1.3% in April, a slight increase, highlighting that inflation pressures remain firm.

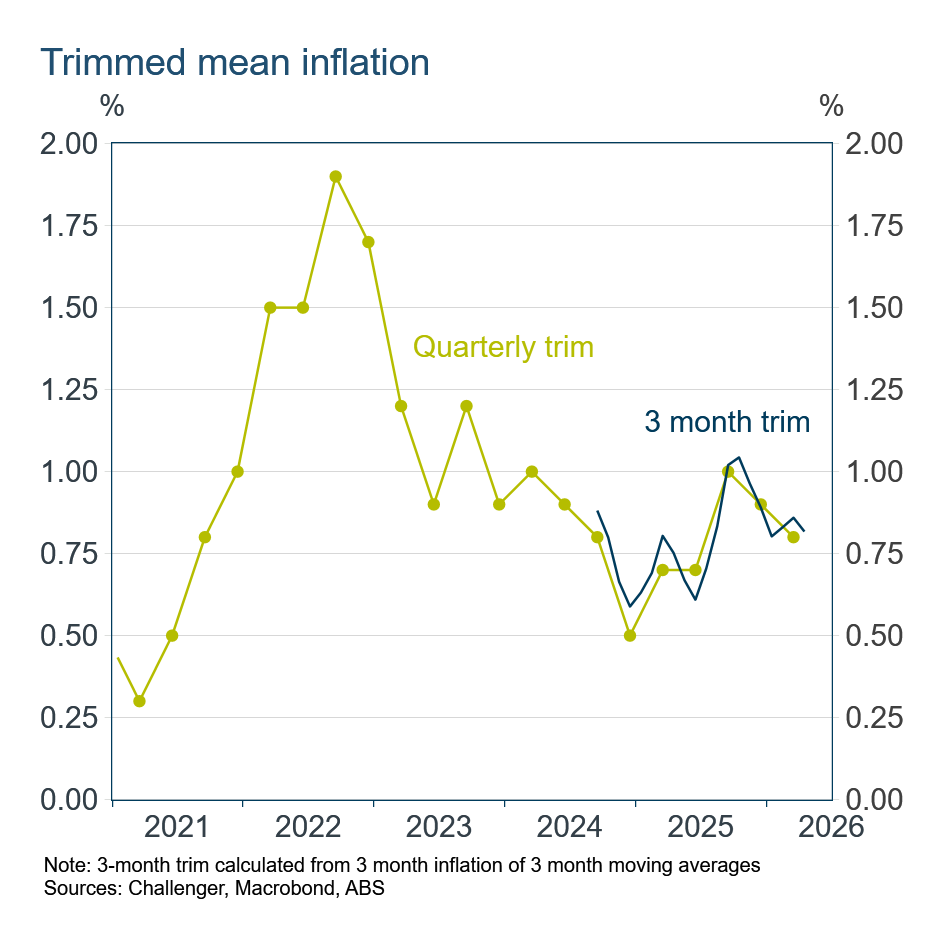

A useful measure of underlying inflationary pressures is a three-month trim I calculate from the distribution of three-month price changes for the 87 items in the CPI. This series provides a timely series akin to the RBA’s preferred quarterly trimmed mean.

Three-month trimmed mean inflation was 0.82% in April, broadly similar to the past three months and a step down from the 0.9–1.0% rates at the end of 2025. Inflation pressures clearly have eased, but underlying inflation remains well-above the RBA’s inflation target.

Inflation of market services excluding volatile items, another of the RBA’s preferred measures of demand-driven inflation, has slowed more sharply in recent months. This measure was –0.5% for three months, and is 3.0% over the year, however service prices will be much less impacted by higher oil prices and so don’t fully reflect economy-wide price pressures.

