Using personal deductible contributions to fund retirement income

Using personal deductible contributions to fund retirement income

Download the full article below.

Personal deductible contributions (PDCs) have become an increasingly powerful tool for individuals looking to strengthen their retirement income. The ability to make personal contributions to super and claim a tax deduction has allowed additional savings to be accumulated in a tax‑effective environment and to build a more secure income stream in retirement. Since PDCs were introduced, there has been a range of changes to the eligibility rules and the contribution limits over time.

The removal of the former 10% rule in 2017 significantly expanded access to PDCs. What was once a strategy available only to a narrow group, primarily the self‑employed, became a mainstream approach open to anyone (subject to eligibility) with assessable income. Additionally, the ability for eligible individuals to contribute higher concessional contributions (CC) utilising unused caps from the five previous years from July 2018 further extended the usefulness of PDCs into a prominent tax efficient vehicle.

This article provides an overview of the current eligibility rules and highlights key considerations, opportunities, and potential pitfalls when using PDCs as part of a retirement income strategy.

A quick recap of the rules

Broadly speaking, a PDC enables an individual to make a contribution using their personal after‑tax monies and have that contribution being reclassified as a CC upon claiming a tax‑deduction. Certain steps and conditions are required to be met to ensure the contribution is classified as a CC.

1. Eligibility to make PDCs

- Check available CC cap space before contributing. The CC cap for 2025–26 is $30,000.

- Individuals with a total super balance (TSB) under $500,000 on 30 June of the previous financial year may use unused CC cap amounts from the previous five years.

Individuals aged 67–74 must meet the work test or work test exemption. Voluntary contributions can be made until the 28th day of the month after the month in which they turn 75. Refer to the ATO page for the compliance rules on work test/work test exemption.

2. Notice of intent

A valid notice of intent (in an approved form) must be lodged to the super fund to claim a deduction1. It must be submitted by the earlier of:

– the date the tax return is lodged for the year of contribution, or

– the end of the following income year in which the contribution is made.- The fund will acknowledge receipt once the notice is accepted.

- A notice may be invalid if:

– the individual has left the fund (e.g., full rollover or withdrawal),

– the fund no longer holds the contribution (e.g., partial or full withdrawal/ rollover),

– the contribution has been used to start an income stream. - A notice cannot be withdrawn or revoked. To increase the amount to be claimed as a deduction, another valid notice can be lodged. To reduce the amount claimed as a deduction (including to nil), a notice of intent can be varied using the approved form. Where an individual intends to make multiple contributions throughout the year, it could be worthwhile waiting until the latter part of the year to submit the notice in order to avoid complications and errors.

- A notice of intent can be varied at any time up until the due date for lodging a deduction claim. If the ATO later determines that all or part of the deduction is not allowable, you may still vary the notice after the deadline, but only to reduce the amount claimed by the disallowed portion.

- Individuals who intend to split contributions to their spouse and intend to claim a deduction must lodge the notice of intent before lodging the contribution splitting claim.

3. Claiming the deduction in the tax return

- The final step in the process is to claim the tax deduction of the amount stated in the notice at the time of lodging the tax return for the year in which the contribution is made.

Strategic considerations

Tax on contributions

Before making a contribution, it is important to ensure there is enough assessable income earned for the financial year in which the contribution is being made. This is because the amount a person can deduct is limited to a person’s assessable income less their other deductions. A deduction for personal superannuation contributions cannot add to or create a tax loss.

Note that the ATO can still deny a tax deduction from a valid notice of intent if the person’s assessable income is below the amount in the notice. Given that the deduction amount denied by the ATO is added to the person’s other non‑concessional contributions (NCC), this can cause the person to unintentionally trigger the bring‑forward rules or even exceed their NCCs for that income year.

