What could proposed tax changes mean for the economy?

Subscribe to Macro Musing

To stay up to date on the latest economic insights, subscribe to Macro Musing on LinkedIn.

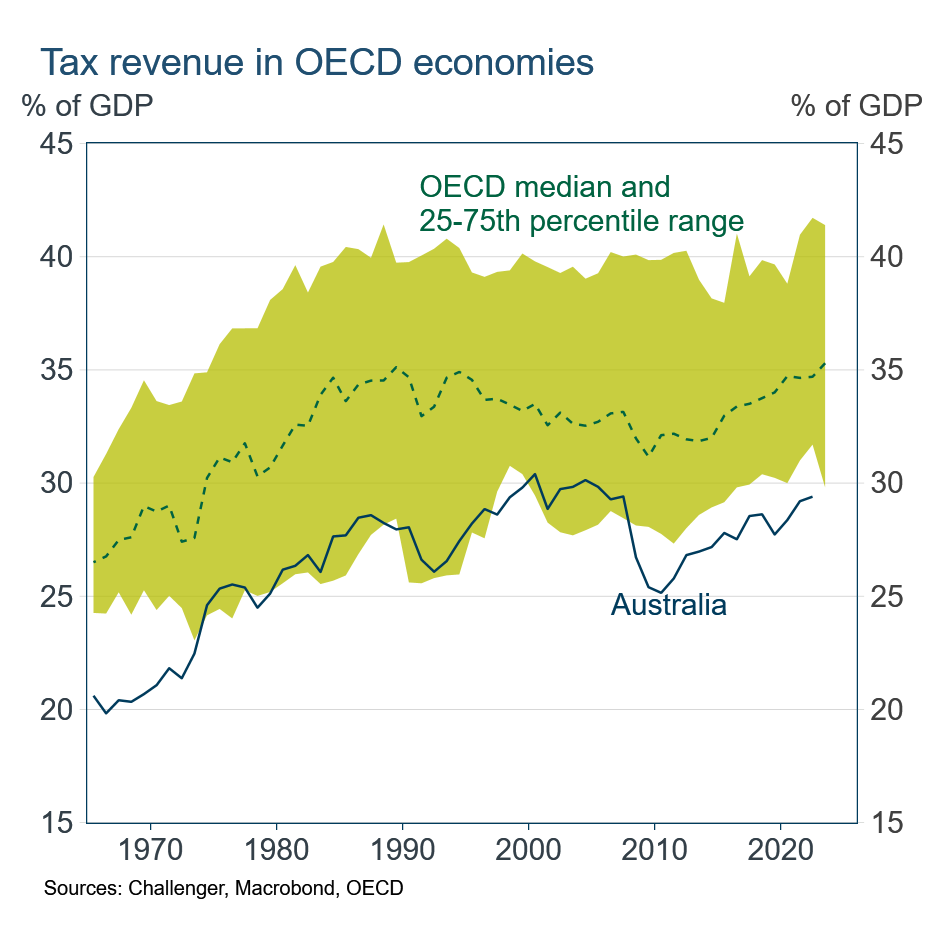

The past week has seen a focus on tax, given Budget announcements on changes to the Capital Gains Tax (CGT), negative gearing and the taxation of trusts. Some commentary on these changes might lead you to think Australia is a high-tax country. It is not. Out of 30 wealthy economies (OECD countries), Australia is in the bottom quarter in terms of tax revenue as a share of GDP.

However, just because we don’t have high taxes doesn’t mean our tax system is efficient. An efficient tax system is important to ensure we don’t disincentivise businesses and individuals from working efficiently. It can also make tax avoidance more difficult.

