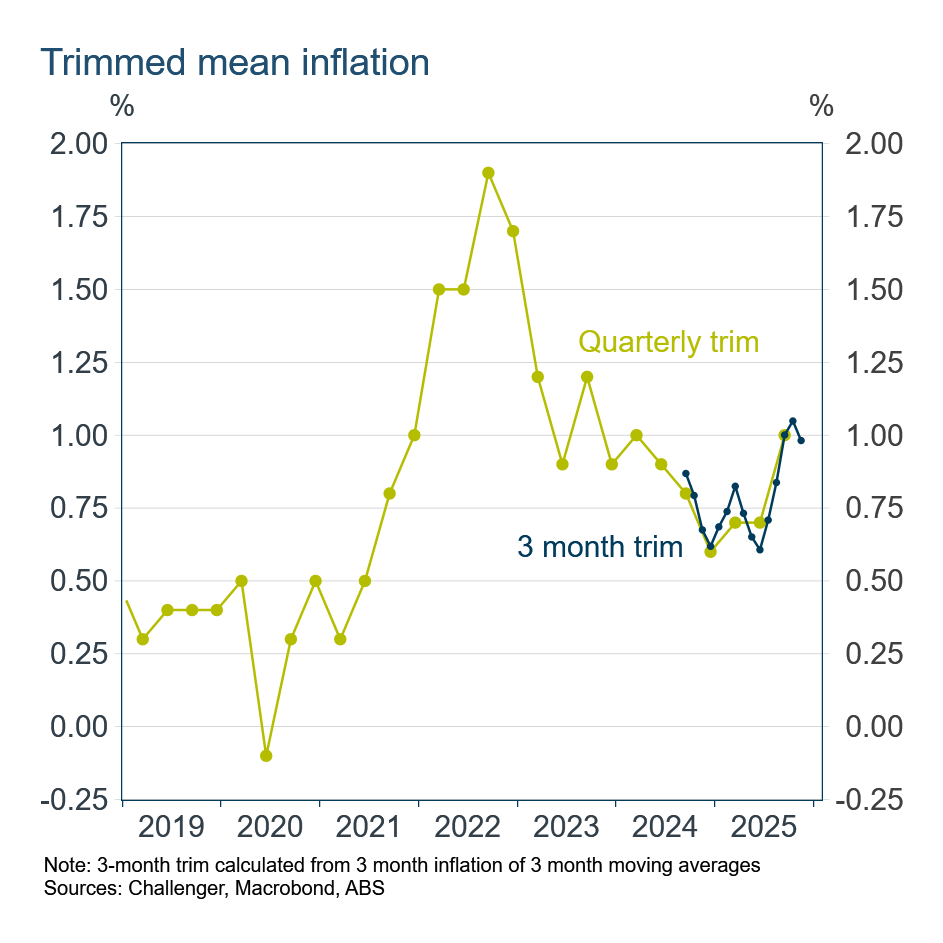

Three‑month trimmed mean shows inflation remains elevated

Subscribe to Macro Musing

To stay up to date on the latest economic insights, subscribe to Macro Musing on LinkedIn.

The summer break glow is fading quickly as reality hits of global geopolitical and economic uncertainty. On the domestic front a U-turn in rates is needed given resurgent inflation.

