Inflation unexpectedly surged: One of the RBA’s largest forecast errors

Subscribe to Macro Musing

To stay up to date on the latest economic insights, subscribe to Macro Musing on LinkedIn.

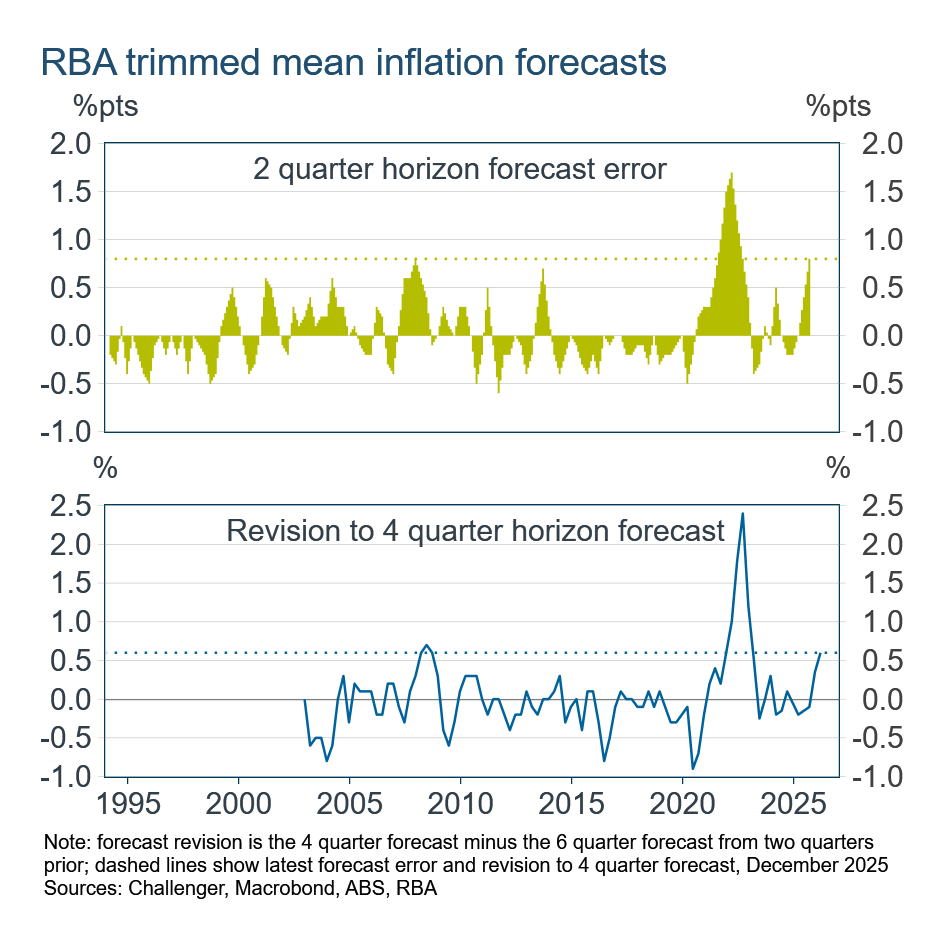

Inflation unexpectedly surged over the second half of last year. The RBA’s preferred trimmed mean measure of inflation was 3.4% over the year to December, 0.8 percentage points higher than the RBA forecast just a few months earlier in August.

This is one of the RBA’s largest forecast errors. It is as big as the underestimate in 2007 prior to the GFC, and is only surpassed by the forecast errors made in the post-pandemic inflation surge.

