RBA Interest Rates Rise Again Third Straight Hike Explained

Subscribe to Macro Musing

To stay up to date on the latest economic insights, subscribe to Macro Musing on LinkedIn.

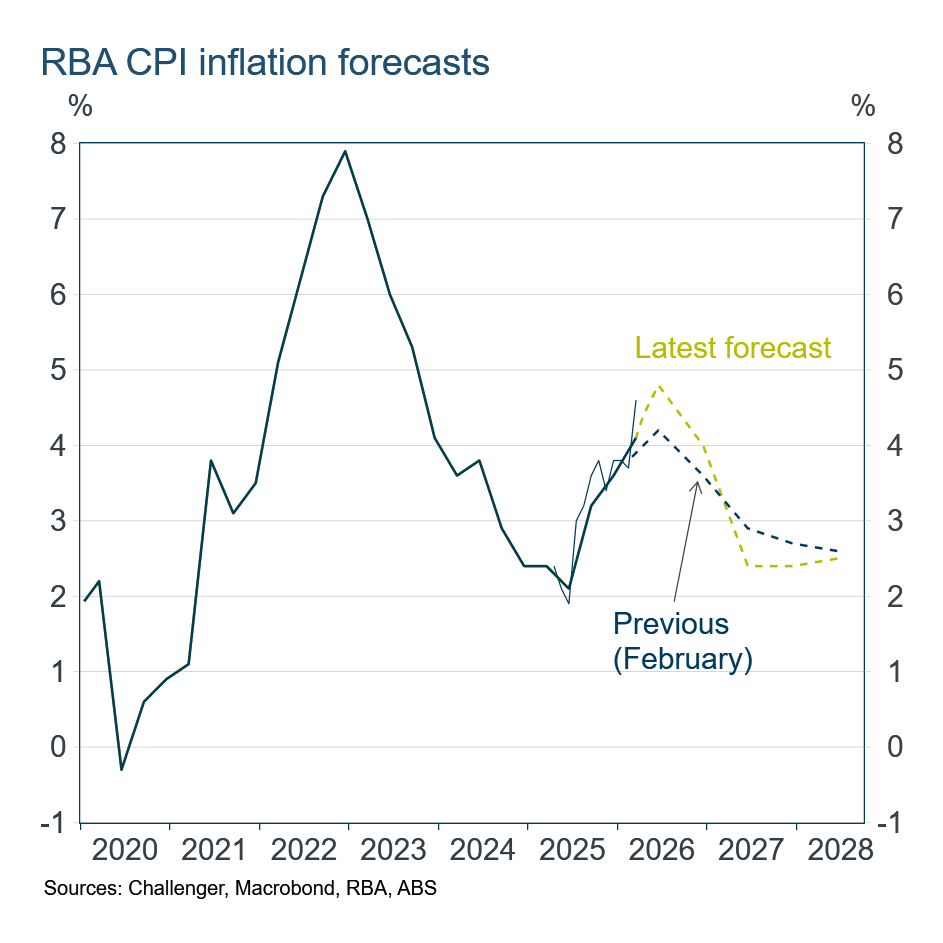

The RBA hiked rates for the third meeting in a row with the near-consensus 8‑1 vote a surprise after the previous meeting’s 5-4 close call. The RBA has increased rates quickly to get monetary policy to being somewhat restrictive as it seeks to avoid the oil-shock adding to already strong domestically-driven inflation. The risk of high inflation becoming ingrained in the economy increases the longer inflation remains significantly above the RBA’s target.

After three increases in a row, as things stand the RBA will likely be able to pause at the next meeting to assess the impact. But as the Board statement notes, “risks remain tilted to the upside, including to inflation expectations” and so with oil prices so uncertain a pause cannot be guaranteed.

