Managing inflation for retirees

Signup for Tech News

Register to receive technical updates on retirement income and aged care advice from the Challenger Tech team.

Inflation has been increasing again in Australia over the past year. This was happening before the oil price spikes from the latest Middle East conflict. Higher inflation has heightened concerns for retirees over how they can keep up with the cost of living. Different investments are available that can help with inflation, and retirees, and their advisers, should understand how these manage the different elements of inflation risk.

Inflation resurgence impacting retirees

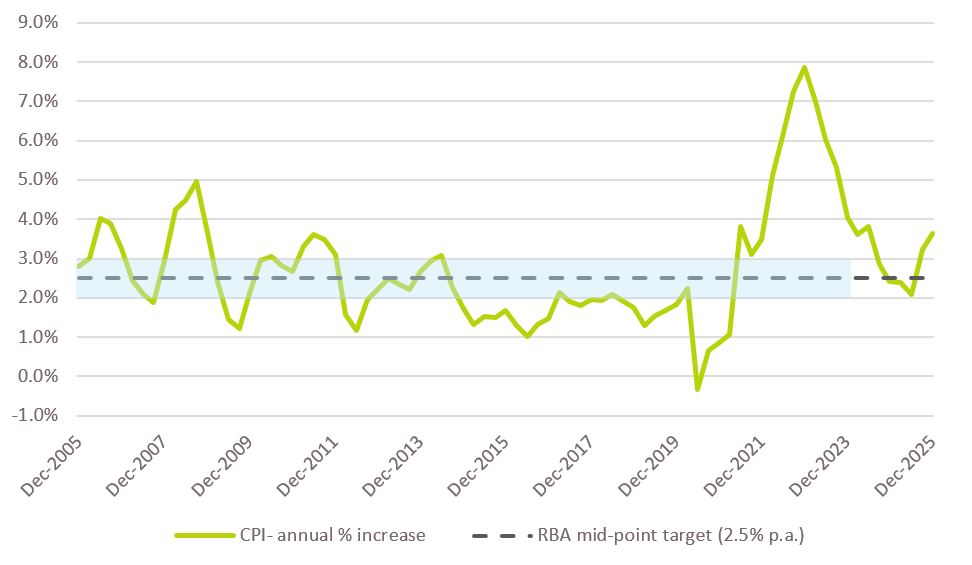

Prior to 2020, Australia had enjoyed a long period of sustained low inflation, with price increases often undershooting the Reserve Bank of Australia (RBA) 2-3% target range. The economic shock of COVID squashed inflation even further, but the rebound, combined with impacts on global trade from Russia’s invasion of Ukraine pushed inflation to almost 8% in 2022. Inflation declined through to mid-2025 as supply chain disruptions were resolved, energy prices stabilised and higher interest rates reduced economic demand. However, inflation pressures have increased since then and the RBA had raised interest rates, even before war in the Middle East, to reduce inflationary pressures.

The recent surge in oil prices from the Middle East war is only adding to inflationary concerns. In Challenger’s latest Happiness Index 2026 update, the cost of living was the largest concern about future spending in retirement with 67% highlighting the importance to plan for the cost of living in the future.

Figure 1 Australian Inflation rates 2005-2025

In practice, there are two elements to inflation that need to be managed in any retirement portfolio. Both involve reducing the impact of inflation on the lifestyle that a retiree can afford by having the right components in the overall retirement portfolio. The two elements can be broadly described as expected inflation and an unexpected increase in inflation. While both elements will push up the cost of living, managing these two different inflation risks requires different approaches.

How does inflation impact a retiree?

Inflation refers to the rising costs of goods and services over time. It reduces the purchasing power of a retiree’s income. Inflation risk arises because the level and impact of future inflation is unknown. Inflation expectations can be factored into a retirement income strategy, but there needs to be a plan for what happens if inflation does not match the built-in expectations.

