What fees apply to grandfathered home care recipients?

What fees apply to grandfathered home care recipients?

Download the full article below.

As part of the aged care reforms that took effect on 1 November 2025, the former Home Care Packages (HCP) program was replaced with the new Support at Home program. The changes provide transitional and grandfathering (also known as “grandparenting”) provisions for existing HCP recipients including a different calculation for participant contributions (fees) for grandfathered HCP recipients compared to those who will be subject to the new rules under Support at Home.

Transitioned funding arrangements

All Home Care Package recipients as at 31 October 2025, including those who were in the National Priority System, were transitioned over to the new Support at Home program on 1 November 2025.

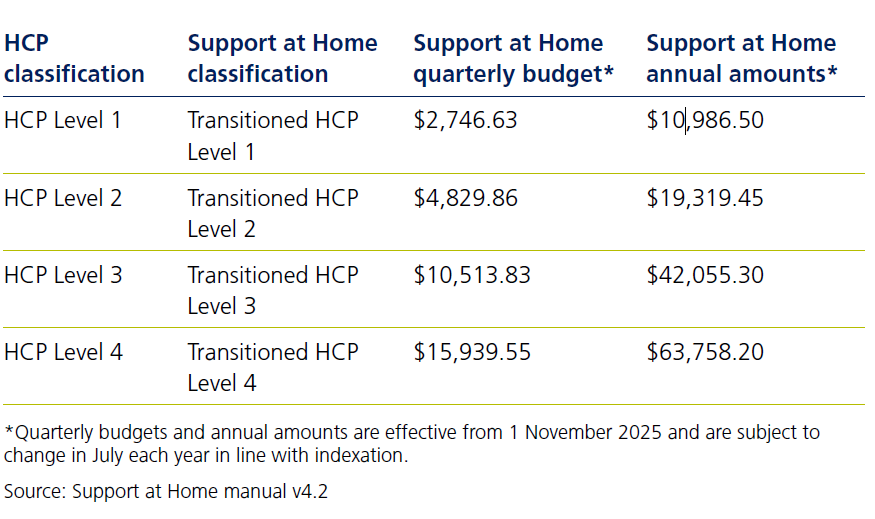

Transitioned HCP recipients will continue to receive an equivalent level of funding (including supplements) as their previous HCP. Their previous annual package amount will be divided into four to create an equivalent Support at Home quarterly budget (see table below).

Those who were waiting for a HCP to be allocated to them on 31 October 2025 will receive an equivalent level of funding to their approved HCP when it becomes available. If a transitioned HCP recipient requires a higher level of funding, they will need to be reassessed and approved for a higher Support at Home classification.

Participant contributions for transitioned recipients who are not grandfathered

Transitioned HCP recipients who were approved for a Home Care Package after 12 September 2024 will have the new participant contribution rules under the Support at Home program apply to them from 1 November 2025.

They will no longer pay the basic daily fee or income tested fee that previously applied to them (if any). If a transitioned HCP recipient receives a pension, Services Australia/DVA will calculate their new participant contributions based on the income and assets information they already have. For non-pensioners, Services Australia/DVA will request income and assets information from the recipient from 1 November 2025.

The new participant contribution rules mean that those who previously didn’t pay a basic daily fee or income tested fee, may become liable for a participant contribution based on their means and types of services they access.

For information on the new participant contributions under the Support at Home program, including how they are calculated, refer to our technical paper “Home Care Packages to support at home – advice considerations”.

Participant contributions for grandfathered recipients

A HCP recipient who, on or before 12 September 2024, was either receiving a package, in the National Priority System, or assessed as eligible for a package will be subject to the no worse off principle for their participant contributions.

The no worse off principle will allow these recipients who on 31 October 2025:

- were not required to pay an income-tested fee, to continue to make no participant contributions for the remainder of their time under Support at Home.

- were required to pay an income-tested fee, to pay participant contributions that are the same or less under Support at Home.