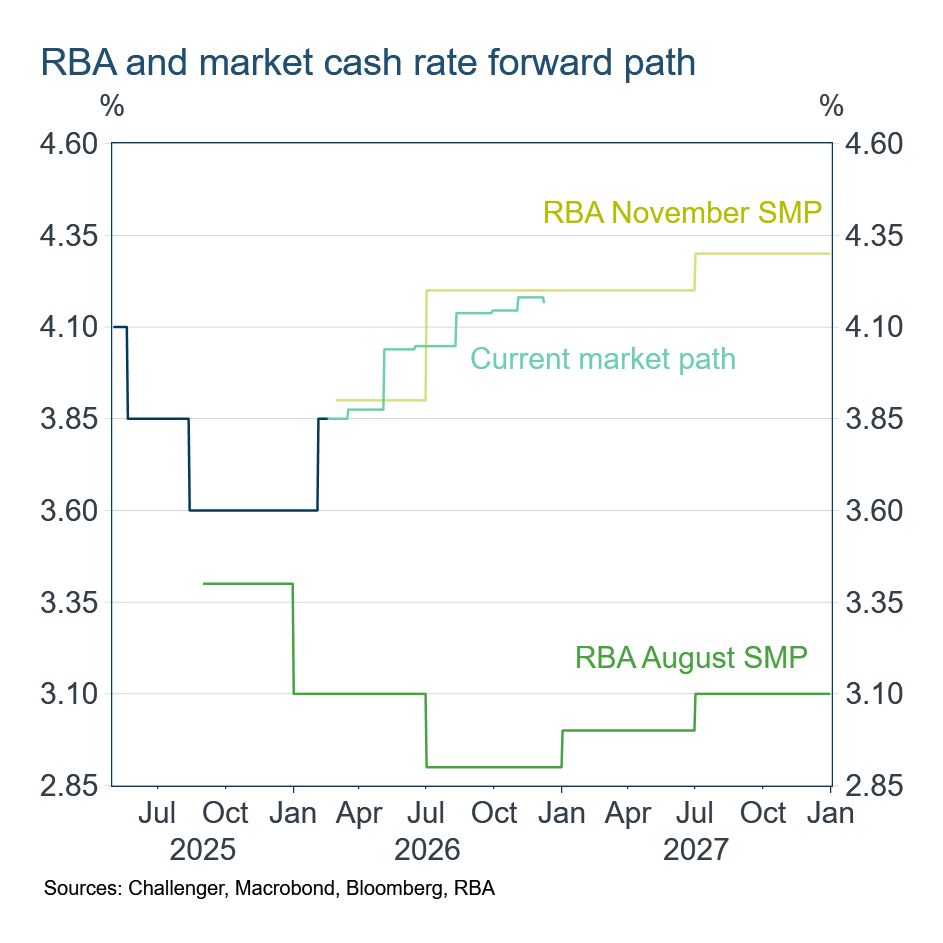

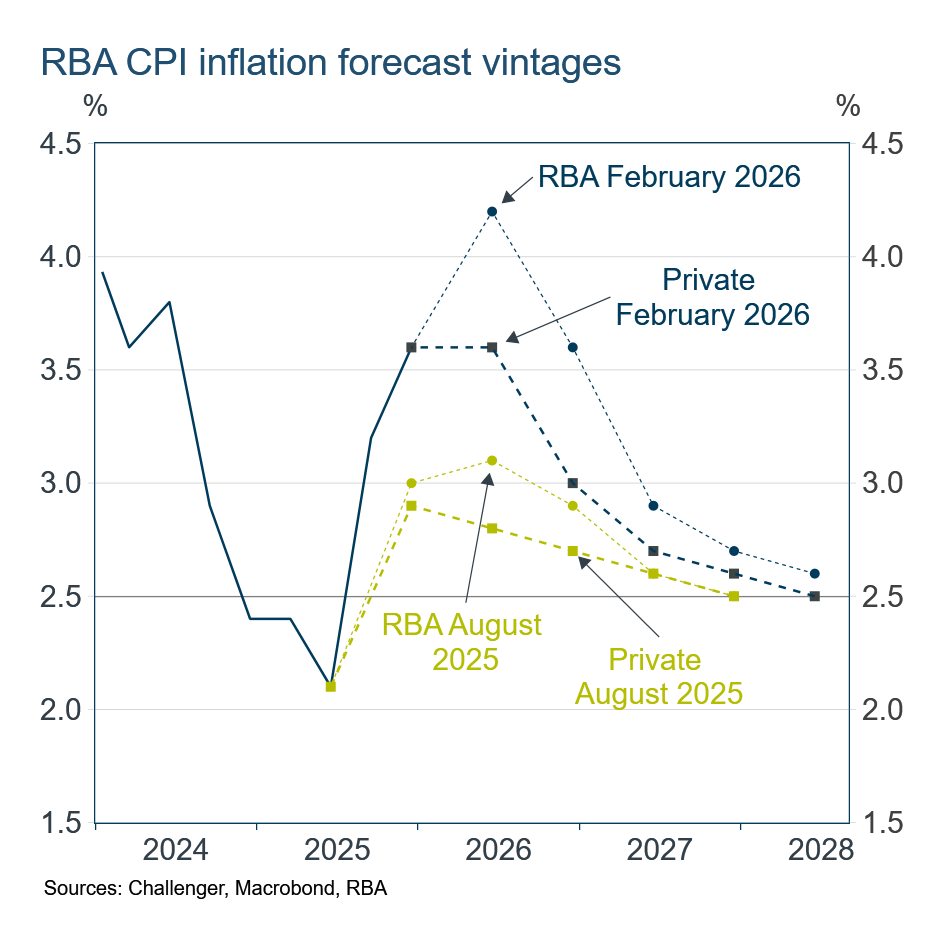

Large forecast errors frequently lead to a recalibration of forecasts, particularly for persistent variables such as inflation. In its most recent forecasts, published this month, the RBA increased its forecast for inflation over 2026 to 3.2%, 0.6 percentage points higher than it had forecast back in August. The RBA expects high inflation to persist.

Pointing out the RBA’s inflation forecast error is not picking on them. Private sector inflation forecasts were even worse. The RBA surveys private sector economists (including me) in the leadup to its Board meeting and publication of the Statement on Monetary Policy. Our median forecast had an even larger miss for inflation over 2025 than the RBA.

Following this big miss, private sector economists revised up their forecasts, but by less than the RBA. Private sector economists’ forecasts remain significantly lower than the RBA forecasts.

The big question is whether the RBA has revised its forecasts sufficiently, or whether they’ve overdone it and private forecasts might be more accurate. The RBA used a cash rate path in generating their February forecasts that had almost two more hikes on top of their February increase. Even those three hikes were not projected to return inflation to the RBA’s 2.5% target.

There isn’t a clear explanation for why inflation surged. The Australian dollar has appreciated and the price of oil has fallen, both of which would imply lower, not higher, inflation. The labour market and wages performed largely as expected. In any case, wages, the exchange rate and energy prices all affect inflation with a lag.

Alternatively, it could be that the rebound in consumer spending and the lack of spare capacity in the economy has allowed firms to increase prices, rebuilding their margins. That would suggest the RBA’s earlier policy setting – characterised by a lower cash rate than in other countries – did not slow demand sufficiently to restore balance with supply, which expanded only gradually amid weak productivity growth.

If this persistent imbalance in aggregate supply and demand has driven the resurgence in inflation it suggests that higher rates might be with us for a while longer.