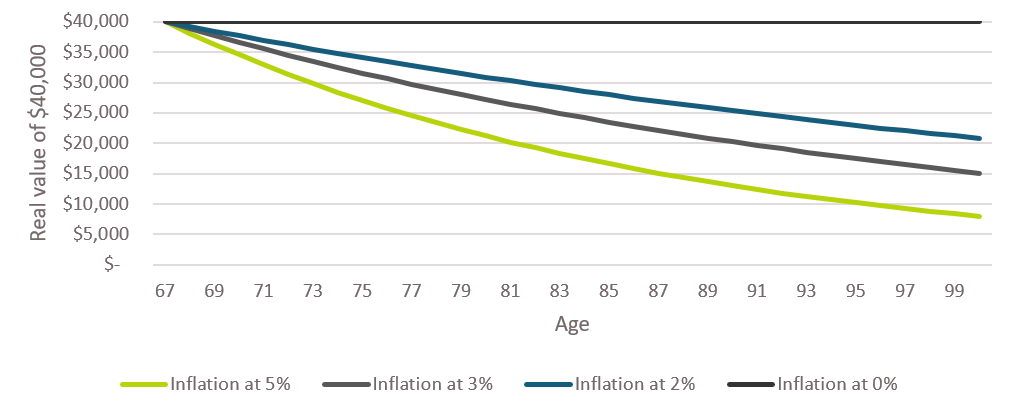

The impact of inflation over a retiree’s lifestyle can be dramatic, even with modest inflation. Figure 2 below highlights how inflation erodes the real value of income for a retiree. There isn’t much difference in the early years, but the impact compounds over time. Even modest rates of inflation will hamper a retiree’s lifestyle. With inflation of only 2% a year, one-quarter of the value of the nominal income is lost after only 14 years. The risk of higher inflation is stark; 5% a year would halve the value of payments over the same period.

Figure 2: The impact of different inflation rates on $40,000 of retirement income per year

The erosion of value can have a severe impact on a retiree’s lifestyle. Some reduction in lifestyle might be OK. Research by David Blanchett in the US1 and the Grattan Institute2 have shown that retirees tend to spend less (in real terms) over time. However, the fall in spending is typically less than inflation, which means that nominal spending increases. Even if a decline in living standards is intentional (i.e. less spending on discretionary items), retirees still need to manage inflation to afford the lifestyle they desire.

Managing expected inflation

Protecting against inflation in accumulating savings requires investment returns high enough to offset the inflation over time. Some investments, like equities have higher risks and market volatility but can provide high returns on average that have compensated for rising prices over the long term. Others, such as unlisted property while still contending with the fickle property market, can be of benefit as property prices often increase in inflationary periods, potentially increasing returns when inflation is higher.

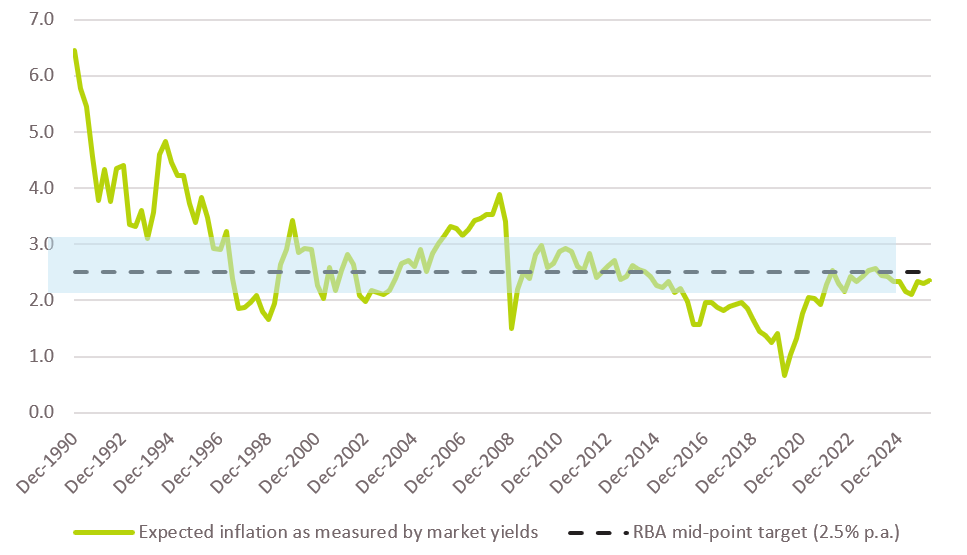

Bond investments are more exposed to inflation because the yield to maturity doesn’t change after purchase unless they are CPI-linked bonds. This doesn’t mean that bonds can’t help with managing inflation. Buyers of bonds know about the potential impact of inflation. So, the price they pay, and the yield they demand, will depend on the average inflation rate that they expect in the future. This is central to bond markets and is monitored by the RBA in monitoring inflation expectations. Figure 3 shows the bond market’s inflation expectations published by RBA back to 1990.

