Federal Budget webinar

Hear from the Technical Services Team as they discuss and identify the impact of budget announcements on your retiree and pre-retiree clients.

Macro Musing Live

Join us for our CPD-accredited webinar as Chief Economist Dr Jonathan Kearns unpacks the latest forces shaping the global macro landscape. From rising oil prices to slowing growth, gain insights into what these shifts could mean for markets and investors.

Read Dr Jonathan Kearns, Chief Economist and Head of Regulatory Affairs, insights on the 2026-27 Federal Budget.

The Budget was framed around goals of addressing intergenerational equity and improving access to housing for first home buyers. It did not deliver expensive cost-of-living relief, but equally the Budget remains in deficit for the next four years, with The Budget resulting in only a small reduction in the cumulative deficit. This is not a Budget that will add to inflation through new spending, but nor is it restrictive in a way that would reduce pressure on the RBA to restrain aggregate demand.

Tax changes

The focus of the Budget is on three tax changes which are projected to raise around $7 billion per year in four years' time.

Capital Gains Tax (CGT) will change from the current 50% discount to an indexed base for all assets. There is a 30% floor on the effective tax rate on capital gains – so if the taxed amount (the difference between the sale price and the indexed purchase price) multiplied by a person's marginal tax rate produces an effective tax rate of less than 30% a tax rate of 30% is still applied. This is designed to avoid people realising capital gains only when they stop work and face a lower marginal tax rate. Investors in new builds will have the option of using either the 50% discount method or indexation. The new tax rules come into effect from 1 July 2027 for all assets purchased from now. Existing owners can obtain a valuation as at 1 July 2027 to set the capital gain under the old 50% discount method before applying the indexed method thereafter.

Superannuation funds retain their existing one-third discount on capital gains.

Negative Gearing will be restricted to new builds only, with any existing dwellings purchased after Budget night only able to be negatively geared until 1 July 2027. Income losses on an asset can be offset against future capital gains. Existing investors will be grandfathered, enabling them to continue to use negative gearing. This will create disincentive for existing investors to sell their property as doing so would relinquish this tax benefit, which could depress housing turnover.

Treasury estimates that the CGT and negative gearing change will result in housing prices being 2% lower than otherwise after a couple of years.

Discretionary trusts will have their minimum tax rate lifted to 30% from 1 July 2028.

No cash splash

There was no cost-of-living relief in the Budget to add to the reduction in fuel excise. There was a small, permanent Working Australia Tax Offset of up to $250 but this only starts in 2027–28 and applies only to wages not investment income.

Defence spending will grow significantly over the coming decade increasing in total by $53b as the Government aims to get defence spending to 3% of GDP.

The net impact - is it wishful thinking?

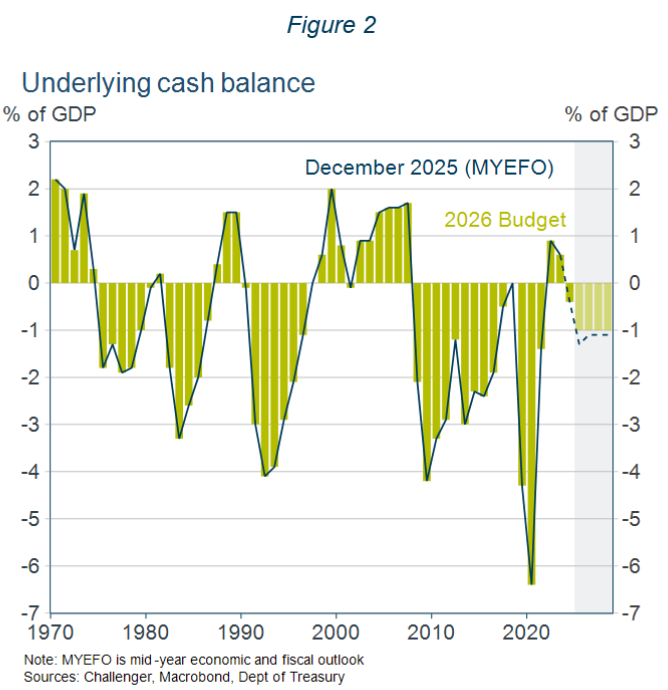

The Budget deficit over the current and next four financial years is now projected to total $150b, a reduction of $45b from the December budget update (Table 1).1 While this seems impressive, the improvement rests heavily on projections for the 2029–30 fiscal year which deliver a $27b improvement, with $19b coming from policy savings. Much of this projected saving will come from the reductions in planned NDIS spending announced before the Budget. The challenge for the Government will be to deliver on this spending restraint. The reduction in spending sees the projected deficit for 2029–30 fall sharply from 1.5% of GDP to just 0.7% of GDP.

