Quantifying the technical benefits of Challenger CarePlus

Moving into an aged care facility can often be unexpected or unplanned. However, a well-structured aged care advice plan can not only help with managing aged care costs to ensure sustainable cash flow but also provide financial peace of mind for loved ones left behind. Challenger CarePlus was introduced as a solution-based offering that provides clients with regular payments for life and provides 100% of the investment amount to nominated beneficiary(s) or their estate in the event of death1.

CarePlus is comprised of an annuity and an insurance component and can be offered to clients receiving/planning to receive Government-subsidised aged care services. Together, these two products also offer a range of technical benefits which can, in certain cases, deliver clients, reduced aged care costs, reduced tax payable and estate planning certainty. This article quantifies the technical benefits of CarePlus with the help of a case study.

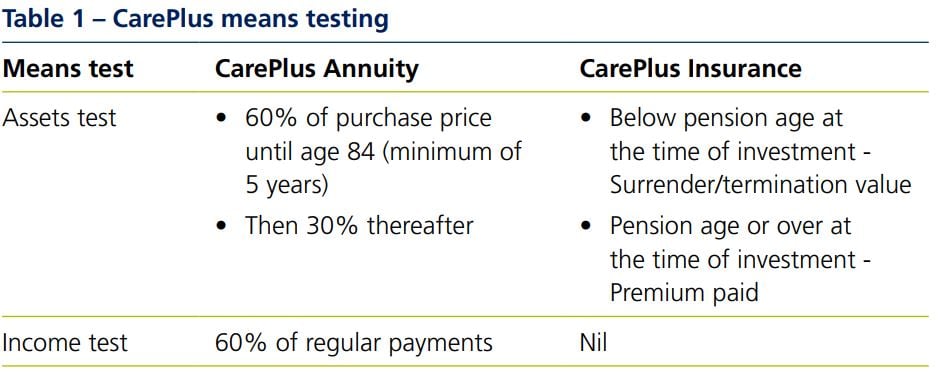

Interaction with social security and aged care rules Centrelink assesses the two components of Challenger CarePlus – CarePlus Annuity and CarePlus Insurance separately and the total assessment is the sum of the assets and income assessments for both the CarePlus Annuity and CarePlus Insurance. This also applies to the means test assessments used to calculate aged care fees. For social security and aged care means testing, CarePlus investments made from 1 July 2019 are assessed as outlined in Table 1:

Age Pension benefit

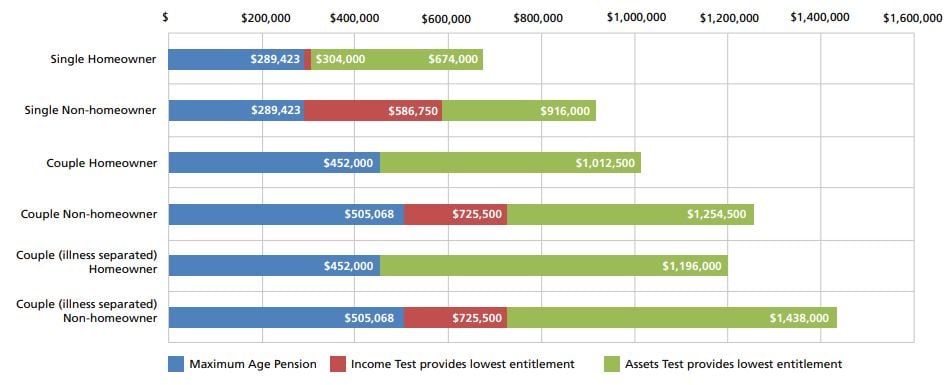

The concessional assessment of CarePlus annuity under the assets test can help increase Age Pension entitlements for asset tested clients. Asset tested clients on part pension may see an increase in their Age Pension rate and the ones who didn’t receive any Age Pension due to being slightly above the cut-off threshold may start to receive the Age Pension and access benefits under the associated Pensioner Concession Card.

For every $1,000 worth of assets not being assessed, an asset tested client can increase their Age Pension by $78 p.a. For income tested clients, the assessable income from CarePlus (equal to 60% of regular payments) will (with current CarePlus and deeming rates) generally exceed deemed income on financial investments. The chart below explains the interaction between the income and assets tests and provides a snapshot of the dominant means test determining the rate of Age Pension payable. It takes into assumption that all assets held are financial assets and deemed under the Income Test. Rates and thresholds as at 20 March 2024.

