The economic impact of oil price shocks on inflation, growth and employment

Subscribe to Macro Musing

To stay up to date on the latest economic insights, subscribe to Macro Musing on LinkedIn.

Oil price shocks are the stuff of nightmares for central banks. They simultaneously increase inflation and reduce economic growth, resulting in higher unemployment. Growth is hit from reduced spending by households and businesses facing higher prices. It also comes from disruptions to the supply of oil constraining production (e.g. plastics, fertiliser) and the change in relative prices inducing firms to change how they produce.

Because of the trade-off between higher inflation and lower growth, the text book prescription for central banks is to ‘look through’ – i.e. ignore – temporary oil shocks. However, there is a critical caveat that if oil-induced inflation results in a rise in inflation expectations central banks will typically increase their policy rates somewhat to avoid the oil shock resulting in persistently higher inflation.

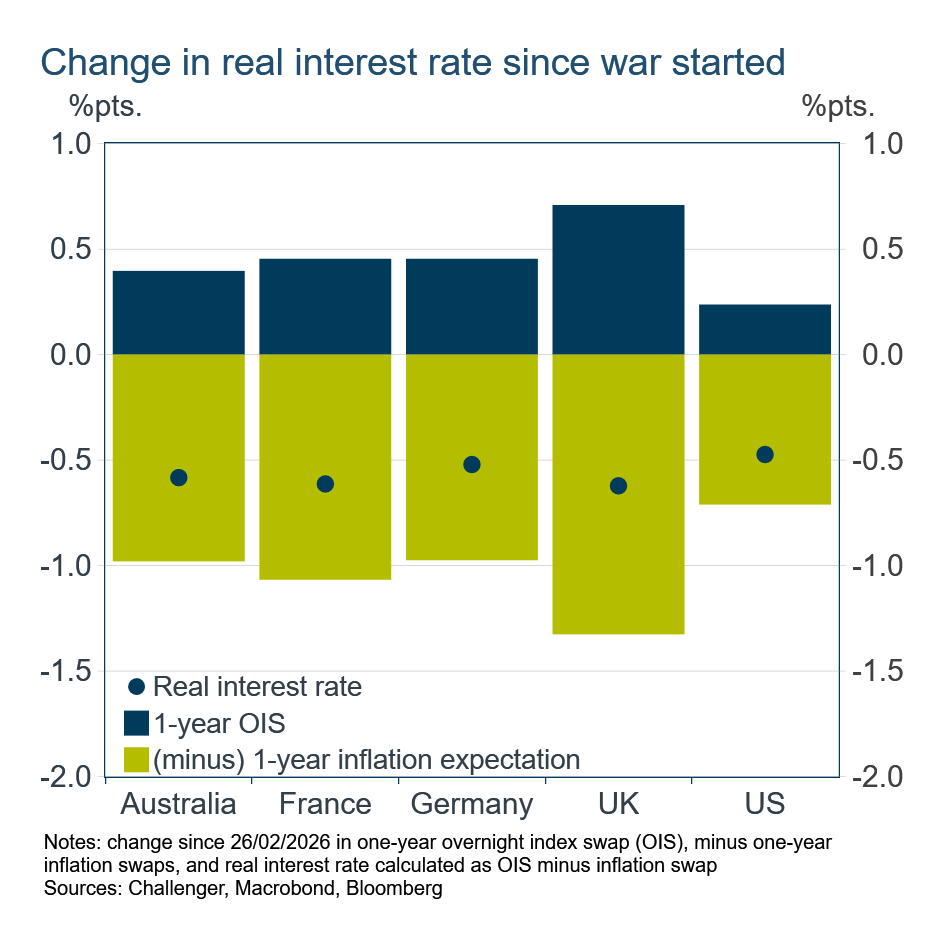

That is exactly how markets are expecting central banks to respond to the current oil shock. For a selection of countries, one-year inflation swaps have increased by around 1 percentage point since the onset of the Middle East war (a bit more for the UK, a bit less for the US). One-year Overnight Indexed Swaps (OIS) – which map market expectations for central bank policy interest rates – have increased by a touch under 50 basis points (again a bit more for the UK, a bit less for the US).

