Prospective tax changes and asset prices

Subscribe to Macro Musing

To stay up to date on the latest economic insights, subscribe to Macro Musing on LinkedIn.

Prospective tax changes and asset prices

Download the full article below.

With the Budget one week away, it seems almost certain that changes to capital gains tax (CGT) and possibly negative gearing will be announced. These changes are part of the Government’s plans for tax reform and to address intergenerational equity by increasing taxation on property investors to improve housing affordability for younger generations. This note briefly summarises the likely changes before considering the possible impacts, including on asset prices.

Two changes have been widely discussed

Replace the capital gains discount, which is currently 50%, with indexation, under which the capital gain is calculated as the sale price less the inflation-indexed purchase price. This is how CGT was calculated during 1985–1999. Earlier speculation centred on a reduced discount (for example, 33%), but recent media reports suggest the Government has settled on indexation.

Reports suggest the CGT change will apply to all assets, including shares, in contrast to earlier speculation that it would apply only to property.Also critical is whether current asset holders are grandfathered. Recent media reports suggest future CGT would be apportioned according to how many years an asset was held under the old (50% discount) and new (indexation) regimes. The new rules could commence on Budget night (12 May) or at the start of the new tax year (1 July).

- Restrict negative gearing, possibly by limiting the number of properties a taxpayer can negatively gear (for example, to two properties), or by ring-fencing all negative gearing losses from labour income.

Given the changes to capital gains tax are much more likely and have broader implications, this note focuses on that change.

Implications for housing

- The impact on housing prices is likely to be less than many people might expect, with most estimates suggesting very small price falls, perhaps 1–2%1. The small impact is calculated from the change in the value of the tax benefits for investors relative to the total value of the housing stock. Put simply, only a small change in prices is needed to induce new owner occupiers into the market as investors drop out.

- Not grandfathering would avoid suppressing turnover. With grandfathering, existing property investors would be less willing to sell if doing so would forgo their more generous tax treatment.

- Investors who have large existing capital gains and expect smaller gains going forward (perhaps because of the tax change), could have an incentive to realise gains sooner so that a smaller share of their total gain is taxed under the new regime. There could be quite a few investors in this category, which would boost turnover in the near term.

- The impact on supply is likely to be tiny given the small price impact, and any reduction in investor demand would be offset by stronger demand from first home buyers (because the number of households is unchanged).