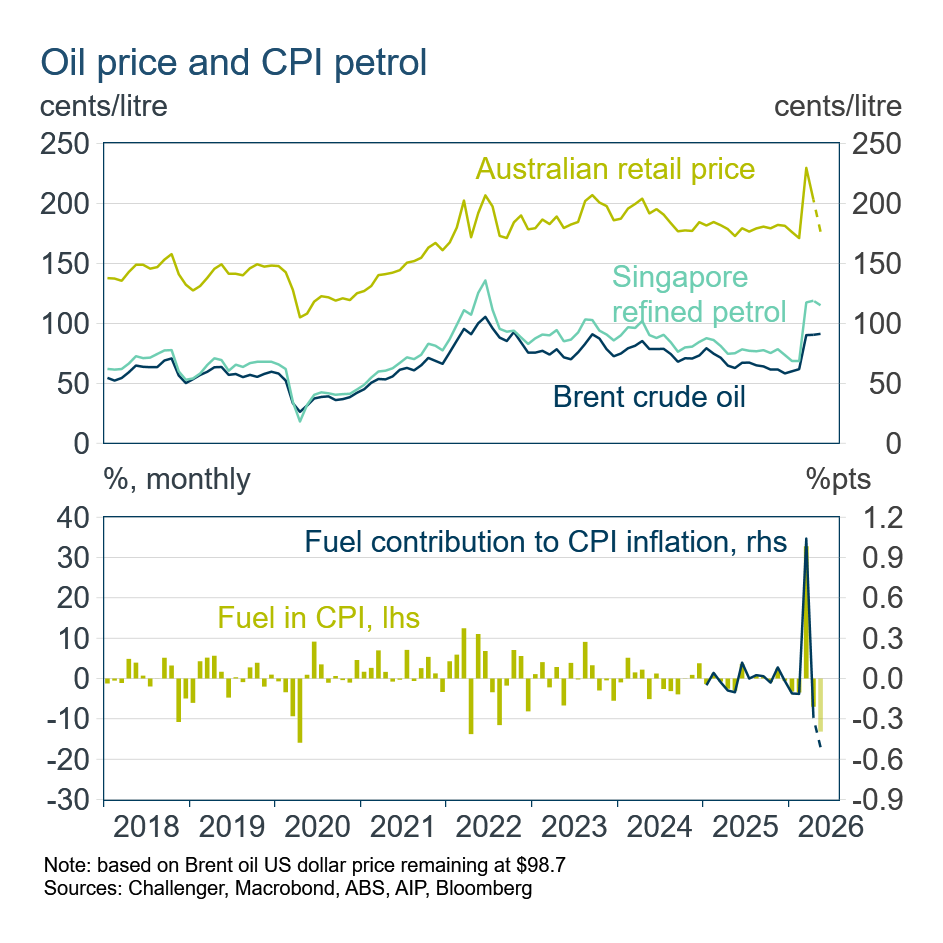

Retail petrol prices fell sharply in April as a result of the reduction in fuel excise. The fuel component of the CPI fell 7% in April, subtracting around 0.3 percentage points from inflation. Retail petrol prices have fallen further in May and fuel prices will again make a meaningful subtraction from inflation when the May CPI is released in a month.

The cut in the fuel excise is scheduled to finish at the end of June, which will increase petrol and diesel prices. Of course, like the earlier electricity rebates, the fuel excise cut may well be extended if oil prices haven’t fallen by then.

While the direct effect from higher oil prices has eased with the temporary reduction in fuel excise, and a small decline in the margins on refined fuel products, second-round effects from higher fuel prices will add to prices across the economy for months to come.