Taken together, higher OIS and higher inflation expectations imply that expected real policy rates – policy rates minus inflation – have fallen by a little more than 50 basis points. Because interest rates are forward-looking (i.e. returns over the coming year), it’s consistent to deflate them with expected, not realised, inflation.

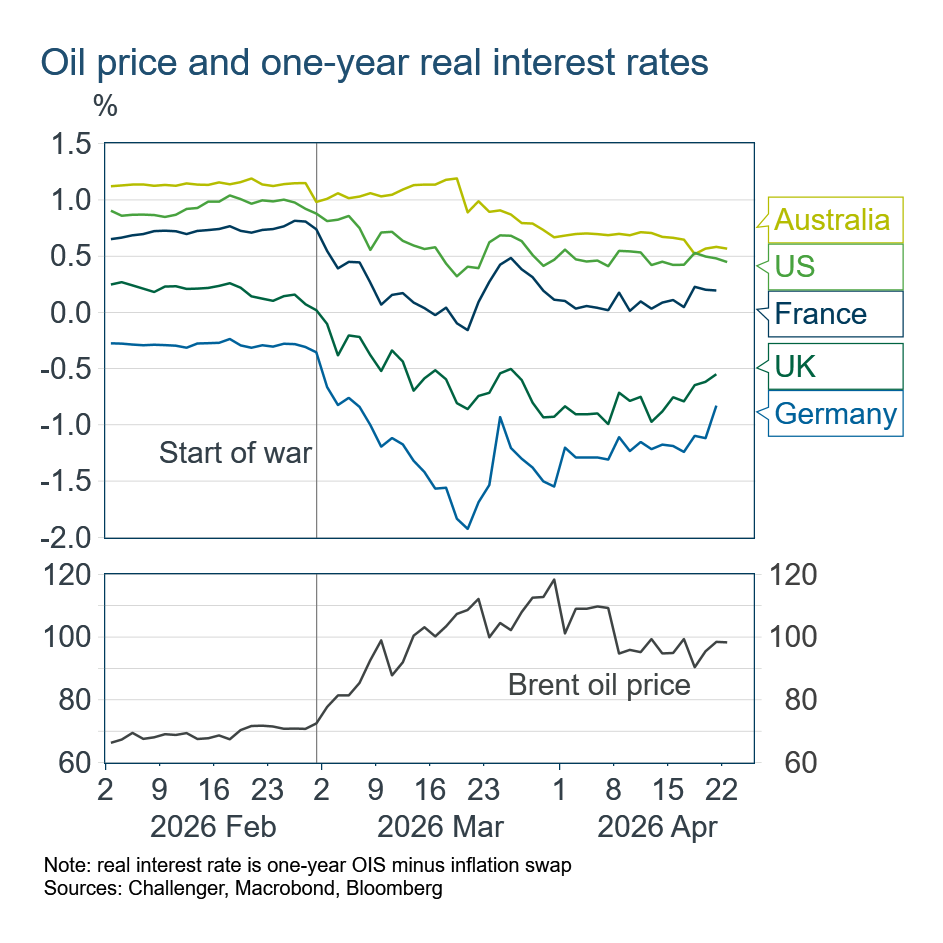

Real rates fell through March as oil prices rose, then partly reversed when oil pulled back on 20 March. In April, one-year real rates have been broadly steady even as the oil price declined. Markets appear to think there are limits to how far central banks will accommodate higher inflation.

