Introduction to Listed Floating Rate Notes

CIM - Fixed Income

The Challenger Investment Management (CIM) Fixed Income team is a leading alternative investment manager focussed on providing clients consistent income-based solutions across public and private credit markets.

Over the past decade, many Australian investors have used bank hybrids and credit-focused Listed Investment Trusts (LITs) to access income-producing investments through the ASX. These investments have offered regular income and the convenience of daily trading, making them popular with income-focused investors.

However, these structures are not without drawbacks. Credit LITs in the Australian market have historically had periods of trading at significant and persistent discounts to their underlying asset value. In 2024 APRA announced2 that the listed bank hybrid market will be gradually phased out, meaning investors will eventually lose access to this source of income via the ASX.

Listed floating rate notes have emerged as an alternative way for retail investors to access income-generating credit investments on the ASX. They retain many of the features of a LIT that investors value, such as regular income and daily liquidity, and may include a limited first loss protection feature which is intended to reduce investor’s downside exposure during times of volatility.

What is a Listed Floating Rate Note?

A floating rate note is an unsecured debt instrument where investors receive regular interest payments calculated relative to fluctuating short-term interest rates, rather than a fixed rate. It functions similarly to a listed hybrid issued by a bank, paying a regular floating interest payments at a pre-determined margin above a reference rate, such as the Bank Bill Swap Rate (BBSW). This means that when interest rates rise, income generally rises too; when rates fall, income adjusts downward.

Unlike shares or investment trusts, floating rate notes are debt investments rather than equity investments. Investors are lending money to a corporate issuer (who appoints a professional investment manager to invest the assets of the corporate) and are entitled to receive interest payments and the return of their capital at maturity.

What sits behind a Listed Floating Rate Note?

The issuer uses the money raised from noteholders, often alongside its own equity capital, to invest in a diversified portfolio of income-producing assets such as public and private credit, property or infrastructure investments. The income generated by this underlying portfolio funds the interest payments from the issuer to noteholders.

Liquidity and pricing

Unlike most debt instruments which are traded over the counter and are only available to institutional investors, listed floating rate notes are ASX-listed and trade on the exchange. Once issued, a note’s market price will fluctuate according to buying and selling activity/demand and supply forces in the market. Accordingly, there may be times where the market price differs from the face value of the notes.

Common structural features of Listed Floating Rate Notes

While structures vary by issuer, many listed floating rate notes share the following features:

Fixed term

Notes are issued with a defined maturity date, at which time investors should be repaid their face value. Some notes also include an optional early call date, allowing the issuer to repay investors earlier. In certain cases, the interest margin may increase if the note is not redeemed at the first call date, called a “step up” feature, which encourages repayment.

First loss buffer

Note structures may include junior layers of debt or equity capital that sit below holders of listed notes. These junior layers are designed as a buffer to absorb losses first, helping to protect note investors and reduce the likelihood of capital loss to noteholders in periods of portfolio stress.

Pull to par

As a note approaches maturity, its market price typically moves closer to its face value, or “par”. This is because investors expect to be repaid the face value at maturity. This feature can help reduce price volatility over time compared with perpetual or equity‑style investments.

Underlying portfolio

The income paid to investors is ultimately generated by the performance of the underlying investment portfolio. Portfolio composition, diversification, and risk profile can vary meaningfully between issuers and should be considered carefully by investors.

