Treasury’s best practice principles for superannuation retirement income

.png?h=360&iar=0&w=640)

Treasury’s best practice principles for superannuation retirement income solutions

Download the full article below.

In February 2026, the Australian Government released the best practice principles for superannuation retirement income solutions (the Principles). Issued by Treasury, the Principles provide voluntary guidance to superannuation trustees on how to design, deliver, and continuously improve retirement income solutions for members approaching and in retirement.

Although the Principles apply directly to superannuation trustees rather than financial advisers, their practical influence will likely be widely felt across the retirement advice ecosystem. The Principles articulate government expectations around retirement product design, cohort-based solutions, member engagement, and the role of guidance and advice. Collectively, they will shape the products advisers recommend (or choose not to recommend), the superannuation income stream defaults clients encounter, and even, to some degree, the standards against which “good” retirement advice may be judged.

For advisers, understanding these Principles is important. They frame the environment in which advice is given, influence trustee behaviour under the Retirement Income Covenant, and subtly reset what clients think a “reasonable” retirement outcome looks like, often before they ever sit down with an adviser.

The Principles sit alongside the Retirement Income Covenant, introduced in July 2022, which requires superannuation trustees to have a documented strategy to help members:

- maximise expected retirement income,

- manage longevity and investment risks, and

- maintain flexible access to savings.

The Covenant does not mandate specific products or advice models. Instead, it establishes outcome-focused objectives. The Principles clarify what good practice looks like in action.

While non-binding, the Principles are likely to influence regulator and set de facto benchmarks for trustee conduct.

The five core principles

Treasury has structured the guidance around five interconnected principles, intended to be read holistically rather than as a checklist.

1. Understanding members and their retirement income needs

The first principle emphasises deep, ongoing understanding of a fund’s membership.

Best practice includes:

- regular analysis of member demographics and characteristics, engagement preferences and retirement income needs;

- behavioural and retirement research;

- segmenting members approaching retirement into at least three distinct cohorts; and

tailoring solutions to those cohorts rather than offering a single default path.

Retirement solutions should reflect who members actually are, not who trustees assume them to be.

Why this matters for advisers:

In future, clients will increasingly seek advice with (fund informed) assumptions about spending needs, longevity, and product suitability. Advisers will likely need to understand, and sometimes challenge, these assumptions when providing personal advice.

2. Designing the elements of a quality retirement income solution

The second principle focuses on the building blocks of retirement solutions. Treasury’s guidance suggests trustees should:

- provide access to account-based pensions, lump sums, and a lifetime income product (other than the Age Pension); and

- design flexible product settings that allow for the construction of retirement income solutions that meet members’ retirement income needs, including:

- lifetime income product settings that have regard to member preferences around expected risk and return, for example managing longevity or investment risk;

- account-based pension product settings that help to manage expected risks, for example sequencing, market and inflation risks;

- trustee-designed drawdown pathways for account-based pensions that more efficiently convert superannuation balances into income than the legislated minimum drawdown rates.

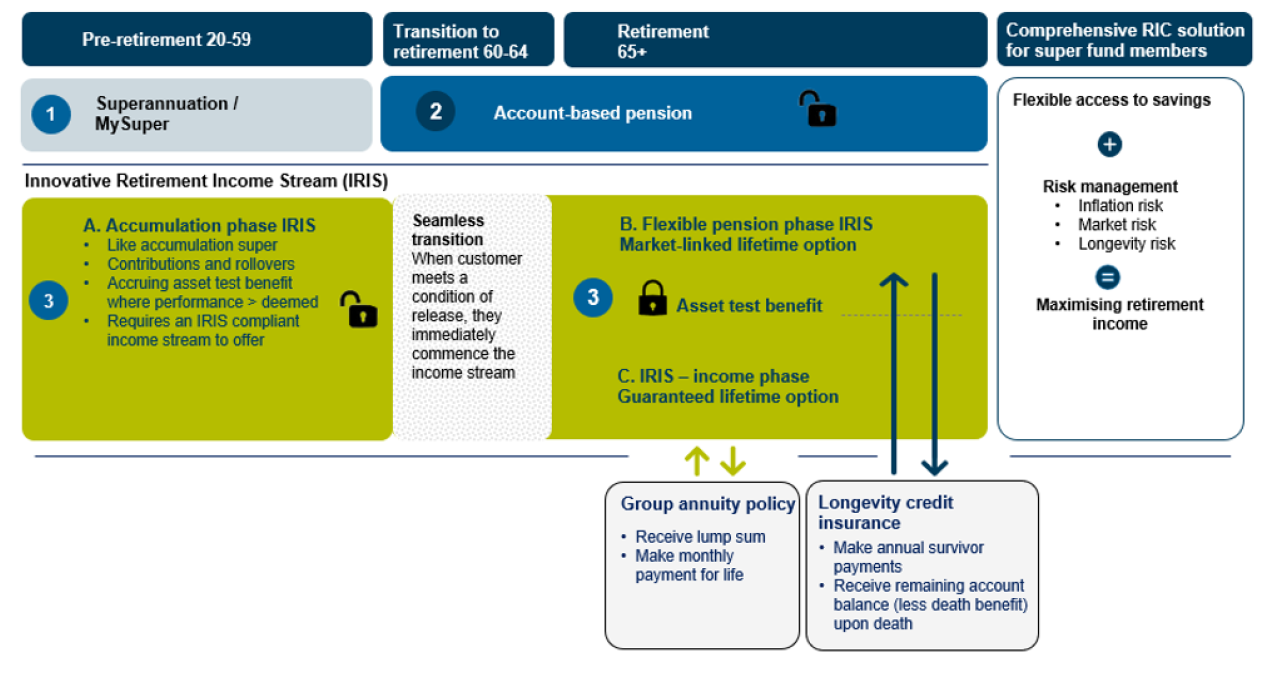

Many super funds have delivered, or are preparing to deliver, members comprehensive retirement income product solutions. The following diagram represents one version of what a comprehensive retirement income product solution might look like:

This diagram illustrates the existing super accumulation, TTR and account-based pension offerings of the fund being complemented by:

- an accumulation phase IRIS - enhancing retirement readiness while members are still accumulating with all the flexibility of the existing accumulation offering of the fund but with enhanced Centrelink outcomes for members in retirement;

- an investment-linked lifetime pension offering members with a whole-of-fund investment menu with lifetime income supported by annual longevity credits; and

a guaranteed lifetime pension with CPI-linked or fixed income payments for life supported by a guaranteed group annuity policy.

Why this matters for advisers:

Advisers can expect a broader presence of lifetime income products offered by superannuation funds. As trustees elevate these products, advisers will need to clearly articulate when they are appropriate and when alternative structures may better serve a client’s needs.

3. Combining products into cohort-based retirement solutions

Rather than promoting single products, the Principles encourage trustees to combine products and settings into trustee designed retirement income solutions for different member cohorts.

Examples may include:

- partial allocation to lifetime income,

- flexible account-based pension drawdown overlays,

- preserved liquidity for unexpected expenses, and

- explicit interaction with expected Age Pension eligibility.

Treasury explicitly acknowledges what advisers have always known, that one size fits all approaches do not work in retirement.

The Principles also suggest that superannuation funds design guidance services that assist members to understand and select the components of their retirement income solution, for example through personas or assisted choice tools.

Why this matters for advisers:

More clients will enter advice conversations already positioned within a trustee designed solution. Advisers will increasingly be asked whether to opt in, opt out, or modify those arrangements, shifting some advice from construction to evaluation and optimisation.

4. Engaging members to support informed decisions

The fourth principle centres on member communication and engagement. Best practice includes:

- providing income projections and forecasts;

- fostering member engagement by providing information and tools that can help members prepare for and understand their retirement income needs;

- supporting informed rather than passive decisions; and

- offering access to guidance and financial advice services that reflect member needs and preferences.

Why this matters for advisers:

Trustee communications will increasingly frame retirement income decisions before advice is sought. Advisers may be required to engage with, interpret, and sometimes recalibrate expectations created by trustee calculators, projections, and guidance tools.

5. Reviewing and improving solutions over time

Finally, the Principles emphasise continuous improvement. Trustees are expected to:

- review retirement solutions regularly;

- monitor member take up and outcomes;

- adapt solutions as member demographics evolve; and

- respond to changing economic and policy conditions

This principle aligns closely with APRA’s broader focus on measurable outcomes and accountability.

Why this matters for advisers:

As trustees iterate their solutions, advisers will operate in a dynamic product environment. Advice models will need to remain flexible and alert to trustee changes, especially where default settings evolve and member communications become more influential.

What the Principles mean for financial advisers

Although advisers are not directly regulated by the Principles, the influence of the Principles on advice is potentially significant.

1. A higher baseline for “reasonable” retirement solutions

Trustee designed solutions will likely become more sophisticated and better aligned with Covenant objectives. This raises the reference point against which advisers’ alternative recommendations may be implicitly compared.

Advisers should be prepared to:

- explain why deviating from trustee solutions is appropriate;

- demonstrate added value beyond defaults; and

- document how personal advice improves outcomes.

2. Greater client exposure to lifetime income

As trustees normalise lifetime income products, advisers will face better informed, but not always well understood, client questions about lifetime income (and other retirement income) solutions.

This creates opportunity for advisers to:

- clarify trade-offs;

- integrate lifetime income with broader retirement strategies; and

- ensure recommendations align with personal objectives rather than assumptions.

3. Increased importance of adviser/trustee literacy

Understanding a client’s fund provided retirement solution will become a core technical skill, particularly if these solutions grow more complex and less transparent.

In practice, this means:

- reviewing trustee retirement income strategies;

- identifying embedded assumptions; and

- positioning advice as either complementary or corrective.

4. Reinforcement of hybrid advice models

Treasury’s recognition of guidance and advice within trustee engagement reinforces the role of hybrid models that blend digital support with personal advice.

Well-positioned advisers can benefit by:

- partnering with fund ecosystems;

- offering scalable retirement advice; and

- focusing on higher complexity needs where personalisation matters most.

Conclusion

Treasury’s Best Practice Principles do not impose new obligations on financial advisers. However, they reshape the context in which advice is delivered, influencing products, defaults, communications, and client expectations.

For advisers, the message is not defensive but strategic. Understanding how trustee‑led retirement frameworks are evolving allows advisers to step forward, not step back, in adding and demonstrating client value.

The Principles mark another step toward a more integrated retirement income ecosystem, one in which professional advice remains essential, operating in partnership with trustee designed solutions.

Related content

Stay informed

Sign up to our free monthly adviser newsletter, Tech news containing the latest technical articles, economic updates, retirement insights, product news and events.