Figure 3: RBA measure of inflation expectations from the bond market

Source: RBA

Breakeven inflation, as it is known, is simply the yield on a normal bond, less the yield on a matching CPI-linked bond. If inflation were to match breakeven inflation until the maturity of both bonds, then the return on each bond would be the same. As demand for nominal and CPI-linked bonds adjusts depending on their expected returns, the breakeven inflation rate tends to adjust to be the market’s inflation expectation.

As Figure 3 shows, expected inflation has generally been in the 2-3% target band of the RBA since the mid 1990s, reflecting the policy target that was confirmed at that time. It dropped lower as COVID hit markets, but the long-term expectation is currently within the target band. This has been the case even as inflation rose to 8% and it hasn’t changed much with the latest increase in inflation. Markets are expecting that the actions of the RBA will eventually stabilise inflation.

These inflation expectations can be managed by exposure to assets with higher expected long-term returns along with higher exposure to the risk and return trade off and market volatility. But there is an additional challenge to manage inflation risk. While lower than expected inflation will mean a higher living standard so that isn’t much of a problem, what if the inflation rate in the future is higher than what is expected? Can you prepare for the unexpected inflation shock?

Unexpectedly higher inflation could be called one of the ‘known unknowns’ in the language of Donald Rumsfeld. Everyone knows that there will be inflation and that it can be damaging to investors’ returns, and while we might have an expectation of what it will be, no-one knows what it will be ahead of time. Managing this takes more than just high returns. They might not be high enough or they be late, with sequencing risk from the low returns before the higher returns. The inflation shock might even push markets down as inflation rises like they did in 2022. What you need is an investment allocation that benefits from correlation with higher inflation, or even better, automatically adjusts through a linkage to the CPI.

Managing inflation risks to retirement income

A successful retirement needs an effective retirement income strategy. Part of this strategy will include the Age Pension for many Australians. Over 60% of Australian retirees currently receive a full or part Age Pension. The Age Pension is linked to the higher of inflation or average wages which helps manage inflation risks. However, the share of retirees receiving a pension is expected to decline in the coming years as average super balances continue to grow meaning that more retirees will be exposed to inflation risk and need strategies to manage that risk.

Another consideration for retirees is the composition of their spending and so the type of inflation they need to protect against. At older ages, some discretionary spending drops, so inflation on this consumption might be OK with less protection, but they might be more exposed to wage driven inflation in healthcare costs. It is important to have some inflation cover for the essential components of a retiree’s lifestyle.

Those with only a part Age Pension, or those who receive no Age Pension, could benefit from an investment that explicitly manages inflation risk, by protecting against higher-than-expected inflation. For most retirees, this protection is only needed for a small but important component of the retirement portfolio. The rest of the portfolio can aim to be protected from expected inflation through the focus on long term higher expected returns, albeit with higher risks and market volatility.

When saving for retirement, investors can try to protect their capital from inflation by aiming to grow their assets faster than inflation. In retirement, however, inflation risk has a different impact on generating retirement income. Retirees can improve their (inflation-adjusted) retirement outcomes by using some inflation-linked assets in addition to investments with higher risk, market volatility and expected long term returns.

1 Blanchett (2013). Estimating the true cost of retirement. Morningstar.

2 Daley, J., Coates, B., Wiltshire, T., Emslie, O., Nolan, J. and Chen, T. (2018). Money in retirement: More than enough. Grattan Institute.

Past performance information is not a reliable indicator of future performance of that company or product. Any reference to past performance in this article is intended to be for general illustrative purposes only.

Related content

Stay informed

Sign up to our free monthly adviser newsletter, Tech news containing the latest technical articles, economic updates, retirement insights, product news and events.