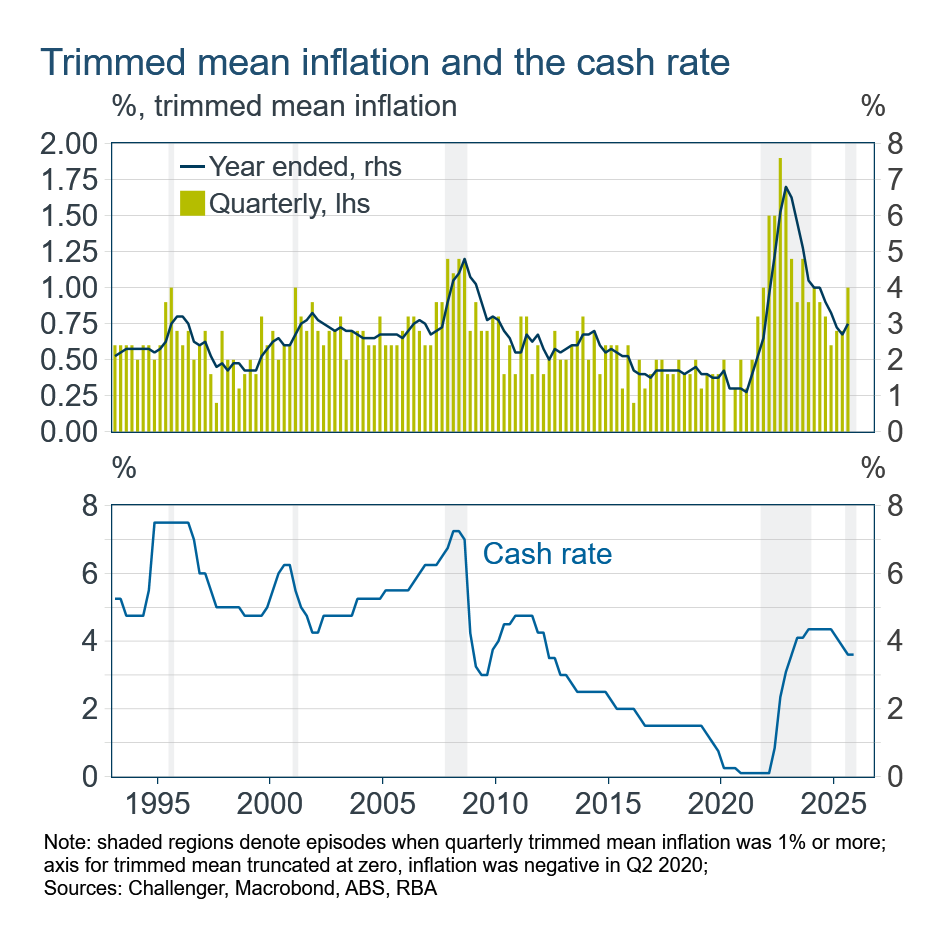

The RBA focuses on trimmed mean inflation which better reflects demand and supply pressures. Trimmed mean inflation in the September quarter was 1%, a rate that has signified excessively high inflation over the RBA’s Inflation Targeting era. In 1995 and 2001, 1% quarterly inflation lasted only one quarter but saw annual inflation climb above 3%. Both times the RBA had already tightened policy, anticipating higher inflation.

In 2007-08, 1% quarterly inflation lasted for a year, but again the RBA had seen inflation pressures building and the cash rate had already been increased significantly. The cash rate was only subsequently cut quickly because of the onset of the Global Financial Crisis.

And then there was the post-pandemic inflation surge. The cash rate was increased sharply through this period from its near-zero base. The crucial question is whether the September quarter 1% inflation was a blip as price pressures ease, or an inflation resurgence.

With the benefit of the new monthly CPI we have more timely information on price pressures. I construct a 3-month trimmed mean measure of inflation which provides the best timely measure that aligns with the long history of the quarterly trimmed mean that has been so crucial in influencing RBA policy. This shows that inflation has remained high, with rates around 1% in October and November.

Policy needs to be tighter to redress the imbalance of demand that is too strong for supply in the current economy.

