Understanding the Centrelink treatment of granny flats

A Granny flat is often defined as a self-contained unit within or attached to another home, or detached and on the same property as another home. While this is the real estate definition of a granny flat, the Centrelink definition of a granny flat interest is different.

Centrelink defines a granny flat interest as an agreement for accommodation for life and not a description of a type of dwelling. It is important to understand the Centrelink definition because of the implications for deprivation and homeownership status.

In this month’s article we will look at common granny flat arrangements and how they are treated for Centrelink purposes. We will use examples to demonstrate where deprivation will apply and how homeownership status is determined.

Granny flat interest

For Centrelink purposes, a granny flat interest is a life interest or right to accommodation for life if:

- the person pays for a life interest or right to accommodation for life; and

- the life interest or right to accommodation for life is in a private residence that is to be the person’s principal home.

Granny flat arrangements can allow a person to transfer assets to another person in exchange for a life interest without deprivation applying. The person can also be considered a homeowner with the value of the granny flat interest not assessed as an asset.

Typically, the amount paid for a granny flat interest is the same as the value of the granny flat interest and deprivation will not apply. Common granny flat arrangements where deprivation will not apply include:

- a person transfers the title of their home to another person in exchange for a life interest in that property or another property, or

- a person pays for the construction of premises on another person’s property in exchange for a life interest in that property, or

- a person purchases a property in another person’s name in exchange for a life interest in that property.

Reasonableness test

Where a person transfers assets in addition to the granny flat arrangements described above, Centrelink will apply a ‘reasonableness test’ to determine whether deprivation will apply. Centrelink will also apply the ‘reasonableness test’ where the value of the granny flat interest is indeterminate or the person enters into multiple granny flat arrangements. The ‘reasonableness test’ uses a formula to allow a granny flat interest to be valued at a different amount than the amount paid.

'Reasonableness test' amount:

Combined annual partnered pension rate x Conversation factor1

Where:

- the combined annual partnered pension rate is used irrespective of the person's marital status. The combined annual partnered pension rate is $41,7042; and

- the applicable conversion factor is based on the person's age next birthday. For partnered couples, the age of the younger member is used.

Note the extended land use test is disregarded where a person transfers the title of their home for the purposes of the ‘reasonableness test’. Adjacent land exceeding 2 hectares is considered additional assets and Centrelink will apply the ‘reasonableness test.

Example 1: Purchases a property and transfers additional assets

Maria is single, aged 73 and recently sold her home. Maria purchases a property worth $700,000 in her daughter’s (Melissa) name in exchange for a life interest in Melissa's home. Maria also pays Melissa an additional $100,000 for the life interest.

Maria has purchased a property and has transferred additional assets to Melissa therefore has triggered the ‘reasonableness test’. Maria's conversion factor is 14.25.

Reasonableness test amount = $41,704 x 14.25 = $594,282

Example 2: Value of the granny flat interest is indeterminate

Sally is single, aged 71 and recently sold her home. Sally pays $750,000 in cash to her daughter (Sarah) in exchange for a life interest in Sarah’s home.The value of the life interest is indeterminate as Sally paid cash therefore has triggered the ‘reasonableness test’. Sally’s conversion factor is 15.77.

Reasonableness test amount = $41,704 x 15.77 = $657,672.08

Value of a granny flat interest

The value of a granny flat interest is determined by the nature of the granny flat arrangement:

- Where a person transfers the title of their home AND transfers additional assets, the value of the granny flat interest is the greater of the value of the home and the ‘reasonableness test’ amount.

- Where a person pays for the construction of premises AND transfers additional assets, the value of the granny flat interest is the greater of the cost of construction and the ‘reasonableness test’ amount

- Where a person purchases a property AND transfers additional assets, the value of the granny flat interest is the greater of the value of the property and the ‘reasonableness test’ amount

Where a person enters into multiple granny flat arrangements or the value of the granny flat interest is indeterminate, the value of the granny flat interest is the lesser of the amount paid and the ‘reasonableness test’ amount.

Where a person does not transfer additional assets as part of the granny flat arrangements described above, the value of the granny flat interest is the same as the amount paid or value of assets transferred.

Example 3: Transfers the title of their home and transfers additional assets

Peter is single, aged 77 and owns his home worth $500,000. Peter transfers the title of his home to his son (Paul) in exchange for a life interest in Paul’s home. Peter also pays Paul an additional $150,000 for the life interest.

Peter has transferred the title of his home and has transferred additional assets to Paul therefore has triggered the ‘reasonableness test’. Peter's conversion factor is 11.37.

Reasonableness test amount = $41,704 x 11.37 = $474,174.48

The value of the home ($500,000) is greater than the ‘reasonableness test’ amount ($474,174.48) therefore the value of the granny flat interest is $500,000.

Example 4: Value of the granny flat interest is indeterminate

Charles is single, aged 78 and recently sold his home. Charles pays $450,000 in cash to his son (Chris) in exchange for a life interest in Chris’s home. The value of the life interest is indeterminate as Charles paid cash therefore has triggered the ‘reasonableness test’. Charles’s conversion factor is 10.70.

Reasonableness test amount = $41,704 x 10.70 = $446,232.80

The ‘reasonableness test’ amount ($446,232.80) is less than the amount paid for the granny flat interest ($450,000) therefore the value of the granny flat interest is $446,232.80.