Strategy zones

Means Tested Care Fee benefit

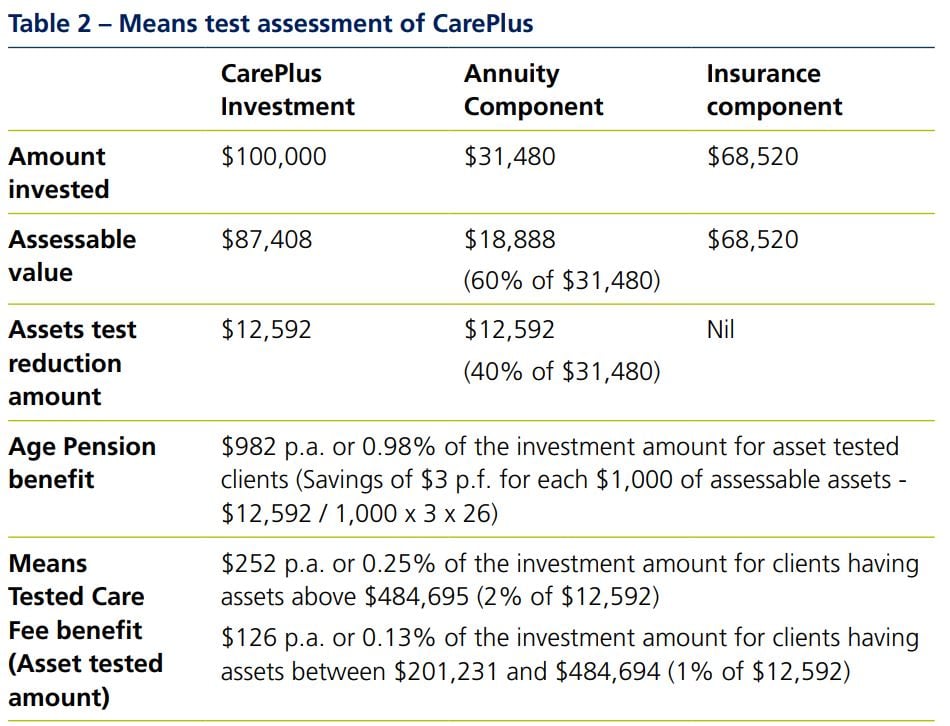

Aged care residents can be asked to pay a means tested care fee (MTCF) which is calculated based on their assessable income and assets. This is an ongoing fee and is a contribution towards the cost of their care in the aged care home. The higher their assessable income and assets, the higher their MTCF (subject to annual and lifetime caps).

An investment into CarePlus may help reduce a resident’s assessable income and assets which can reduce their MTCF. The asset-tested amount is calculated as a percentage of assessable assets at increasing thresholds. The asset thresholds as at 20 March 2024 are:

- 17.5% per annum of assets between $59,500 and $201,231

- 1% per annum of assets between $201,231 and $484,694

- 2% per annum of assets above $484,694

Table 2 outlines the Age Pension benefit for an asset tested client and the MTCF benefit for $100,000 invested in CarePlus as compared to investing $100,000 in a product with no assets test reduction. Note, this benefit changes from year to year and will be different for clients with different age, gender, assets and income.

Assumptions – CarePlus pricing at 22/05/2024 for a female, age 85. CarePlus investment amount of $100,000 (split of $68,520 in CarePlus Insurance and $31,480 in CarePlus Annuity). Rates and thresholds as at 20 March 2024.