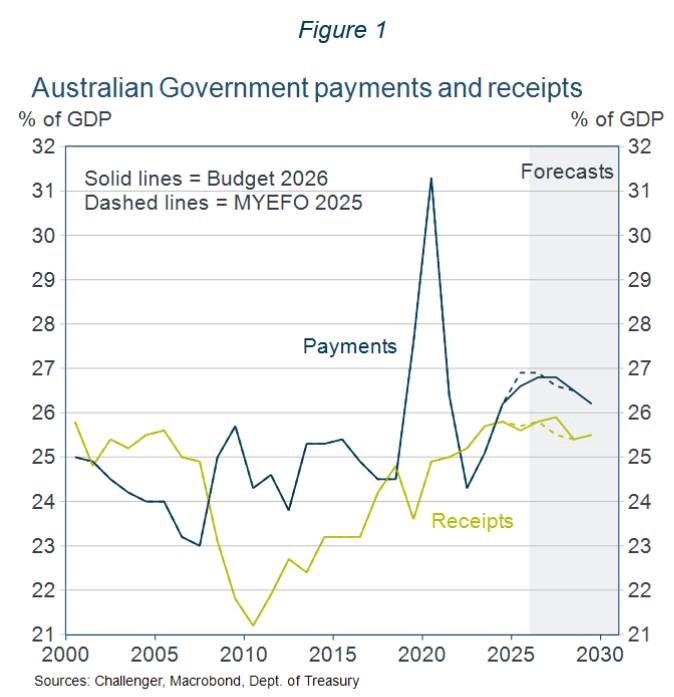

By contrast, changes in spending and revenue in the first four years are small (Figure 1). Collectively, they deliver a combined improvement of only $18b, with the deficit reduced by only 0.1% of GDP in each of the next three years (Figure 2).

Table 1: Policy measures and other variations contributions to change in Budget balance

2025-26 | 2026-27 | 2027-28 | 2028-29 | 2029-30 | |

|---|---|---|---|---|---|

| $ billion | |||||

| 2025-2026 Budget | -42.2 | -35.4 | -37.1 | -37.0 | |

| 2025 MYEFO | -36.8 | -34.3 | -36.2 | -36.0 | -52.1 |

| % GDP | -1.3 | -1.1 | -1.1 | -1.1 | -1.5 |

| Parameter & other variations | 13.8 | 9.3 | 7.5 | -1.5 | 7.6 |

| New policy measures | -5.3 | -6.5 | -2.3 | 3.1 | 19.3 |

| New projected budget surplus | -28.3 | -31.5 | -31.0 | -34.4 | -25.3 |

| % GDP | -1.0 | -1.0 | -1.0 | -1.0 | -0.7 |

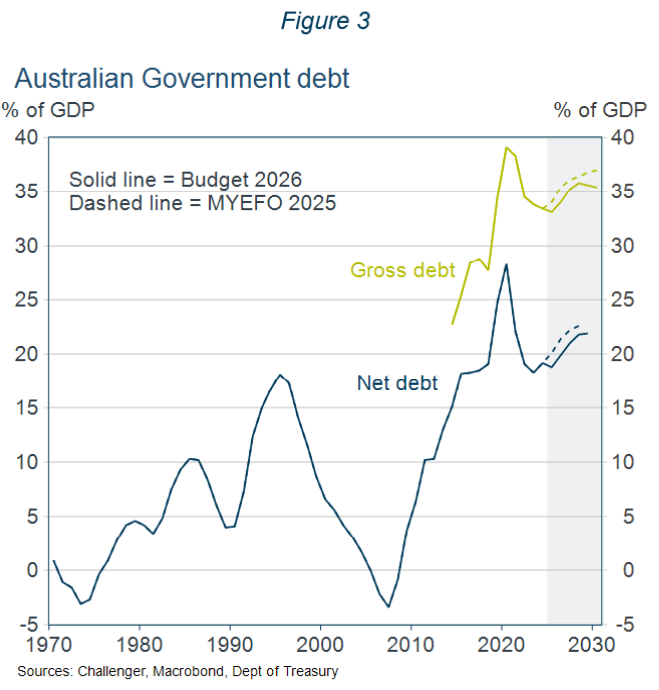

Government debt

The profile for gross debt is lower, reflecting a small decline over the past year, but is projected to increase and peak at 36% in three years' time (Figure 3). Net debt similarly has a lower profile reflecting past improved performance but continues to drift up over coming years.

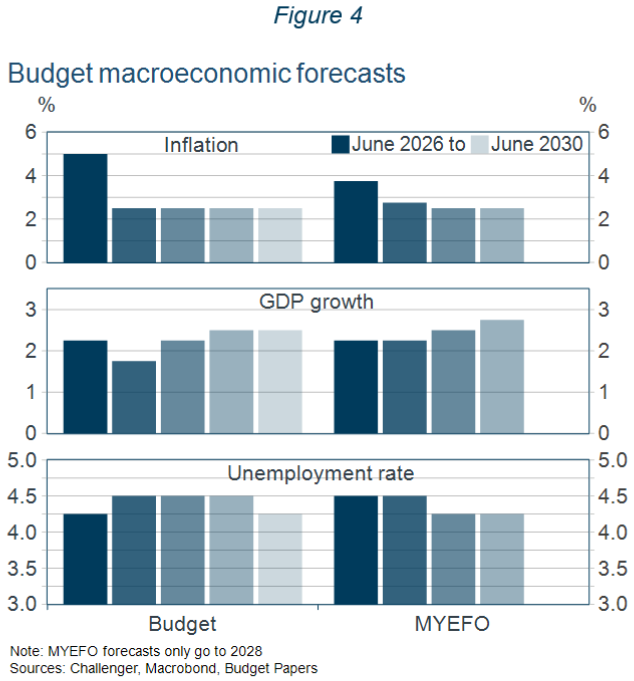

Economic outlook

Higher oil prices have pushed the inflation forecast up to 5% for the year to June 2026 (Figure 4). But an assumption that oil prices fall back results in inflation returning to 2.5% the following year, where it is assumed to remain in subsequent years. This broadly aligns with the RBA forecasts released earlier this month.

Growth in GDP in the 2026-27 financial year is expected to be 1.75%, less than the 2.25% forecast in the December update. However, the slowdown is expected to be short-lived, with growth recovering to 2.25% in the subsequent year. The unemployment rate is projected to peak at 4.5%, the same as the in December forecasts. These growth and unemployment forecasts are a bit more optimistic than the RBA's, although the differences can be accentuated because the Budget contains only annual forecasts.