Residential aged care considerations for self-funded retirees

Residential aged care considerations for self-funded retirees

Download the full article below.

Due to their higher means, a certain cohort of clients are not eligible for any social security payments. For these clients, advisers sometimes enquire as to whether there are any specific considerations when these self-funded clients enter residential aged care. Typically, issues such as whether there is any financial detriment if means are not disclosed to Services Australia, cashflow, lifetime caps for ongoing fees and potential financial restructuring to improve position are some of the key considerations which are deliberated.

In this article, we look at some of the common issues advisers bring to the discussion when dealing with self-funded clients.

Unless otherwise quoted, the numbers and thresholds stated in this article apply as at 1 January 2026 and will be subject to routine indexation.

Self-funded for aged care and social security purposes

While the aged care means testing is based on both assets and income, for most clients, the assets component forms the bigger component of the means tested amount.

From an aged care means testing purpose, there are two issues to consider when it comes to discussing the concept of self-funded – at what level of assets is the client a Refundable Accommodation Deposit (RAD) / Daily Accommodation Payment (DAP) payer and what level of assets makes the client pay the capped Hotelling Supplement and Non-Clinical Care Contribution?

A client is a RAD payer if their means tested amount is ≥ $70.94 per day which is the case when assessable assets are ≥ $210,555. For single homeowners, where the home is not resided by a protected person1, this would mean that the client is a RAD payer on the assumption that the home is worth ≥ $210,555. For partnered homeowners, where one member of the couple enters aged care, they would be a RAD payer if their assessable assets outside of the family home are ≥ $421,110.

The RAD varies based on the facility’s advertised price but anecdotally there could be a range between $350,000 to $3.26 million, with advisers reporting an increase in RAD prices since 1 January 2025. Where the RAD is unpaid, the client is liable for a DAP which is effectively interest on the unpaid RAD. The current interest rate for entry into aged care between 1 January 2026 to 31 March 2026 on an unpaid RAD is 7.65%.

It’s worth noting that a self-funded client could potentially be eligible for social security entitlements upon entering residential aged care depending on the level of their means. Upon paying a RAD which is exempt from a social security perspective, client’s level of assessable assets could reduce and the client could potentially be eligible for social security.

Example – self-funded retiree becoming eligible for the Age Pension upon entering care

Daisy has a home worth $1.5 million and has $1 million in other financial assets. She hasn’t been receiving the Age Pension because of failing the assets test which currently has a cut-off limit of $714,500 for single homeowners.

Upon entering aged care, her home will be exempt for two years. She intends to allow one of her grandchildren to live in the home rent-free. She will pay $750,000 RAD, leaving her with $250,000 in financial assets.

During the two year period while the family home is exempt, Daisy could be eligible for the full Age Pension. However, after the two year period or when the home is sold (whichever occurs earlier), with the inclusion of the family home as an assessable asset, she will lose the Age Pension.

Hotelling Supplement Contribution and Non-Clinical Care Contribution reach their maximum cap at assessable assets of around $1.023 million

The two new ongoing means tested fees from 1 November 2025 are the Hotelling Supplement Contribution (HSC) and Non-Clinical Care Contribution (NCCC). Liability towards these fees is based on the means tested amount (MTA) which is based on the client’s assessable assets and income.

Focusing specifically on assets, the HSC applies2 once assets exceed $252,000 and reaches the daily cap of $22.15 per day when assets are ≥ $355,367.