Tax effective investment

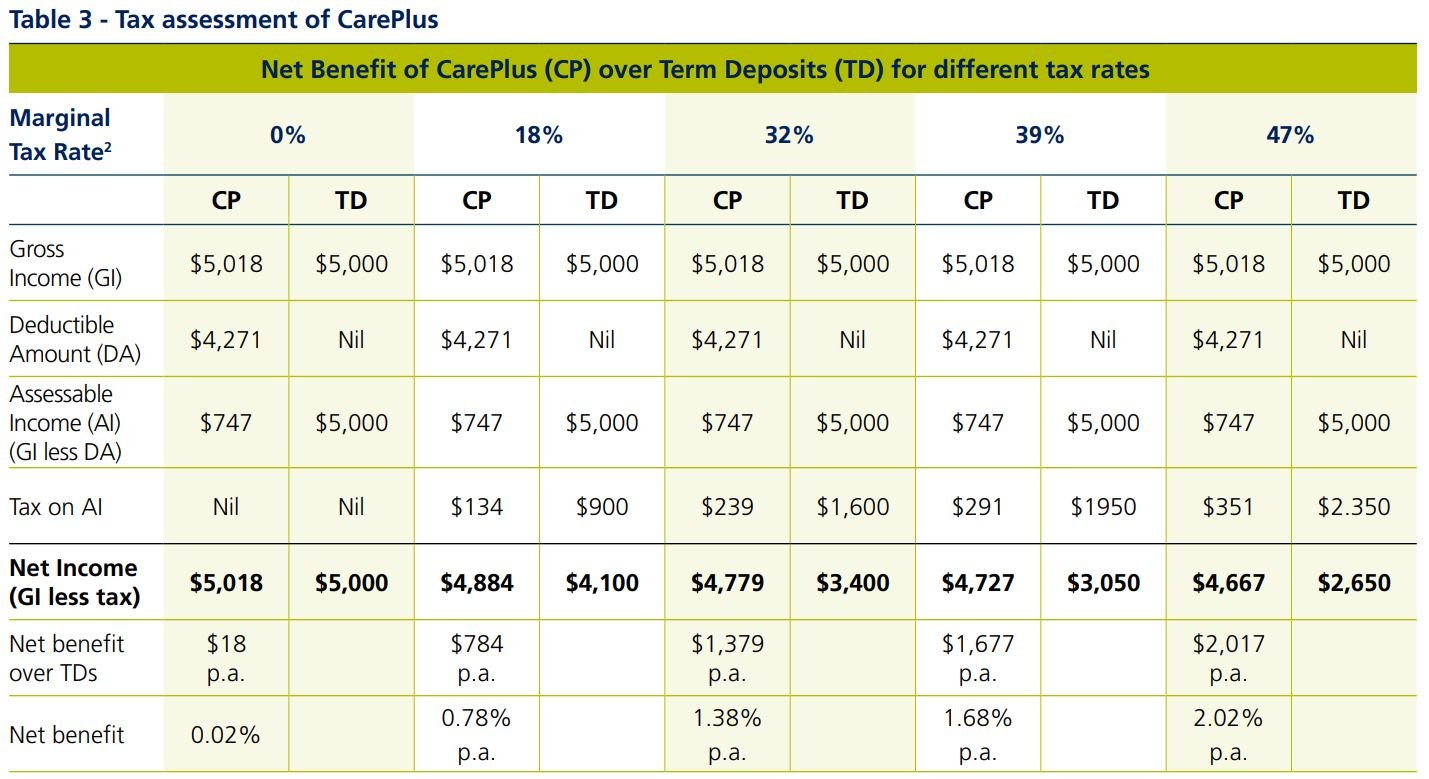

CarePlus can be a tax effective investment option for aged care clients. Unlike other types of investment income, only part of the regular payments from CarePlus is subject to tax. This is because of the availability of a deductible amount that reduces assessable income for tax purposes.

Assessable income from CarePlus = Regular payment less deductible amount

Deductible amount = CarePlus Annuity purchase price / life expectancy at commencement

The value of tax benefits can differ based on the client’s marginal tax rates. Table 3 outlines the income tax benefit for $100,000 in CarePlus as compared to investing $100,000 in term deposits. Note, this benefit changes from year to year and will be different for clients with different age, gender, assets and income.

Assumptions - CarePlus pricing at 22/05/2024 for a female, age 85. CarePlus investment amount of $100,000 (split of $68,520 in CarePlus Insurance and $31,480 in CarePlus Annuity) with an annualised payment of $5,018. Term deposits returning 5% p.a.

Estate planning assurance

Clients can nominate a single or multiple beneficiaries or the estate to receive the lump sum death benefit. If no beneficiary is nominated, the death benefit will be paid to the estate. Challenger allows a Power of Attorney (POA) to nominate beneficiaries on CarePlus Insurance where the POA document contains specific authority to this effect. Challenger can also allow a POA3 to nominate themselves as beneficiary with an appropriate POA legal authority.

When paying CarePlus death benefits, Challenger currently does not require probate if there is a valid beneficiary nomination or if the death benefit is payable to the estate and is less than $500,000. This can reduce the time it takes for beneficiaries to receive bequests and help reduce the cost of applying for probate in states where probate filing fees are dependent on the size of the estate. Where there is a valid beneficiary nomination, Challenger will pay the death benefit directly to that beneficiary i.e. the death benefit is a non-estate asset and will not form part of the estate4.