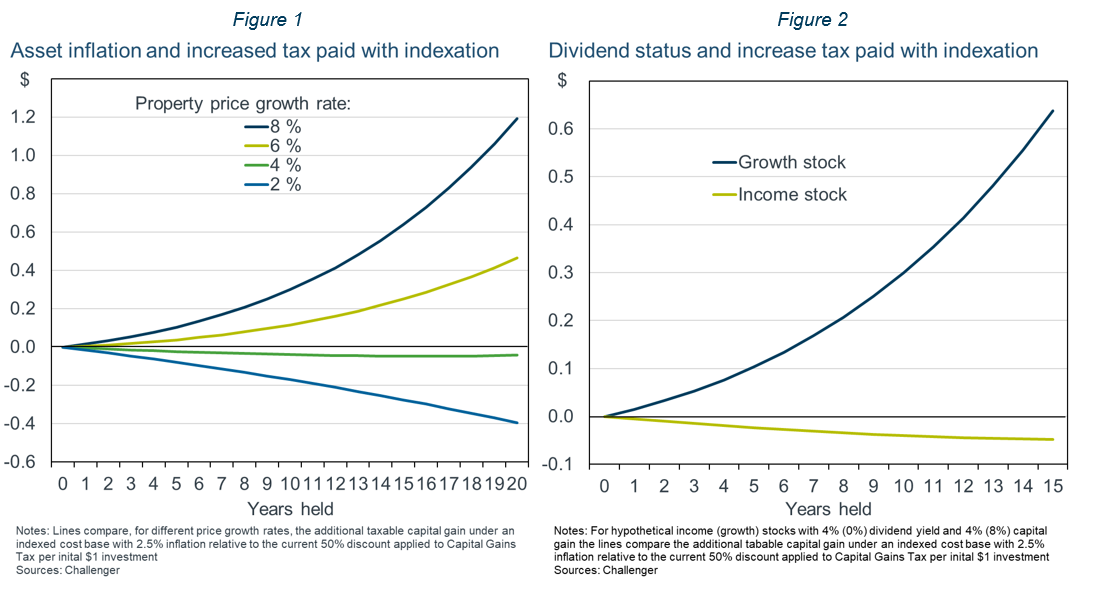

- Investors will probably pay more tax under indexation, although it depends on the rate of inflation and property price growth. Assuming inflation averages the RBA’s target of 2.5% over the holding period, the income subject to CGT under the 50% discount and indexation is very similar for 4% house price growth (Figure 1). Note that this 4% rate is less than 2.5% divided by 50% because of compounding. For higher rates of price growth, more income is taxable under indexation than under the 50% discount regime. With historical average house price growth of 5–6%, the new regime will progressively raise more revenue.

Implications for equities

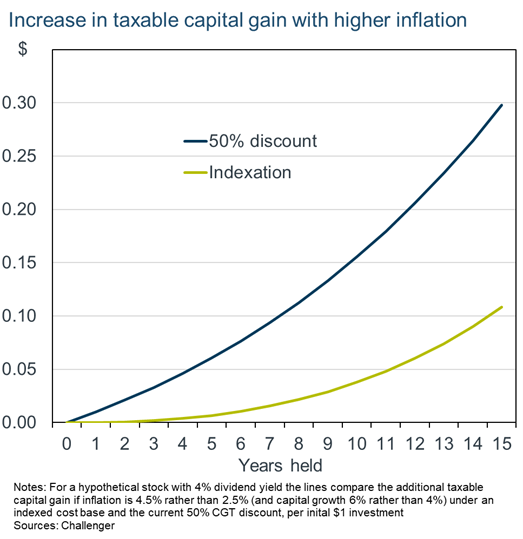

- Indexation typically results in higher taxation of capital gains and so shifts the tax relativities of growth (paying no dividends) and income (dividend-paying) stocks. For example, for two stocks with an 8% total return, the growth stock will have a larger increase in the taxable capital gain than an income stock (with a 4% dividend yield) (Figure 2). This would reduce the tax disincentive to pay dividends that companies face. Higher investor demand could increase the prices of income stocks relative to growth stocks.

- A less favourable tax treatment of growth stocks would reduce the relative tax disadvantage for wealthy retirees – those with superannuation balances over $2 million and non-superannuation assets – who hold income stocks.

- While investors will likely pay more tax under indexation, in a period of high inflation there is some comfort that it provides more insulation from inflation shocks. If nominal – but not real – share prices rise with inflation, the 50% discount regime effectively compensates investors for only half of the price increase that reflects inflation, whereas indexation provides a larger allowance for inflation (Figure 3). 2

- Leverage can reduce income and increase capital gains on a portfolio, so it will be relatively less advantageous under a regime that taxes capital gains more aggressively.

Other implications

- The impact on Budget revenue depends on the extent of grandfathering. Applying the new regime only to capital gains that accrue going forward is a pragmatic trade-off between grandfathering – which would mean a very slow increase in revenue – and applying the new regime to past purchases – which would raise revenue faster but would be far more controversial as a retrospective tax change.

- In practice, this transition is likely to be implemented as a weighted average of the old and new regimes, with weights based on holding periods before and after the change. This method is simpler, less subject to fraud, and avoids the need to value many assets at the regime change date.

- However, revenue could be brought forward temporarily improving the Budget position if asset sales rise as investors seek to crystallise large existing capital gains before they are diluted under the less favourable new regime.

- There is no discernible implication for monetary policy, given the negligible impact on aggregate demand from very small changes in asset prices and housing supply.