Besides the technicality of ensuring there is adequate assessable income to cover the stated deduction amount, it is also important to consider whether this reduces the taxable income to below the tax‑free threshold. The comparison of tax paid on income outside super with the 15% tax on CCs within super is recommended. This is even more pertinent where the individual may end up paying Division 293 tax. Division 293 tax is an additional 15% tax on CCs (part or full) for individuals with an income threshold of $250,000. Refer to the ATO page to understand when Division 293 tax can be levied.

PDCs are reportable superannuation contributions. Therefore, it is important to consider that making PDCs can impact any income tested government benefits where reportable superannuation contributions are included.

1 Note that a deduction cannot be claimed for ineligible contributions like employer contributions (e.g. salary sacrifice), rolled over amounts, transfers from foreign super funds, First Home Super Saver contributions, contributions to certain public sector or untaxed/constitutionally protected funds, contributions specified as excluded under regulations and downsizer contributions.

Catch-up concessional considerations

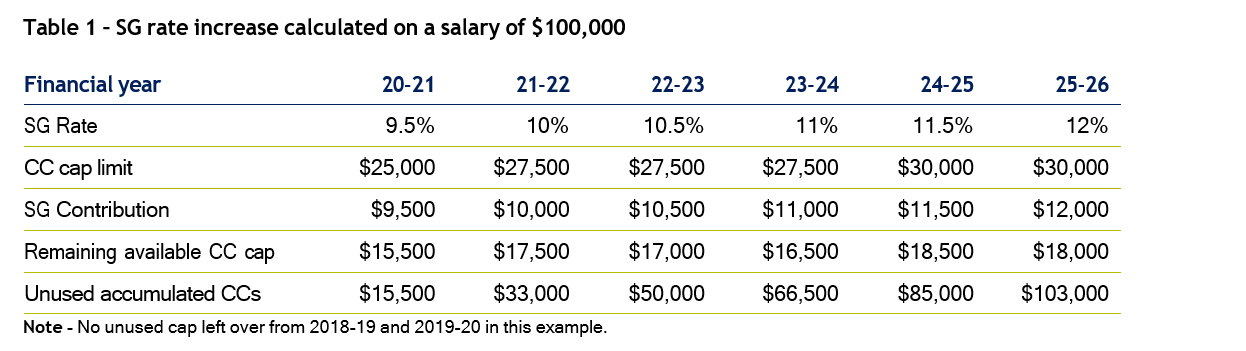

Eligible individuals can utilise their unused cap from 2020‑21, 2021‑22, 2022‑23, 2023‑24, 2024‑25 and can contribute in 2025‑26, subject to the TSB being under $500,000 on 30 June 2025. Table 1 outlines an example of the calculation of a salary of $100,000 a year and the unused accumulated CC cap after taking SG into consideration. Assuming no indexation on salary and no additional contributions being made until now, the last row shows the total of the existing year’s cap plus the amount accumulated that is available to be used.

The ability to utilise unused cap from previous years can be particularly helpful when an individual makes a large capital gain which can be contributed to super on which they can claim a tax deduction if eligible.

Case Study 1

Jurgen, aged 62, has not made any voluntary CCs since 1 July 2021. In January 2023, he sells part of his share portfolio. As of 30 June 2022, Jurgen’s TSB was $150,000. This allowed him to reduce his assessable capital gains by making a PDC of $50,000 to superannuation, utilising his available CC cap from 2022‑23 along with unused caps from previous years.

Maximising PDCs to fund retirement income streams

Many young families with high cash flow needs who are paying off their mortgage in early years may not necessarily have excess savings left to voluntarily contribute. In such cases, PDCs using catch‑up concessional provisions can be particularly valuable for those seeking to accelerate their retirement savings later in their careers or after periods of irregular contributions.

By making larger tax deductible contributions in selected years, individuals can meaningfully increase the capital available to generate income in retirement.

Whilst these contributions made by pre‑retirees can be accessed as a lump sum at retirement, a wide range of innovative retirement income streams, including lifetime annuities, can be used in combination with other income streams to help improve client retirement outcomes.