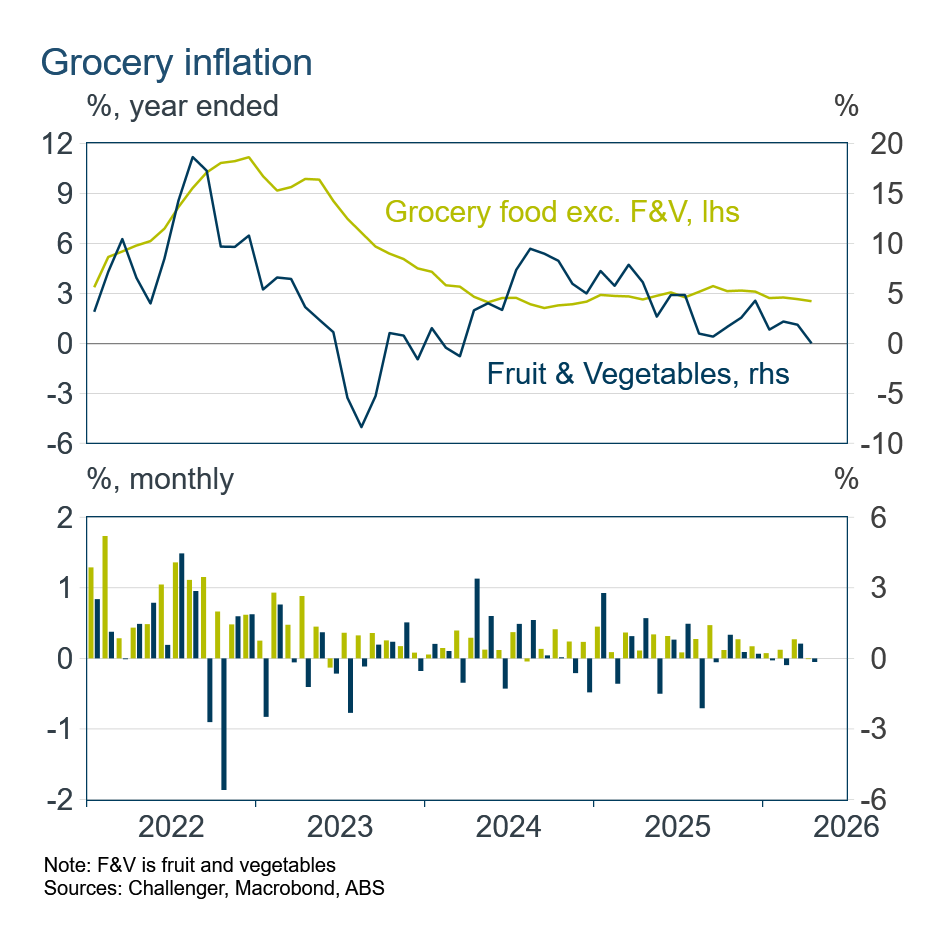

These second-round effects cannot be observed directly. However, the RBA has used detailed data on fuel use within various industries to estimate that the largest second-round impact of higher fuel prices will be on grocery prices and new dwellings.

Both fruit & vegetable, and other grocery prices, fell in April. This is consistent with a special ABS survey of businesses released yesterday that reported around half of businesses have absorbed high fuel costs, with only 11% reporting having increased their prices because of fuel costs. Businesses are likely holding off increasing prices as they wait to see if there is a resolution to the Middle East war that results in lower oil prices.

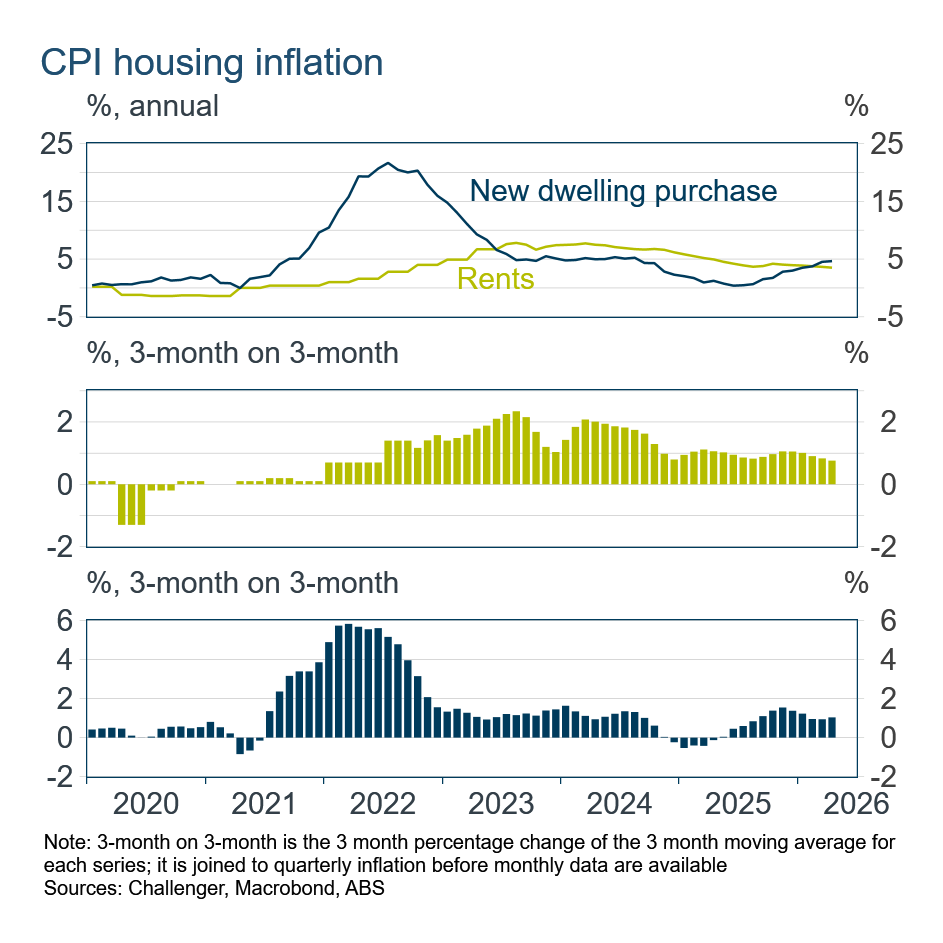

Higher fuel costs are not obvious in new dwelling prices either. Inflation in the cost of building new homes has been broadly stable this year. In other positive news for the RBA, rent inflation has continued to ease slightly.

All up the April inflation data showed inflation pressures have eased this year but remain strong. Without clear evidence of intensifying inflation pressures, it is likely the RBA will pause in June, with a further hike in August remaining possible.