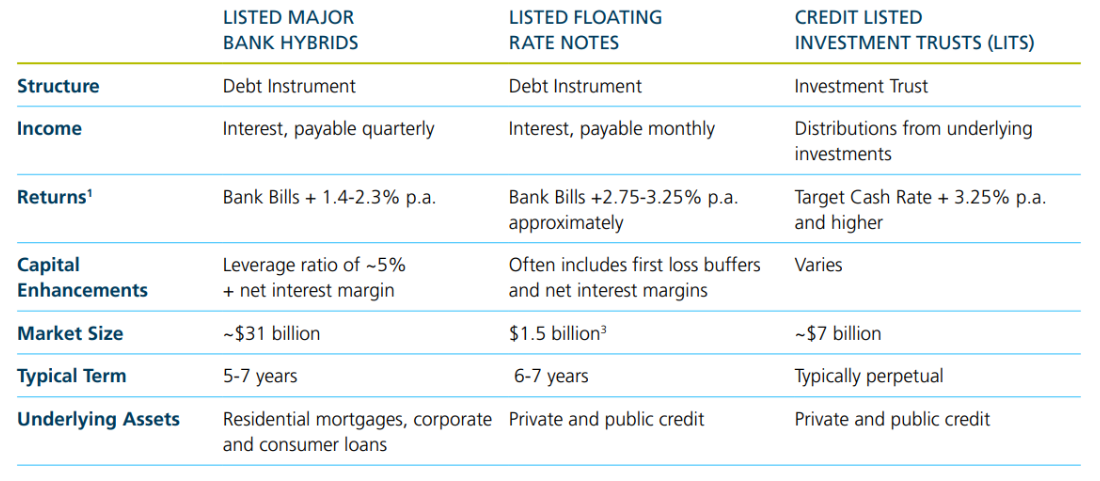

How do Listed Floating Rate Notes compare to bank hybrids and listed investment trusts?

When compared with traditional bank hybrids and credit‑focused LITs, listed floating rate notes typically offer features of both:

- Like hybrids, they offer floating‑rate income and ASX liquidity

- Unlike hybrids, they are not issued by banks and are not designed to convert into equity

Unlike LITs, they are debt instruments with a defined maturity date and carry the obligation to pay regular interest payments

While returns, risk and structure vary by issuer, listed floating rate notes are generally designed to provide regular income with more downside protection than equity‑style credit vehicles.

What are the risks of investing in a floating rate note?

Investors are exposed to credit and default risk, as returns depend on the issuer’s ability to meet its obligations and the performance of the underlying credit portfolios, which may be affected by defaults or economic downturns. Market prices may fluctuate with changes in credit spreads and investor sentiment, meaning notes may trade above or below face value. While the notes are listed, liquidity can vary and investors seeking to exit quickly may need to accept a lower price. In addition, a decline in interest rates would reduce the level of income generated from the investment.

Challenger IM Capital Limited (a wholly owned subsidiary of Challenger Limited) issued unsecured notes quoted on the ASX known as the Challenger IM LiFTS 1 Notes (LiFTS) in September 2025. For further information and to subscribe to receive updates on the LiFTS, please visit Challenger IM LiFTS 1 Notes: Listed Floating Rate Term Securities (LiFTS) - Challenger Investment Management.

1. Major Bank Hybrid returns based on trading margins at 30 June 2025. Excludes any hybrids callable in 2025.

2. https://www.apra.gov.au/news-and-publications/apra-to-phase-out-at1-as-eligible-bank-capital

3. As at April 2026.

Disclaimer

This material is provided for general information purposes only. It is not a prospectus, product disclosure statement, disclosure document or other offer document under Australian law or under any other law. This material is not, and does not constitute, financial product advice, an offer to sell or the solicitation, invitation or recommendation to purchase any securities and neither this material nor anything contained within it will form the basis of any contract or commitment. This material does not directly or indirectly contain any offer or intended offer of securities and is not intended to induce anybody to make an investment in any securities. To the extent permitted by law, no liability is accepted for any loss or damage as a result of reliance on this information. No representation or warranty, express or implied, is made as to the fairness, accuracy, adequacy, reasonableness, completeness or reliability of any statements, estimates or opinions or other information contained in this material. Any forward-looking statements, including projections, guidance on future revenues, earnings and estimates, are provided as a general guide only and should not be relied upon as an indication or guarantee of future performance.

Challenger IM Capital Ltd (ACN 687 738 263) (Issuer) is the issuer of the Challenger IM LiFTS 1 Notes (Notes) which are available on ASX under ticker CIMHA. The Prospectus for the offer of Notes and the Target Market Determination available at www.fidante.com/challenger-im-lifts should be obtained and read in their entirety by an investor before making a decision to acquire the Notes. No cooling-off rights will apply to an investment in Notes. The Issuer is not licensed to provide financial product advice in relation to the Notes and this information does not take into account any person’s objectives, financial situation or needs. You should consider the appropriateness of this information, in light of your own objectives, financial situation or needs before acting.

The Notes are not guaranteed, are not bank deposits and you risk loss of principal and interest.

Related content

Stay informed

Sign up to our free monthly adviser newsletter, Tech news containing the latest technical articles, economic updates, retirement insights, product news and events.