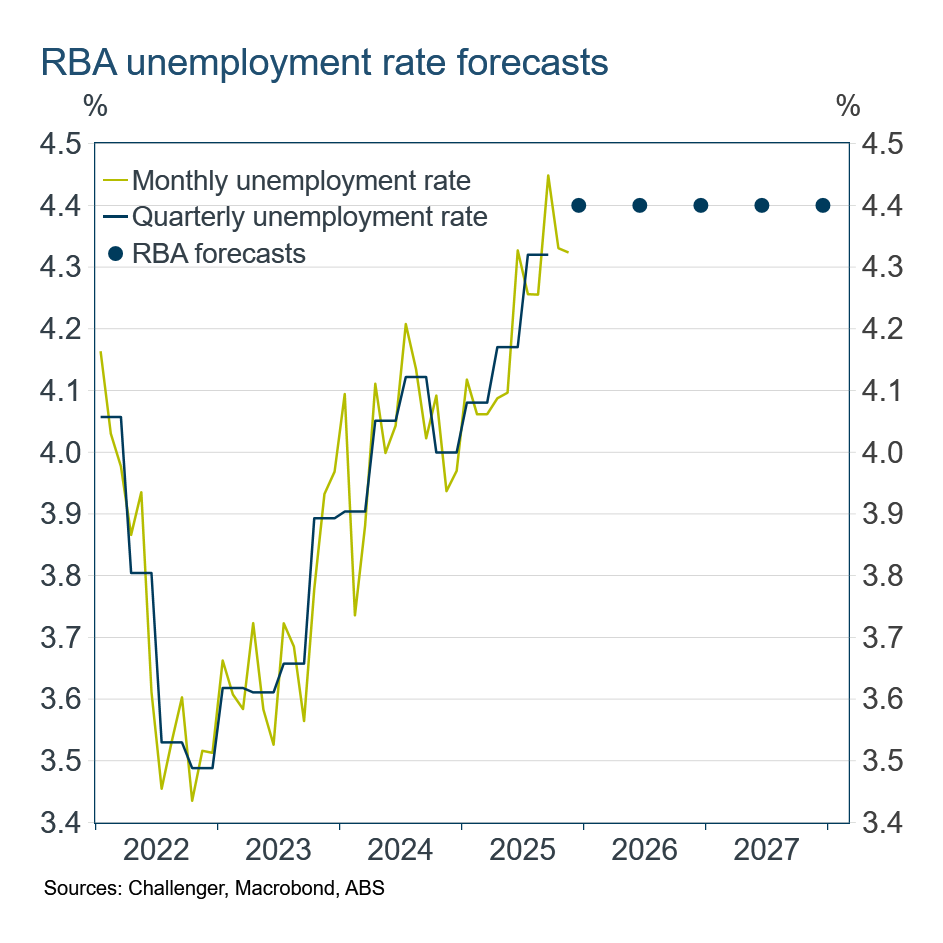

The inflation outlook has clearly deteriorated – the RBA forecast annual trimmed mean inflation for the year to December to be 3.2% but it is likely to be 3.4%. What could stop the RBA from raising rates? The RBA has a dual mandate and so must also consider employment outcomes. However, unlike inflation, the unemployment outlook has not deteriorated. In its latest forecasts the RBA projected the unemployment rate to rise slightly and then remain stable at 4.4%. The monthly unemployment rates for October and November at 4.3%, are consistent with this outlook.

The cash rate is close to, or even slightly above, most estimates of its ‘neutral’ level, where it would be neither stimulating nor contracting the economy. However, overall financial conditions are much more expansionary than this suggests. Spreads, the additional cost above the cash rate that borrowers actually pay, are very low and financing is readily available on favourable terms. Nor is fiscal policy applying a brake to the economy. Given this, the cash rate needs to be higher for the RBA to bring inflation back to its 2.5% target. The final piece of the puzzle to confirming this will be the December CPI released next Wednesday.

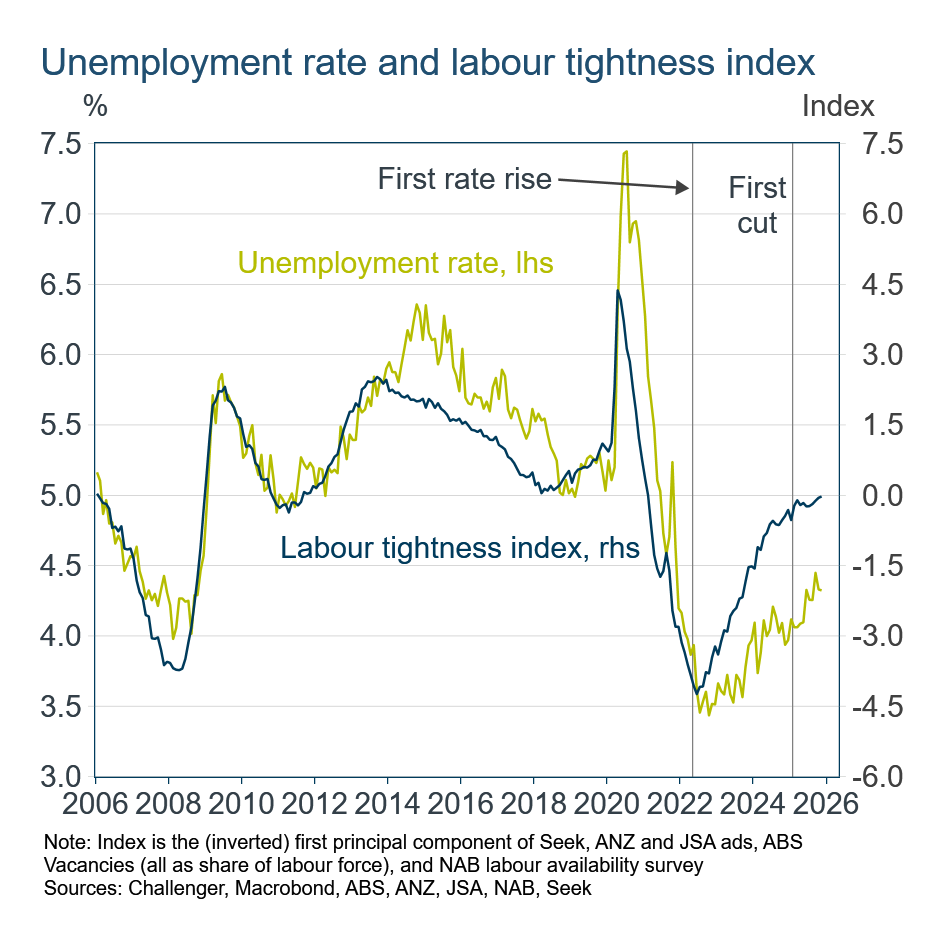

The outlook for the labour market also looks relatively benign and so not a constraint to raising the cash rate. An index of leading indicators I construct shows that the prospects for the unemployment rate have improved with the rate cuts so far. The unemployment rate has increased from its generational lows of 3.5% but at less than 4.5% it remains lower than almost the entire period since the mid-1970s. A higher cash rate will deteriorate the outlook for the labour market, but not enough to derail the higher rates needed to contain inflation.