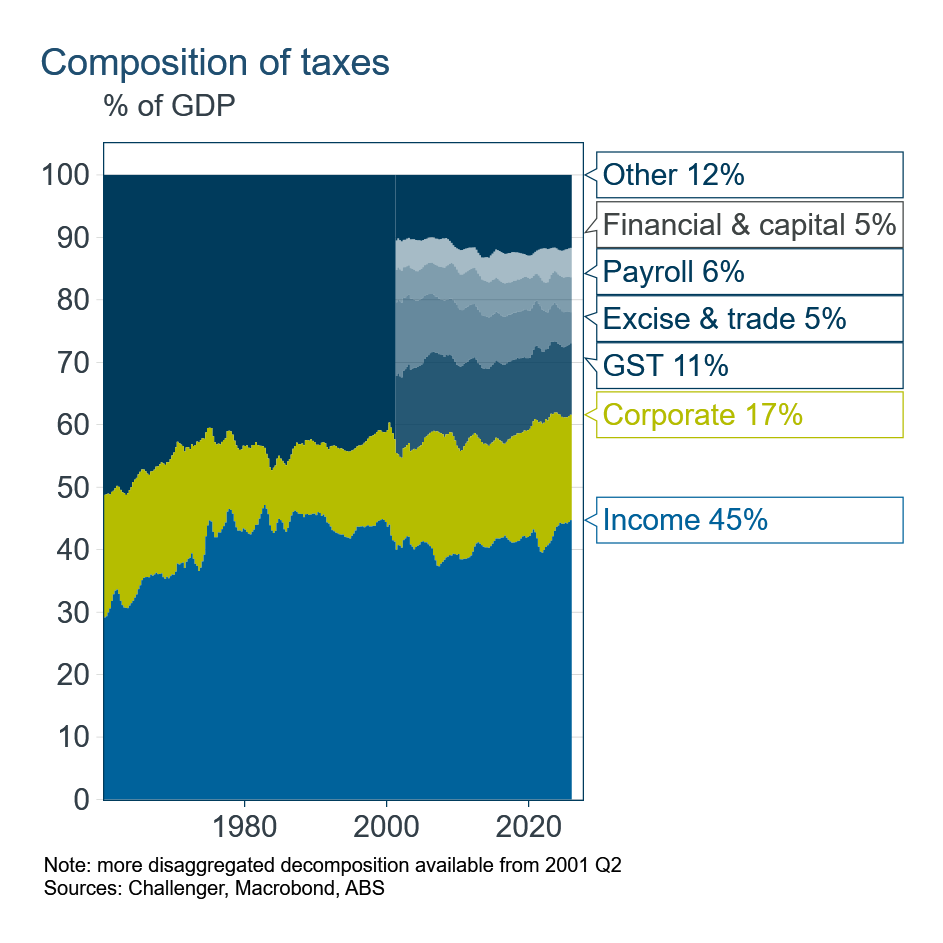

At 45%, too large a share of our tax revenue come from income taxes which can discourage people from working. Internationally this is a high share. Other countries also levy social security contributions to fund unemployment benefits, pensions and similar payments. Australia does not have social security contributions, instead funding these payments from general revenue. However, because social security contributions are typically levied on employers, they don’t affect workers’ incentives in the same way as income taxes.

Corporate and payroll taxes, two other significant sources of tax revenue in Australia are also relatively inefficient.

The Budget has proposed reverting to the CGT method to indexing the purchase price by CPI inflation, the method that applied prior to 1999, rather than applying the 50% discount on capital gains that has applied since then.