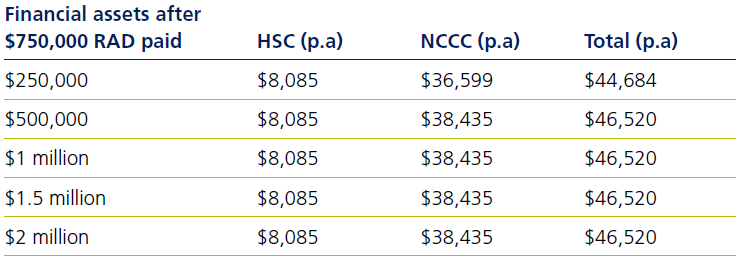

Conversely, the NCCC applies once assets exceed $532,055 and reaches the daily cap of $105.30 per day when assets are ≥ $1,023,455. It’s likely not far fetched to imagine that with inclusion of the RAD, which based on averages is increasing, many self-funded clients may be liable for capped HSC of $8,085 p.a. and capped NCCC of $38,435 p.a. The NCCC does have a lifetime cap of $135,319 or 4 years of NCCC liability, whichever is earlier.

The table below outlines the HSC and NCCC for a single, non-homeowner, who has paid a RAD of $750,000 with different levels of remaining financial assets. It highlights that with inclusion of the RAD, once assessable assets are approximately $1.023 million, clients are liable for the maximum, daily capped HSC and NCCC.

It’s worth noting that in addition to the above ongoing means-tested fees, clients will be liable for $23,926 p.a. Basic Daily Care Fee and, if applicable, any Higher Everyday Living Fee.

Is it worth disclosing the means?

To be assessed for their cost of care, self-funded clients would be required to complete the Residential Aged Care calculation of your cost of care form (SA 457). If the form is completed, then in time, Services Australia confirms the HSC and NCCC. Based on conversations with advisers, there is sometimes a reluctance to complete this form especially if the client has not dealt with Services Australia in the past and has a preference to keeping it that way.

For those who are subject to 1 November 2025 rules, there is no financial detriment in not disclosing their means if the means tested amount is ≥ $198.39 per day. A client’s means tested amount would be ≥ $198.39 per day if their assessable assets are $1,023,455 for a single person or $2,046,910 for a partnered person.

Where their means are not disclosed, the client would be liable for the advertised RAD, capped HSC of $22.15 per day ($8,085 p.a) and capped NCCC of $105.30 per day ($38,435 p.a) until they reach the NCCC lifetime cap.

Means not disclosed status

Clients who do not wish to disclose their means could simply indicate on Question 14 in the SA 457 form that they do not wish to disclose their means. If clients have commenced care and do not complete the SA 457 form, they are sent an initial letter requesting them to disclose their means followed by a reminder letter. If the form is not completed following the reminder letter, the final letter confirms that the client’s status is means not disclosed.

If a client who does not disclose their means wishes to disclose their means in the future, they can do so however any reassessments will not be backdated, and reassessment of assets will apply from the date of disclosing their means.

Interaction of completing the SA 457 form, means not disclosed status and ability to pay RAD

With the advent of 1 November 2025 rules, the law3 states that if the client has not had their ‘means not disclosed’ status yet determined which would occur if the client has either not completed the SA 457 form and the final letter confirming their status hasn’t yet been confirmed (noting the process outlined above) or they have completed the form but Services Australia hasn’t yet issued the confirmation letter notifying of fees which can be charged, that they can only pay the accommodation payment as a DAP and not a RAD.

This is usually an interim period until the status has been determined but it can affect how the client pays for their accommodation while their status is being confirmed. Anecdotally, we are hearing from advisers that given that it is new law, most facilities continue to accept RAD during this interim period. That said, in few situations, some facilities adhere to the strict letter of the law and only accept DAPs until the means not disclosed status has been officially confirmed.

1. A protected person is a spouse, dependent child under 25, carer who has lived in the home for at least two years and receiving or eligible to receive a social security payment, a close relative who has lived in the home for at least 5 years and receiving or eligible to receive a social security payment.

2. HSC and NCCC is not payable until it is at least $1 per day.

3. AGED CARE ACT 2024 - SECT 294 Accommodation agreements – please refer to Section 294 (1)(ca)(ii)

Related content

Stay informed

Sign up to our free monthly adviser newsletter, Tech news containing the latest technical articles, economic updates, retirement insights, product news and events.