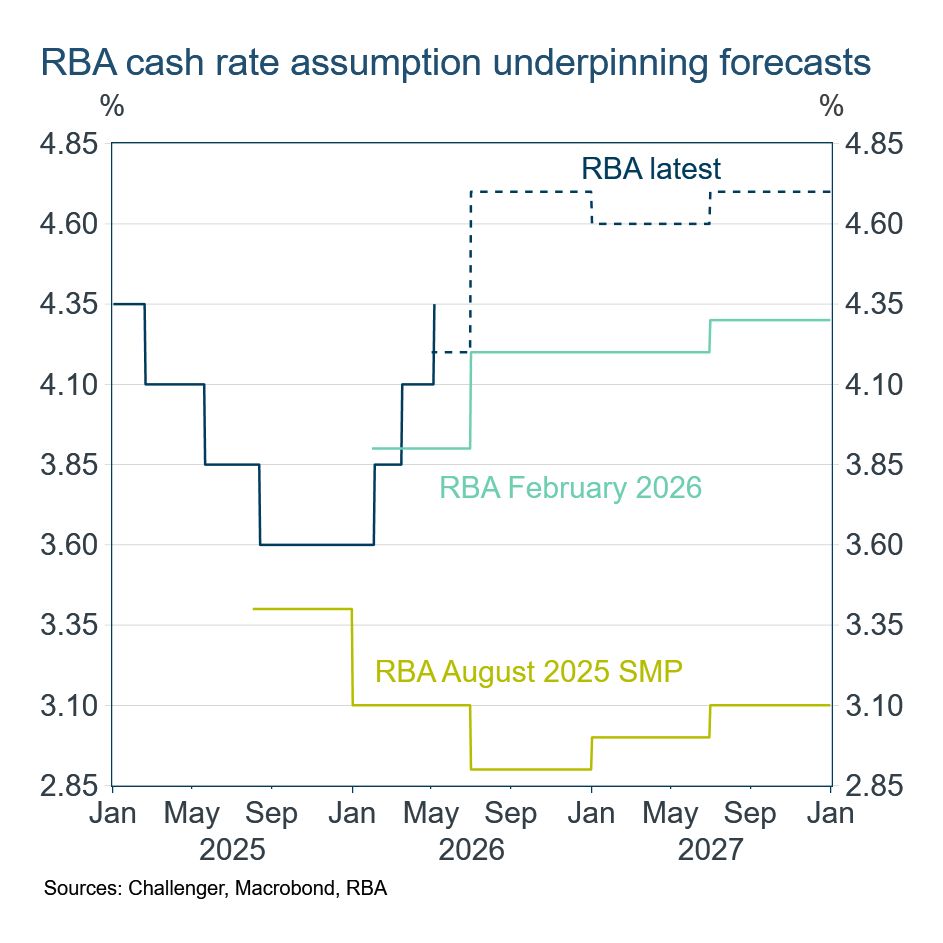

The RBA uses a forward path for the cash rate based on market interest rates to generate its forecasts. That path implies another 1–2 hikes this year. It’s been a stunning turnaround in the economic outlook and rates expectations since August last year when the RBA and others expected ongoing rate cuts as inflation was projected to fall. This has seen 3-year yields rise almost 150 basis points and 10-year yields up almost 75 basis points, significantly increasing income for low-risk investors including retirees.