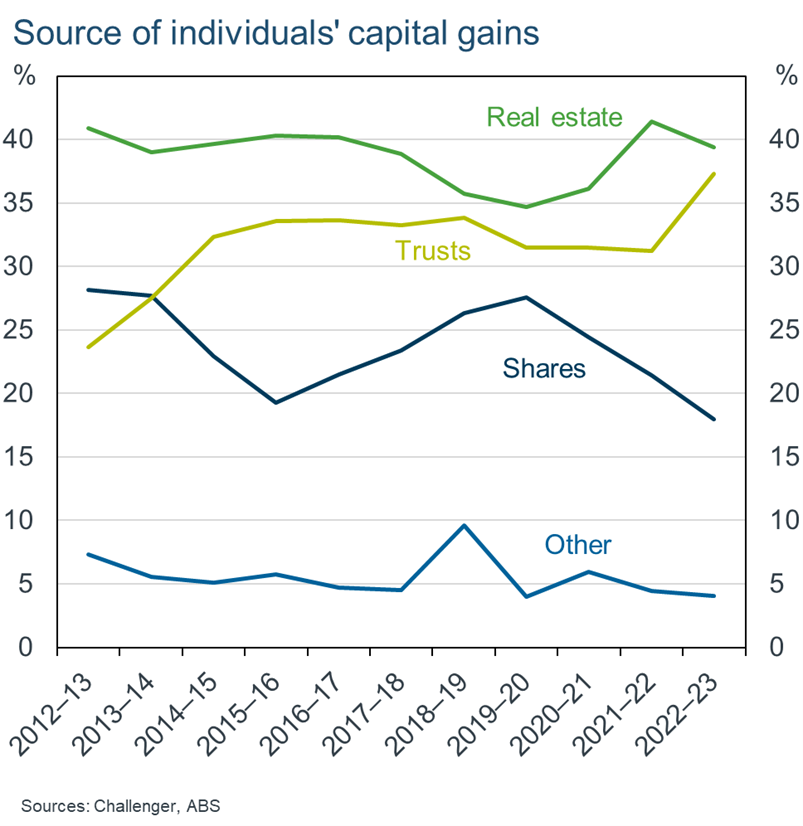

One surprise in the Budget was that this change applies to all assets and not just housing, given the stated goal of addressing intergenerational equity by improving housing affordability. Applying an indexed CGT regime to all assets not only avoids creating a more complex system – which opens up more avenues for avoidance – but also raises more revenue. Profits on real estate sales account for only 40% of individuals’ capital gains; the majority comes from shares and trusts.