Case Study 2

Yui turned 65 in January 2026, she is due to receive a lump sum termination payment of $175,000 on 1 July 2026. She has unused CC cap of $53,000 left over from 2023‑24, 2024‑25 and 2025‑26. She can make a PDC of up to $85,500 (including the available CC cap of $32,500 from 2026‑27). Assuming Yui’s TSB on 30 June 2026 is $350,000, she intends to make a personal contribution of $200,000 to superannuation in July 2026.

She will lodge a notice of intent at the time of making a contribution and will claim a deduction of $80,000 in the notice. The remaining $120,000 will be her NCC for 2026‑27. Once she receives an acknowledgement from the fund, she wants to consider her options to access her retirement savings.

Yui owns her home and has $50,000 left in her bank account after her contributions to super. She also has home contents worth $10,000. She wishes to start an account‑based pension with her $550,000 in superannuation savings. However, despite a tax‑efficient retirement planning, Yui is concerned about running out of her savings over a longer term. She also has a desire to provide for her grandkids when she passes away.

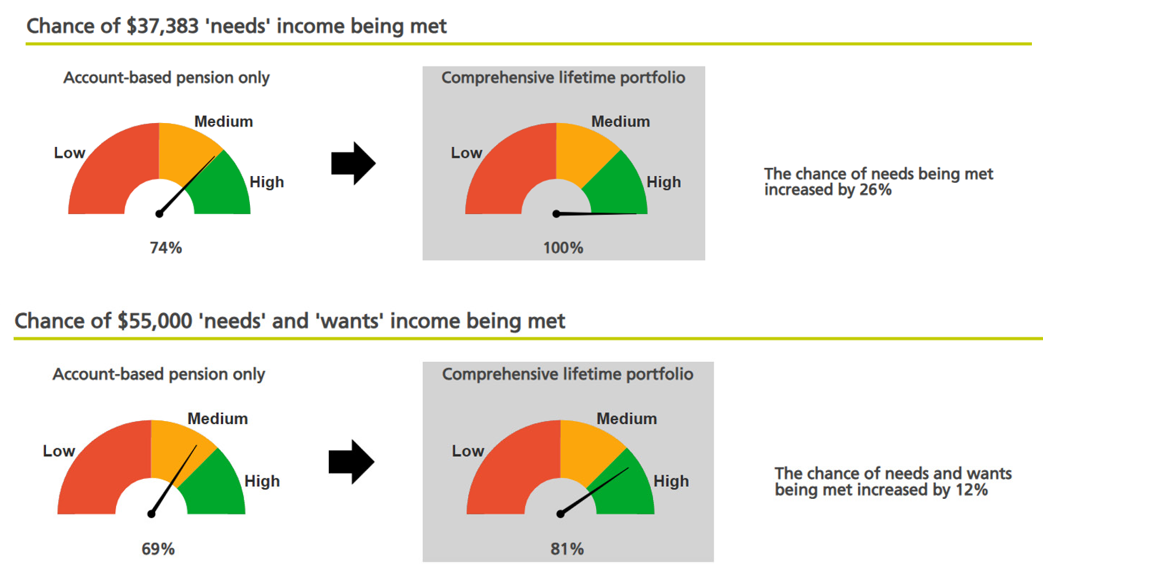

She estimates a retirement income of $55,000 p.a. to keep up with the cost of living. This is in line with the current ASFA ‘Comfortable’ Retirement Standard for a single of $54,250 p.a. (based on September 2025 quarter). To address Yui’s longevity concern and to meet her retirement objectives, her adviser recommends an income layering strategy using a blend of income streams.