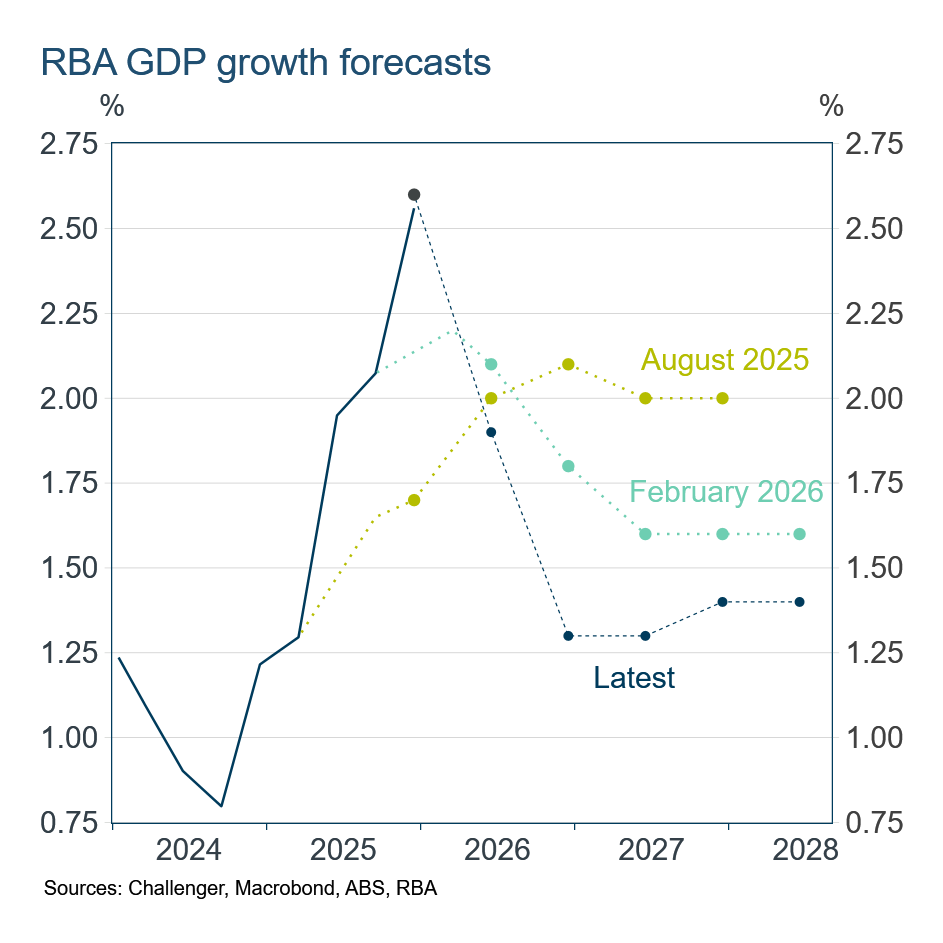

Economic growth was stronger in the second half of 2025 than had been expected, but with higher interest rates and inflation, GDP growth is expected to fall sharply. Growth of 1.3–1.4% from late 2026 would mean two years of virtually no growth in GDP per capita and therefore living standards. Dwelling investment is expected to be contracting by late 2027 given higher interest rates, weaker income growth and no doubt softer house price growth. After falling short in the first year, the Government’s target of 1.2m new homes being built in five years looks to be increasingly wishful.