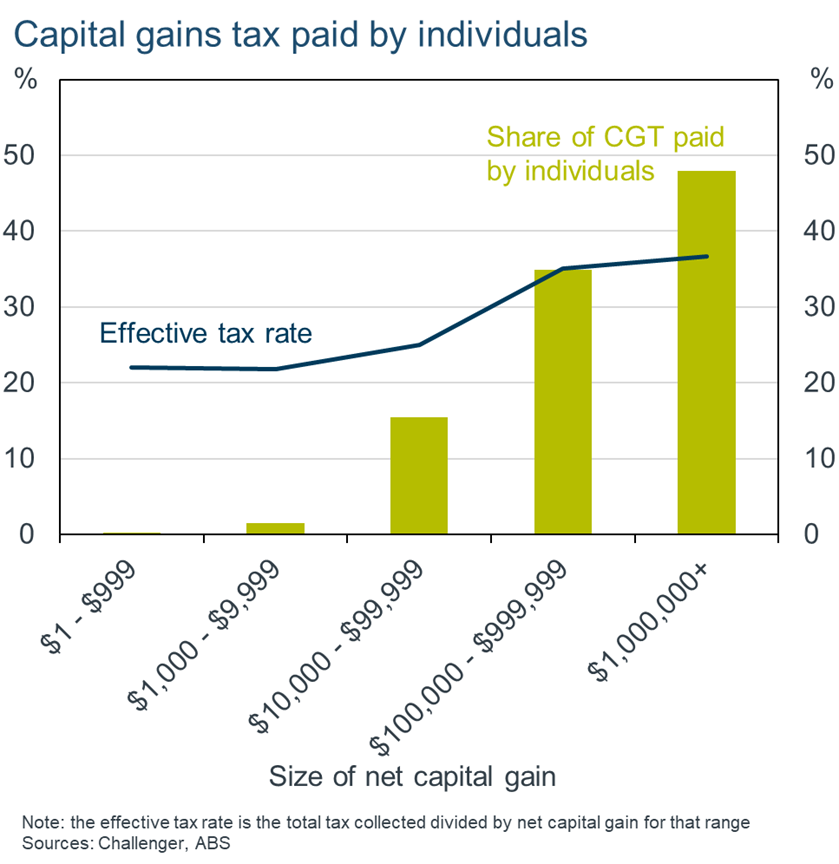

The CGT changes will disproportionately affect wealthier Australians. The Government noted that individuals in the top 1% of lifetime earnings account for around one-third of net capital gains income. Those in the top 10% account for more than half of net capital gains income.

This is consistent with data on the CGT revenue by the size of net capital gain. Almost half of all CGT revenue comes from gains greater than $1 million. Over 80% of CGT revenue comes from net capital gains exceeding $100,000. The average tax rate increases with the size of the capital gain, reinforcing the intuition that larger capital gains are typically earned by those facing higher marginal tax rates.

It was encouraging to see some tax reform in the Budget – even if there is some disagreement on its form. Hopefully this can be the first step in a broader reform process, and that the reaction does not deter this or future governments from implementing changes that improve the efficiency of the tax system and so can contribute to boosting our ailing productivity growth.