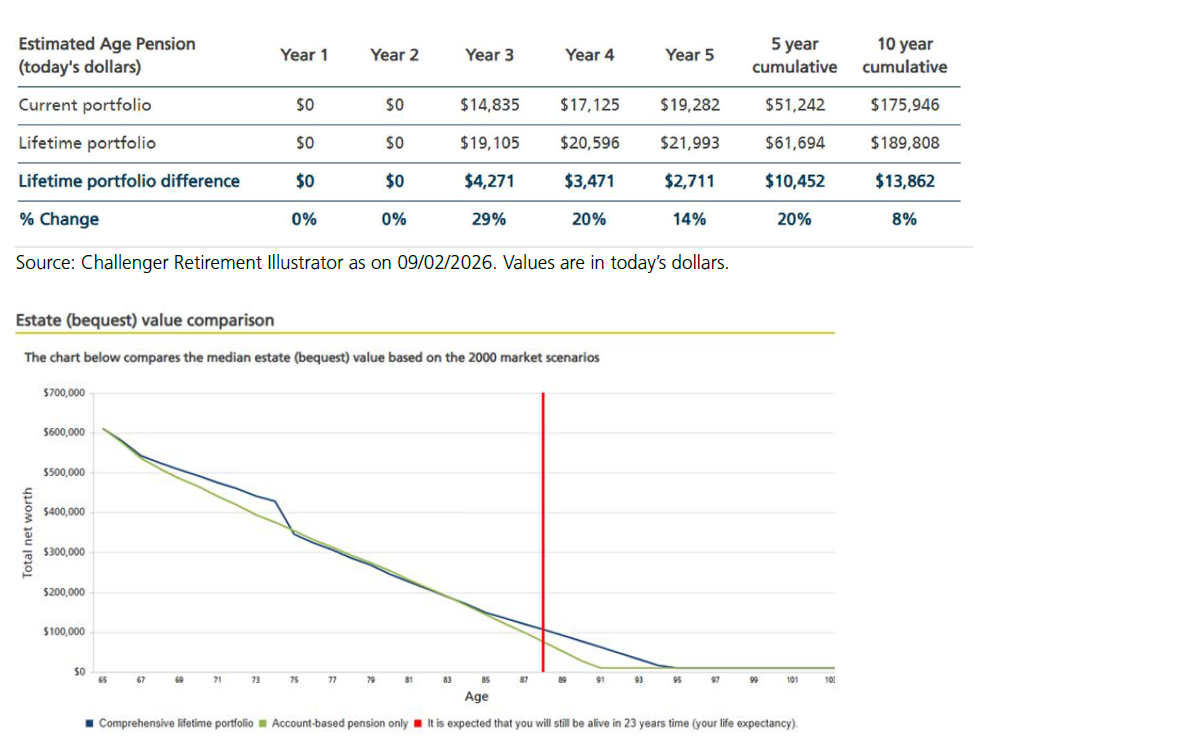

Using Challenger’s Retirement illustrator (accessible to all financial planners via Challenger’s AdviserOnline portal), the stochastic modelling below compares a portfolio of the entire $550,000 allocated to account‑based pension with a blended portfolio that includes a 30% allocation to lifetime annuity. The dials depict Yui’s likelihood of meeting her objectives based on her life expectancy.

In 2 years when Yui reaches Age Pension age, the blended portfolio provides her with an increased Age Pension outcome in addition to a lifetime income starting at $9,370 in the first year, fully indexed for inflation, for as long as she lives. Furthermore, this enhanced strategy is also likely to help improve Yui’s estate value at the end of 23 years (life expectancy) by $40,996.

Excess considerations

Where an individual realises that they have exceeded the cap, they can submit a notice to vary down (if within the time frame outlined above) the amount they intend to reclassify as a CC. However, this would mean that the amount contributed will continue to be counted towards NCC. Considering this was not the original intention, this could mean the NCC cap may be inadvertently breached if the individual has no available NCC cap space for the year or their TSB exceeded the general transfer balance cap on 30 June prior to the year in which the contribution was made.

These issues are helpful to note before providing advice on making contributions for the year to avoid unintended excess consequences. Refer to the ATO page for details on excess NCC process.

Frequently asked questions

Related content

Stay informed

Sign up to our free monthly adviser newsletter, Tech news containing the latest technical articles, economic updates, retirement insights, product news and events.