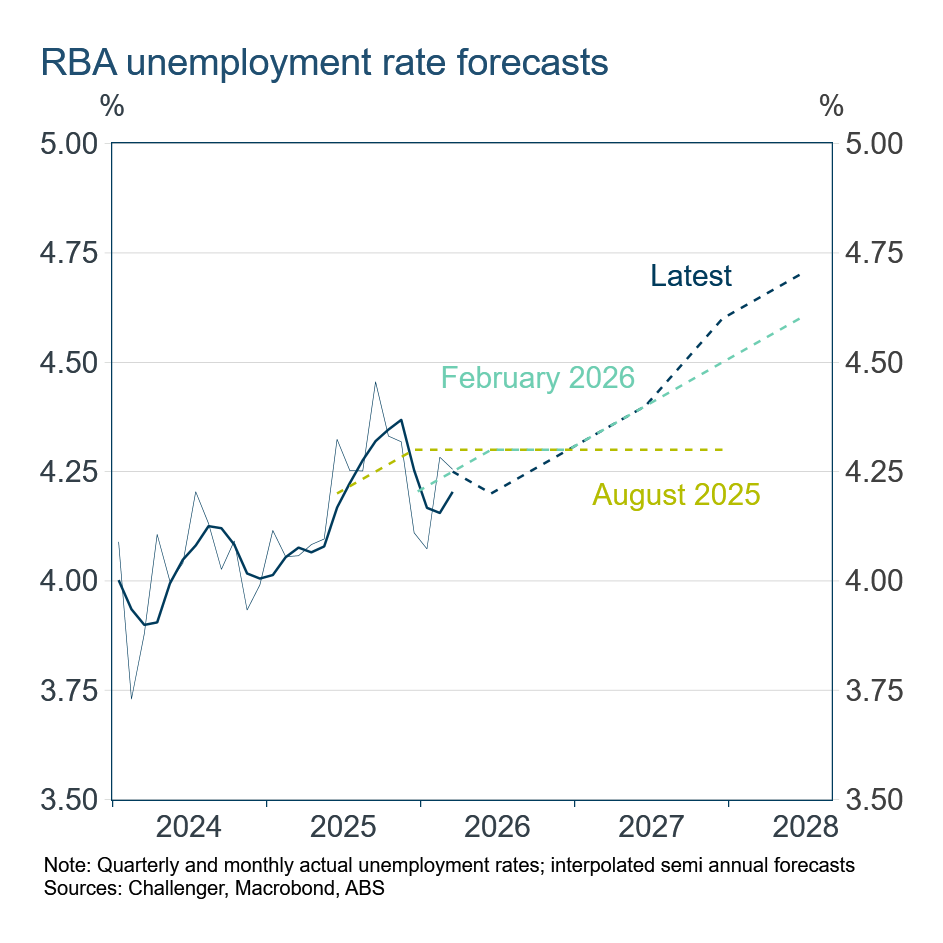

While there was another significant downward revision to GDP growth, there was little change in the RBA’s unemployment rate forecasts. The unemployment rate is projected to gradually increase over the forecast horizon to mid-2028, reaching 4.7% an upward revision of only 0.1 percentage point.