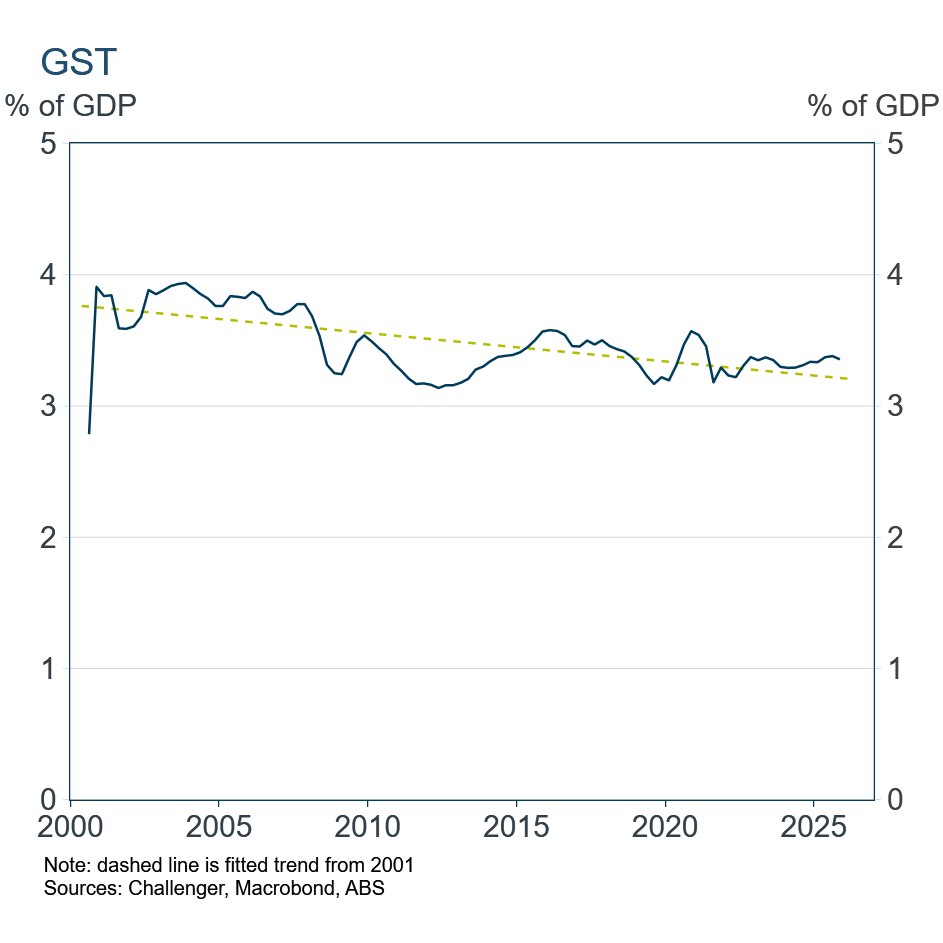

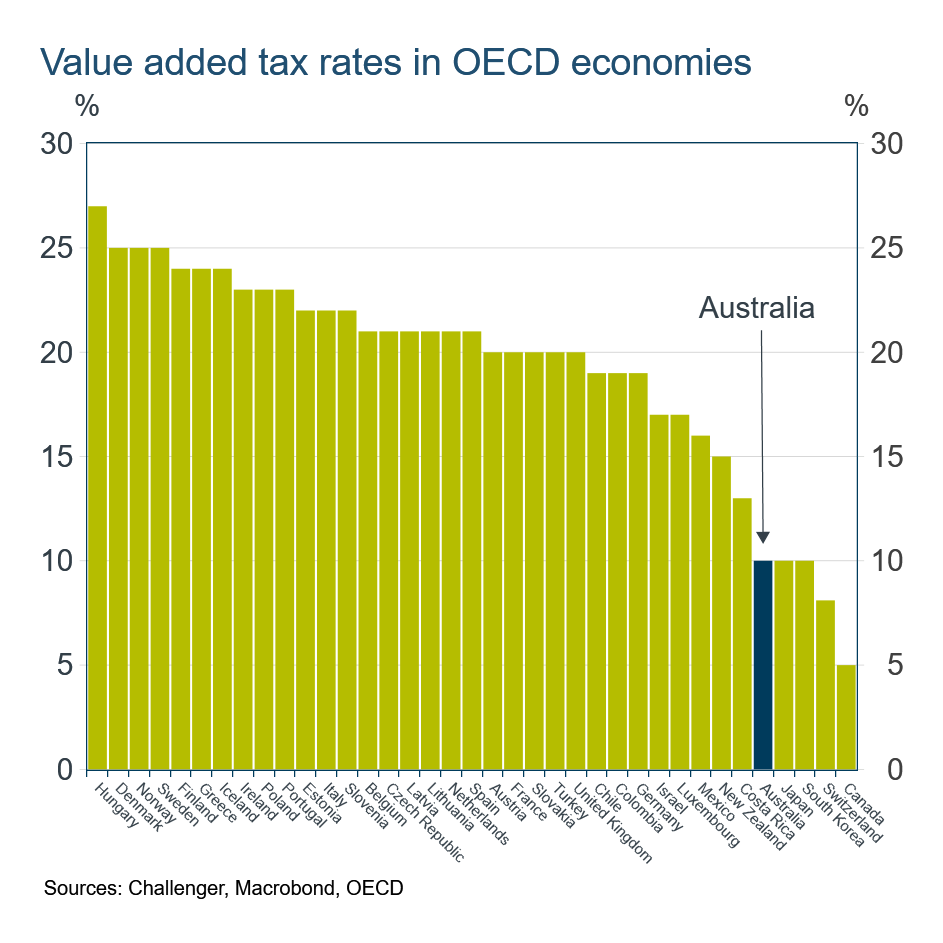

One tax widely considered more efficient is the Goods and Services Tax (GST). The GST is difficult to avoid and ensures that those who spend more, pay more. Australia’s GST, a value added tax in international terminology, is very low relative to other OECD economies where the norm is around 15–20%.

Over time, our 10% GST has also been generating less revenue relative to the size of the economy. This is because the GST base is relatively narrow with many exemptions including medical aids and appliances, prescription drugs and most food. As Australians become wealthier and older we are spending a larger share of our income on healthcare, meaning GST revenue as a share of consumption is likely to continue declining.

Other fruitful areas for tax reform would involve coordination between Federal and state governments to reduce or eliminate inefficient taxes such as stamp duty and payroll tax. Let’s hope this Budget is the first step in evidence-based tax reform.