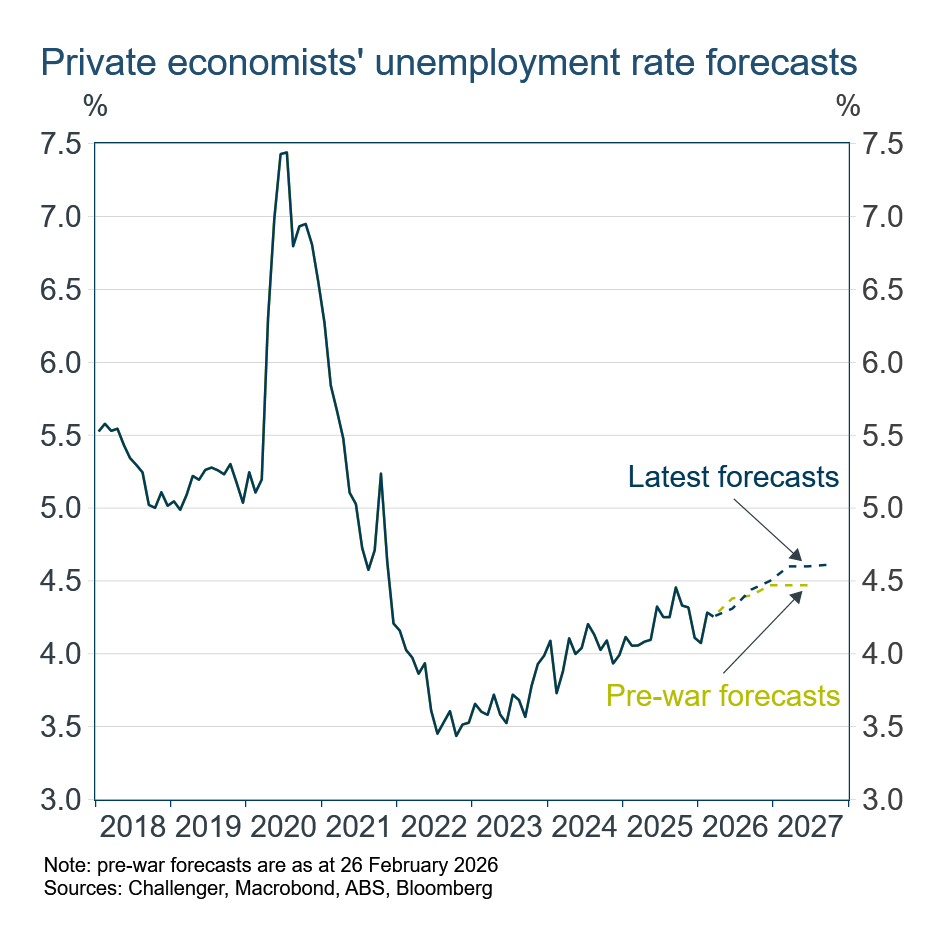

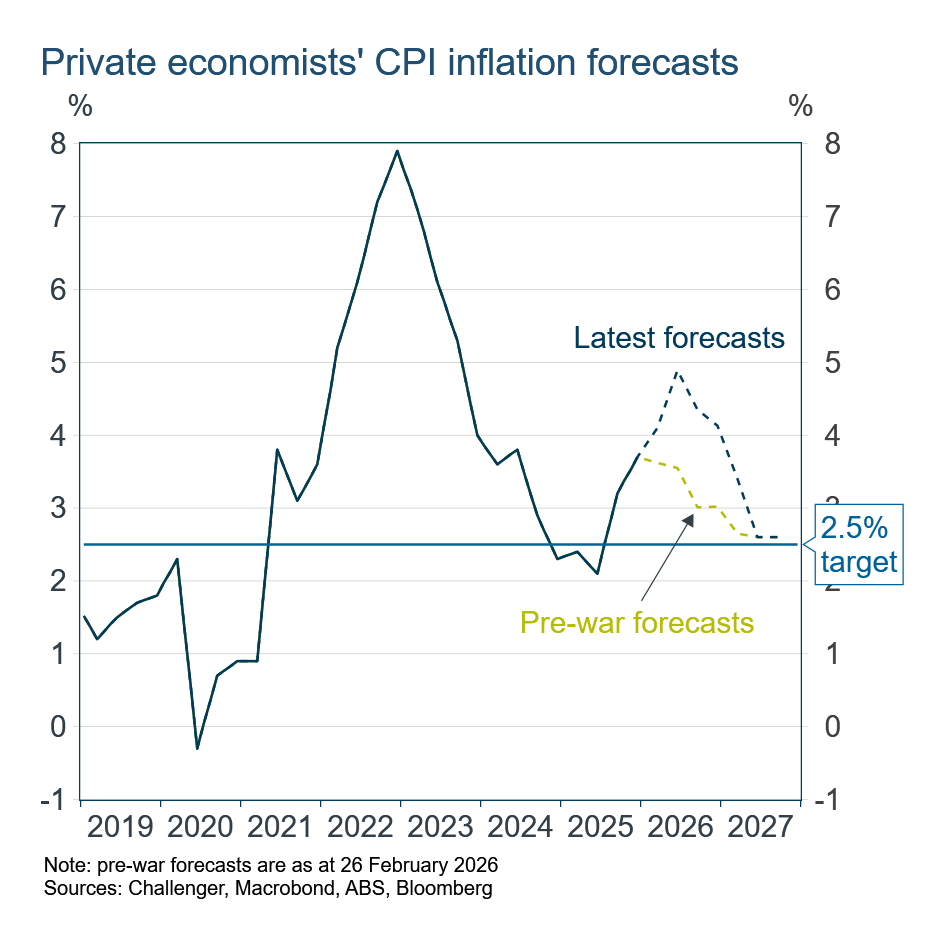

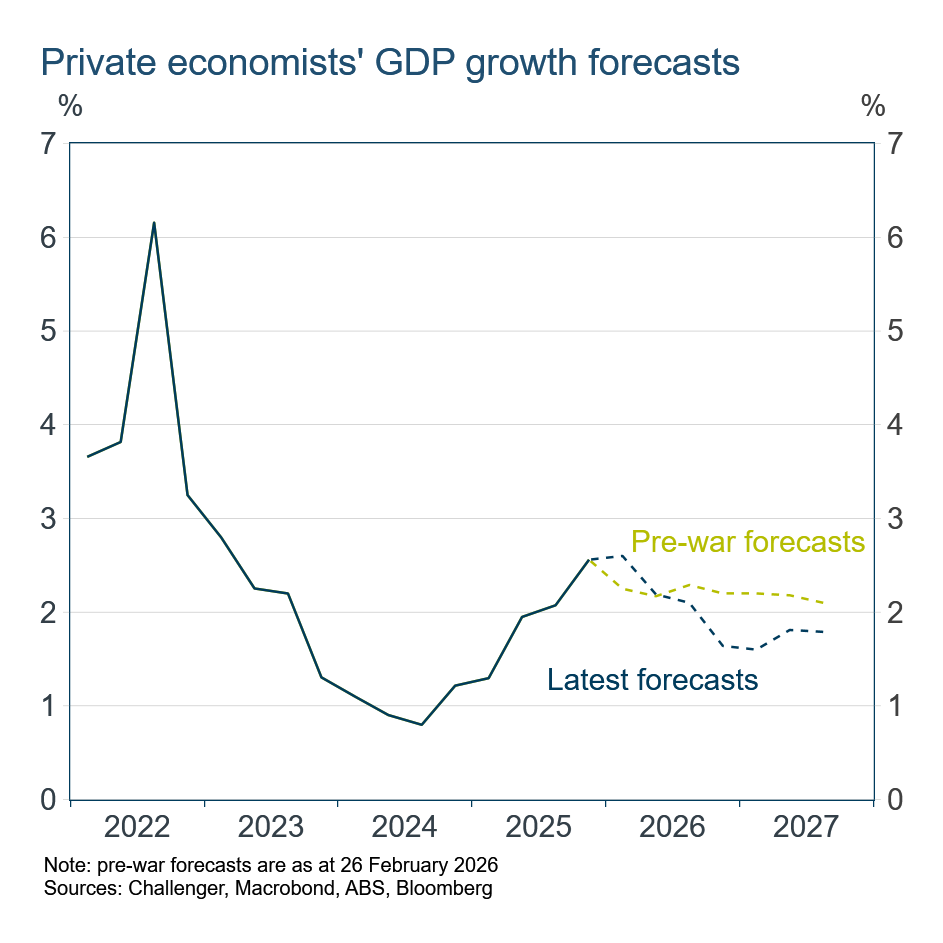

The implications of this expected policy response by the RBA – only partly offsetting the oil-induced inflation – is clear in Australian economic forecasts. Economists have revised up their inflation outlook, now expecting a peak just under 5% in June – far above pre-war expectations that inflation would keep falling from its December peak of 3.7%. (I use a survey rather than my own forecasts as combining forecasts is typically more accurate – the crowd is indeed wise, or at least less flawed.)