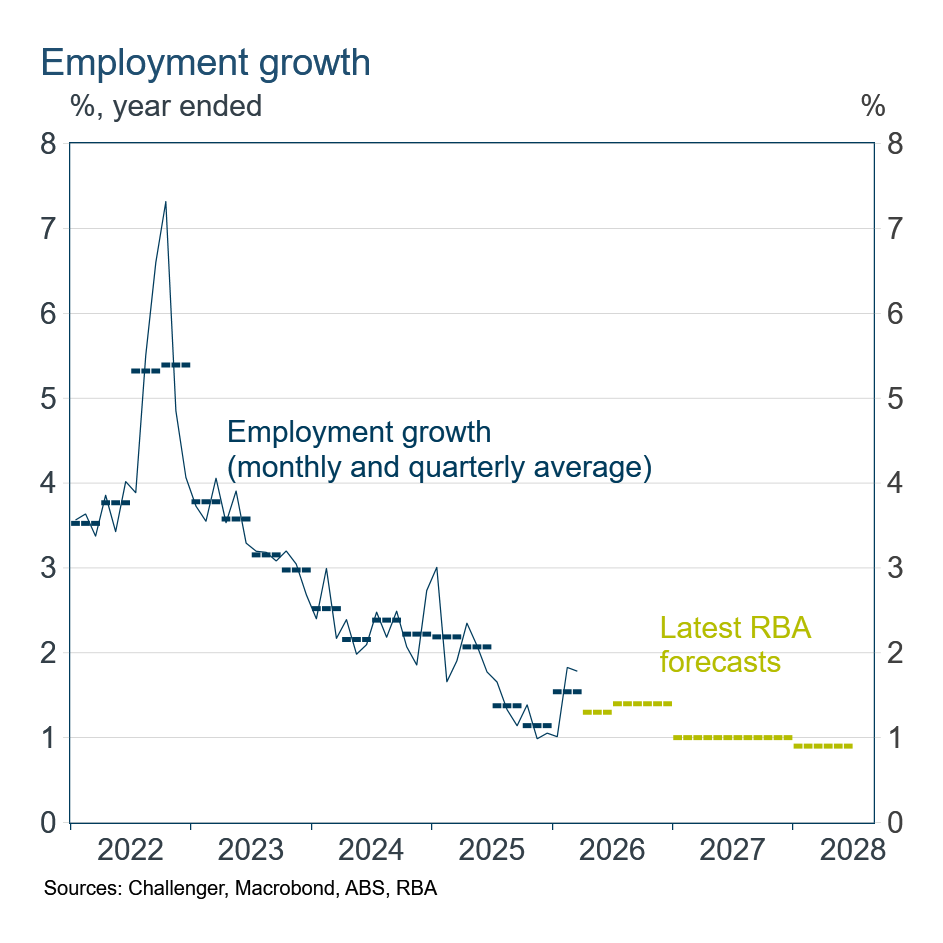

Employment growth is projected to be weak over the next couple of years dropping to around 1%, slower than population growth. With this weak employment growth, the RBA is also factoring in a fall in the participation rate as workers become discouraged by higher unemployment and drop out of the labour market. A decline in the share of people working or looking for work would be surprising given the pressure on many household budgets. However, a softer labour market could encourage some of the increasing number of older workers into retirement.

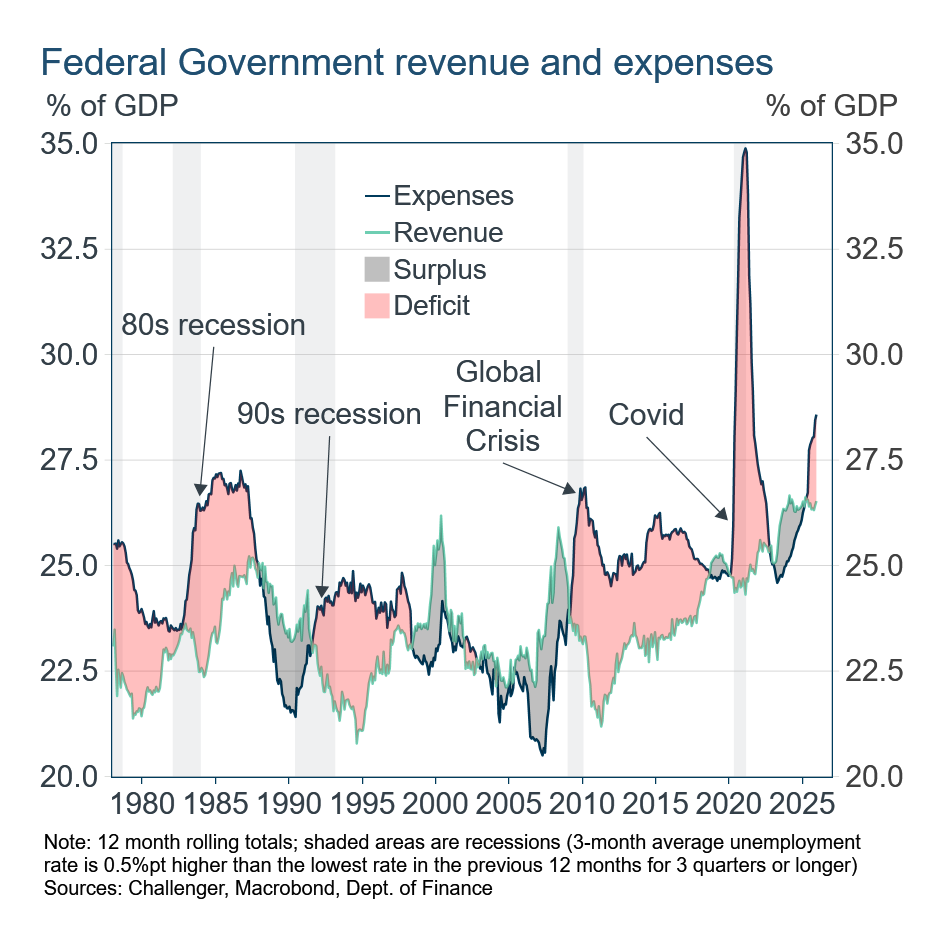

With the RBA’s decision out of the way attention can shift to the Federal Budget next Tuesday. There has been a sequence of curated leaks over recent weeks notably highlighting changes to tax and reforms to restrain NDIS spending. While the increase in living costs makes it tempting for the Government to provide further benefits to households, it is critical that aggregate spending growth isn’t just slower, but slower than GDP growth.

Historically, revenues fall and expenses rise in recessions. But since the pandemic, and despite the low unemployment rate, spending growth has accelerated at a pace typically seen in recessions. Something has got to change.