On death, the total death benefit (CarePlus Annuity death benefit if any plus CarePlus Insurance sum insured) paid to the estate and/or nominated beneficiary(ies) is not subject to tax. This can help with providing estate planning certainty to clients and their beneficiaries.

Case study - Quantifying the combined technical benefits of CarePlus

Lynda, age 85 received an approval from the Aged Care Assessment Team and plans to move into a residential aged care facility with an advertised Refundable Accommodation Deposit (RAD) of $700,000. She lives alone in her own home in NSW worth $1.5 million and does not have any other assets and income other than receiving a full Age Pension.

To enable her to afford the aged care fees, she decides to sell her home and pay $700,000 as RAD. Left with $800,000 to invest and a reduction in her Age Pension due to being asset tested, Lynda approaches her adviser to understand her options. Her aim is to ensure a smooth cashflow for managing her aged care costs without rapidly depleting her capital and a sound estate plan for her grandchildren after she passes away.

Her adviser provided a comparison of investing $500,000 in CarePlus versus Term Deposits. After the analysis provided in Table 3 and 4, he recommended investing $500,000 in CarePlus, currently paying a rate of 5.02% p.a. and investing the remaining $300,000 in term deposits providing an income return of 5% p.a.

Assumptions - CarePlus pricing at 22/05/2024 for a female, age 85. CarePlus investment amount of $500,000 (split of $342,600 in CarePlus Insurance and $157,400 in CarePlus Annuity) with an annualised payment of $25,088. Term deposits returning 5% p.a. Rates and thresholds as at 20 March 2024.

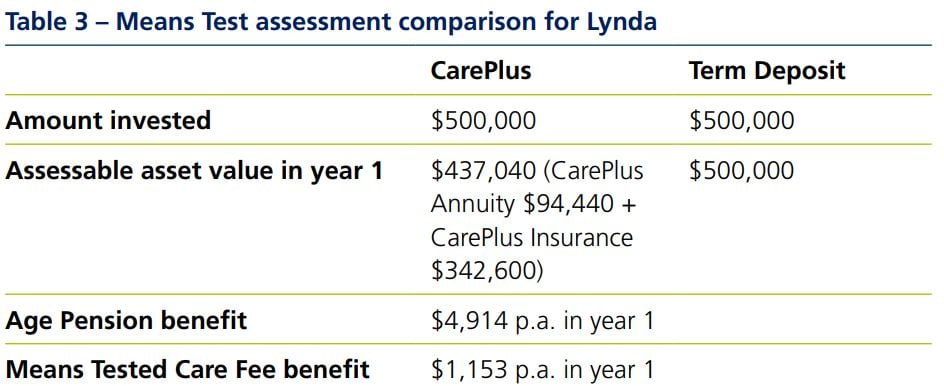

Age Pension and MTCF benefit

With Lynda being asset tested for Age Pension assessment, there is an instant reduction of 40% (40% of $157,400 = $62,960) when assessing the annuity component of CarePlus.

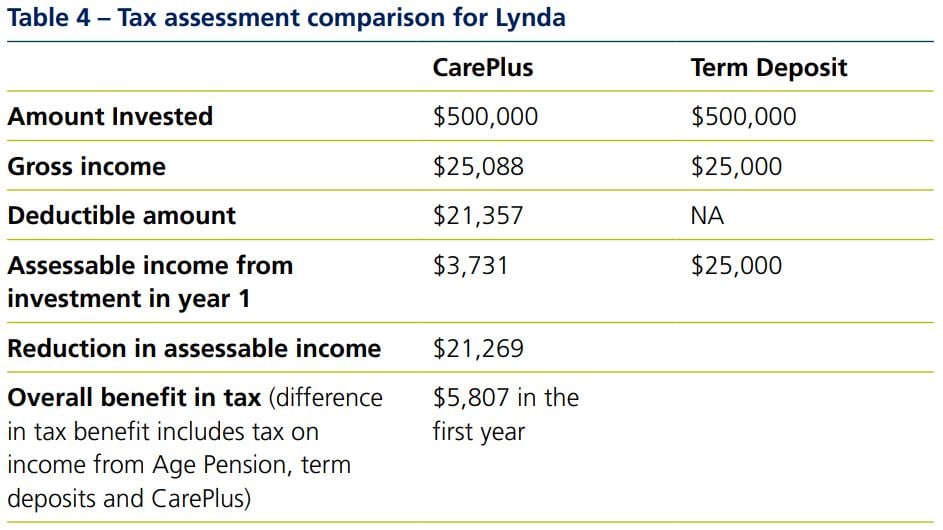

Tax benefit

After taking into consideration the overall technical benefits from an investment of $500,000 in CarePlus, Lynda will receive an additional 2.37% of the investment amount in the first year (an additional $11, 874). This benefit comes from:

- Increased Age Pension ($4,914)

- Reduced Means Tested Care Fee ($1,153)

- Reduced tax payable ($5,807)

Additionally, Lynda will also be satisfied knowing that her grandchildren will receive 100% of the amount invested in CarePlus after she passes away.

Related content

1 For South Australian residents, stamp duty of 1.5% of the CarePlus Insurance premium will be deducted from the death benefit.

2 Includes Medicare Levy and the tax rates are applicable from 1 July 2024.

3 Challenger requires specific wording (or substantially similar in nature) to be in the Power of Attorney document. Required wording for each state can differ and is detailed in the additional information guide available on AdviserOnline.

4 In NSW, notional estate laws exist. The Supreme Court, upon application by an eligible person, may look beyond the property and assets of the deceased estate where the actual estate is not sufficient to meet the family provision order.

The information in this article is current as at 1 June 2024 unless otherwise specified and is provided by Challenger Life Company Limited ABN 44 072 486 938, AFSL 234670 (Challenger, our, we), the issuer of the Challenger annuities (Annuity(ies)) and Challenger Retirement and Investment Services Limited ABN 80 115 534 453, AFSL 295642 (CRISL). The information in this article is general information only about our financial products and is intended solely for licensed financial advisers or authorised representatives of licensed financial advisers, and is provided to them on a confidential basis. It is not intended to constitute financial product advice. This information must not be distributed, delivered, disclosed or otherwise disseminated to any investor, without our express prior approval. Investors should consider the applicable Annuity Target Market Determination (TMD) and Product Disclosure Statement (PDS) available at challenger.com.au and the appropriateness of the applicable product to their circumstances before making an investment decision. This information has been prepared without taking into account any person’s objectives, financial situation or needs. Neither Challenger and/or CRISL, nor any of its officers or employees, are a registered tax agent or a registered tax (financial) adviser under the Tax Agent Services Act 2009 (Cth) and none of them is licensed or authorised to provide tax or social security advice. Before acting, we strongly recommend that prospective investors obtain financial product advice, as well as taxation and applicable social security advice, from qualified professional advisers who are able to take into account the investor’s individual circumstances. Each person should, therefore, consider its appropriateness having regard to these matters and the information in the Target Market Determination (TMD) and Product Disclosure Statement (PDS) for the applicable Annuity before deciding whether to acquire or continue to hold the product. A copy of the TMD and PDS is available at challenger.com.au or by contacting our Adviser Services Team on 13 35 66. Any examples shown in this article are for illustrative purposes only and are not a prediction or guarantee of any particular outcome. Age Pension benefits described in this article will not apply to all individuals. Age Pension outcomes depend on an individual (or couple’s) personal circumstances and may change over time. This article may include statements of opinion, forward looking statements, forecasts or predictions based on current expectations about future events and results. Actual results may be materially different from those shown. This is because outcomes reflect the assumptions made and may be affected by known or unknown risks and uncertainties that are not able to be presently identified. Where information about our products is past performance information, past performance is not a reliable indicator of future performance. Challenger and CRISL relied on publicly available information and sources believed to be reliable, however, the information has not been independently verified by Challenger and CRISL. While due care and attention has been exercised in the preparation of this information, Challenger and CRISL gives no representation or warranty (express or implied) as to its accuracy, completeness or reliability. The information presented in this article is not intended to be a complete statement or summary of the matters to which reference is made in this article. To the maximum extent permissible under law, neither Challenger, CRISL, nor its related entities, nor any of their directors, employees or agents, accept any liability for any loss or damage in connection with the use of or reliance on all or part of, or any omission inadequacy or inaccuracy in, the information in this article.

Stay informed

Sign up to our free monthly adviser newsletter, Tech news containing the latest technical articles, economic updates, retirement insights, product news and events.