Higher rates and higher inflation will slow the economy, even if the economy’s momentum keeps growth steady in Q1. Growth is projected to fall to 1.6% by early 2027 – only a little below potential growth of 2–2¼% – then pick up as inflation eases and the impact of rate rises wanes.

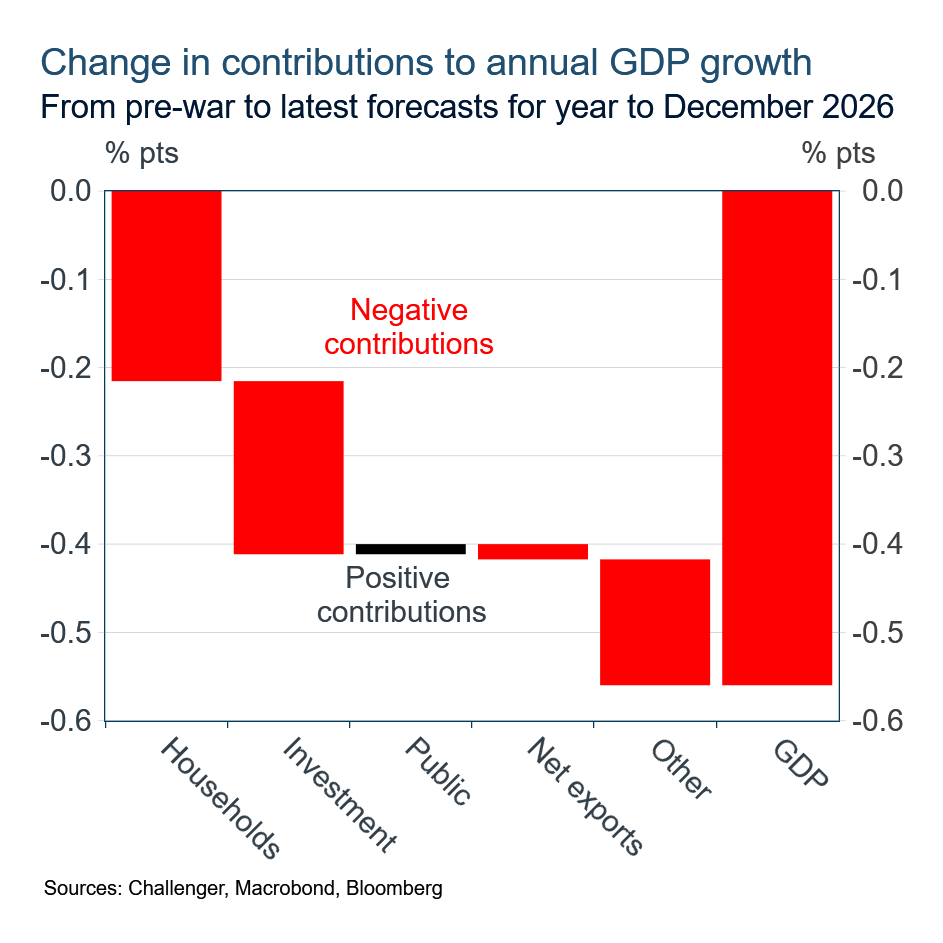

The downward revision to GDP growth projections is not only attributable to softer household consumption. Weaker investment contributes as much to slower GDP growth as does weaker consumption, highlighting the broad impact of the oil shock on the Australian economy.

With projected GDP growth only a little below the economy’s potential growth rate, the anticipated increase in unemployment is small. The unemployment rate is projected to peak at 4.6%, around estimates of the unemployment rate that neither adds to, or detracts from, inflation (the ‘NAIRU’).

This suggests that from 2027, with the labour market no longer tight, the RBA will be comfortable reducing the cash rate, so long as the inflation dragon truly has been slain by then and is not just licking its wounds.