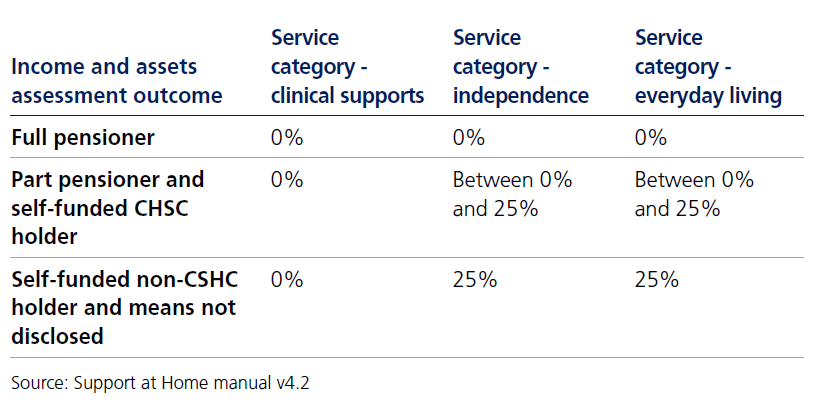

The table below summarises the participant contributions for the different pensioner status of grandfathered HCP recipients under the no worse off principle.

Calculating participant contributions for grandfathered part-pensioners and CSHC holders

The methodology for calculating participant contributions under the no worse off principle differs to that of other Support at Home recipients. Participant contributions under the no worse off principle will be based solely on assessable income compared to assessable income and assets for those who are not grandfathered. Assessable income and assets under the Support at Home Program will be the same as those assessed for Centrelink/DVA income support payments such as the Age Pension.

The methodology for working out participant contributions under the no worse off principle is as follows:

Step 1: Work out the income reduction amount

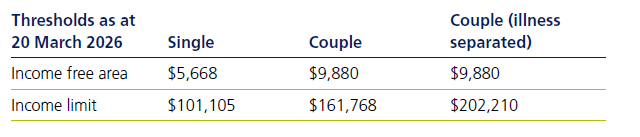

(Assessable income - income free area) x 50% (round to nearest dollar)

Step 2: Work out the maximum reduction amount

(Income limit - income free area) x 50% (round to nearest dollar)

Step 3: Work out the input contribution rate

(Step 1 / Step 2) x 100

Step 4: Work out the percentage contribution

Independence (Step 3 x 0.25) rounding to 2 decimal places

Everyday living (Step 3 x 0.25) rounding to 2 decimal places

In addition to having contribution rates based solely on assessable income, there will be a fortnightly cap, based on the recipient’s previous income tested fee calculation, to ensure they don’t pay more than what they would’ve paid under the old income tested fee arrangement.

Example:

The following example is based on the example in Services Australia’s operational guide and the latest income thresholds detailed above.

John (single homeowner), age 80 is a Home Care Package level 3 recipient since July 2024. His level 3 package provides him with $42,055 p.a. (less any contributions made by John as an income tested fee) in government funding to use towards his services.

John’s level of government funding (subject to indexation) for his package will continue post 1 November 2025 but will be broken down into quarterly budgets of $10,514. He can continue to access his usual services from this budget.

John previously paid an income tested fee of $7.07 per day based on his means (assessable income). His HCP provider did not require him to pay a basic daily fee.

As John was a Home Care Package recipient on or before 12 September 2024, his contributions will be grandfathered under the no worse off principle.

His participant contributions going forward will be calculated as follows (his assessable income for the purposes of calculating his contribution rates is assumed to be $26,000 p.a.):

Step 1: Work out the income reduction amount

($26,000 - $5,668) x 50% = $10,166

Step 2: Work out the maximum reduction amount

($101,105 - $5,668) x 50% = $47,719

Step 3: Work out the input contribution rate

($10,166 / $47,719) = 21.30388

Step 4: Work out the percentage contribution

Independence (Step 3 x 0.25) rounding to 2 decimal places

21.30388 x 0.25 = 5.33%

Everyday living (Step 3 x 0.25) rounding to 2 decimal places

21.30388 x 0.25 = 5.33%

John will need to contribute 5.33% of the cost of services in the ‘independence’ and ‘everyday living’ categories but will not pay more than $98.98 per fortnight ($7.07 x 14).

Related content

Stay informed

Sign up to our free monthly adviser newsletter, Tech news containing the latest technical articles, economic updates, retirement insights, product news and events.