Example 5: Pays for the construction of premises but does not transfer additional assets

Steven is single, aged 72 and recently sold his home. Steven pays his son (Simon) $400,000 for the construction of a granny flat at Simon’s home in exchange for a life interest. Simon constructs a granny flat at his home for Steven at a cost of $400,000.Steven has paid for the construction but has not transferred additional assets to Simon therefore the value of the granny flat interest is $400,000.

Example 6: Pays for the construction of premises and transfers additional assets

Jacqueline is single, aged 75 and recently sold her home. Jacqueline pays her daughter (Josephine) $600,000 for the construction of a granny flat at Josephine’s home in exchange for a life interest. Josephine constructs a granny flat at her home for Jacqueline at a cost of $300,000.

Jacqueline has paid for the construction and has transferred additional assets to Josephine therefore has triggered the ‘reasonableness test’. Jacqueline's conversion factor is 12.78.

Reasonableness test amount = $41,704 x 12.78 = $532,977.12

The ‘reasonableness test’ amount ($532,977.12) is greater than the cost of construction ($300,000) therefore the value of the granny flat interest is $532,977.12.The amount paid for the granny flat interest ($600,000) exceeds the value of the granny flat interest ($532,977.12) therefore deprivation will apply.

Deprivation amount = $600,000 - $532,977.12 = $67,022.88

If Jacqueline has not disposed of any other assets previously, the amount in excess of the disposal free area ($57,022.88) will be assessed under the assets test and deemed under the income test for five years after the granny flat interest was created

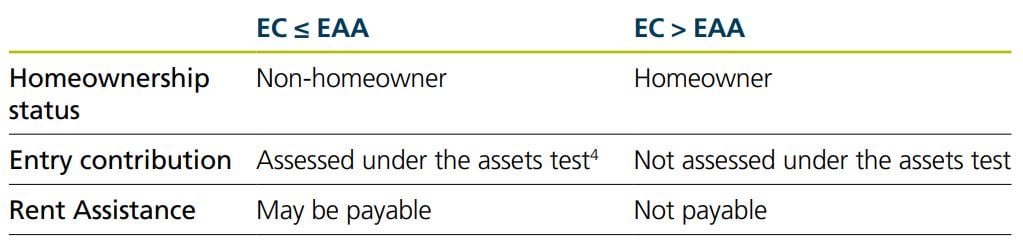

Homeownership To determine whether a person is considered a homeowner when a granny flat interest is created, the entry contribution (EC) is compared with the extra allowable amount (EAA). The EC is determined as follows: • If the ‘reasonableness test’ does not apply, the EC is the amount paid for the granny flat interest • If the ‘reasonableness test’ applies: – If the amount paid for the granny flat interest is more than the ‘reasonableness test’ amount, the EC is the value of the granny flat interest – If the amount paid for the granny flat interest is less than the ‘reasonableness test’ amount, the EC is the amount paid The EAA ($242,0003 ) is the difference between the homeowners and non-homeowners lower assets test thresholds. The following table summarises the rules for determining when a person is considered a homeowner or non-homeowner when a granny flat interest is created.

Note where a person sells their home and intends to use the proceeds to create a granny flat interest, the proceeds from the sale can be exempt under the assets test for up to 24 months. The person will continue to be considered a homeowner during the exemption period.

Example 7: Purchases a property but does not transfer additional assets

Malcolm is single, aged 74 and recently sold his home. Malcolm purchases a property worth $650,000 in his son’s (Michael) name in exchange for a life interest in Michael’s home.

Malcolm has purchased a property but has not transferred additional assets to Michael therefore has not triggered the ‘reasonableness test’.

Where the ‘reasonableness test’ does not apply, the entry contribution is the amount paid for the granny flat interest ($650,000). The entry contribution ($650,000) is greater than the extra allowable amount ($242,000) therefore Malcolm will be considered a homeowner.

Example 8: Transfers the title of their home and transfers additional assets

Andrea is single, aged 76 and owns her home worth $550,000. Andrea transfers the title of his home to her daughter (Angela) in exchange for a life interest in Angela’s home. Andrea also pays Angela an additional $250,000 for the life interest.

Andrea has transferred the title of her home and has transferred additional assets to Angela therefore has triggered the ‘reasonableness test’. Andrea's conversion factor is 12.07.

Reasonableness test amount = $41,704 x 12.07 = $503,367.28

Where the ‘reasonableness test’ applies, if the amount paid for the granny flat interest ($800,000) is more than the ‘reasonableness test’ amount ($503,367.28), the entry contribution is the value of the granny flat interest.

The value of the home ($550,000) is greater than the ‘reasonableness test’ amount ($503,367.28) therefore the value of the granny flat interest is $550,000. Andrea’s entry contribution is the value of the home ($550,000). The entry contribution ($550,000) is greater than the extra allowable amount ($242,000) therefore Andrea will be considered a homeowner.

Related content

1 Conversion factors can be found in the Social Security Guide on the Department of Social Services website at https://guides.dss.gov.au/guide-social-security-law/4/6/4/60.

2 Rates and thresholds as at 1 July 2023.

3 Rates and thresholds as at 1 July 2023.

4 Entry contribution is not deemed under the income test.

Stay informed

Sign up to our free monthly adviser newsletter, Tech news containing the latest technical articles, economic updates, retirement insights, product news and events.