Home Care Packages to support at home – advice considerations

Home Care Packages to support at home – advice considerations

Download the full article below.

Changes effective 1 November 2025 replaced the government subsidised Home Care Packages (HCP) with the new Support at Home program. Being familiar with the new program can help you keep your clients informed on what to expect, understand the impact of the costs of care on client’s cash flow and present strategic advice considerations.

This article outlines the Support at Home program and identifies advice considerations and opportunities.

Assessment

The process of getting assessed before allocating the funding remains the same as the former HCP. Individuals seeking subsidised care need to register with My Aged Care and have an aged care assessment. The outcome of the assessment will be provided in a detailed Notice of Decision letter.

Where an individual is eligible for Support at Home, they will be placed in the Support at Home Priority System and will be contacted when their allocated funding becomes available. When a letter allocating the funding is received, individuals will have 56 days to accept their place by entering into a service agreement with their chosen service provider. The service agreement outlines rights and responsibilities, what services will be provided to the client, and what prices will be charged.

If the person does not enter into a service agreement within this timeframe, their funding will be withdrawn, and they will be removed from the Support at Home Priority System. They can later rejoin the Support at Home Priority System by contacting My Aged Care when they decide to receive home care services. Unless their needs have changed, those looking to rejoin will not need another aged care assessment.

HCP recipients who were receiving a package, on the National Priority System, or assessed as eligible for a package on or before 12 September 2024 are grandfathered under a ‘no worse off’ principle. Accordingly, for advisers onboarding new clients who may have only recently been allocated a package, it is important to establish whether the client qualifies for grandfathering.

This can be confirmed by determining whether the client was in the National Priority System, or assessed as eligible for a Home Care Package, as at 12 September 2024. In practice, this would typically be evidenced by an ACAT assessment /outcome letter or My Aged Care correspondence dated on or before 12 September 2024.

Where this condition is met, the client will make the same contributions, or lower, than they would have under the former HCP program. This protection continues to apply even if the client is later reassessed into a higher Support at Home classification, consistent with the no worse off principle. Please refer to our FAQ of this month’s edition, “What fees apply to grandfathered home care recipients?” for more details on transitional and grandfathering provisions.

Contribution and funding

The Support at Home program is funded through a mix of government subsidy and a participant contribution. Under Support at Home, funding is allocated quarterly per participant into accounts administered by Services Australia. Providers can only access this funding by submitting claims after services have been delivered.

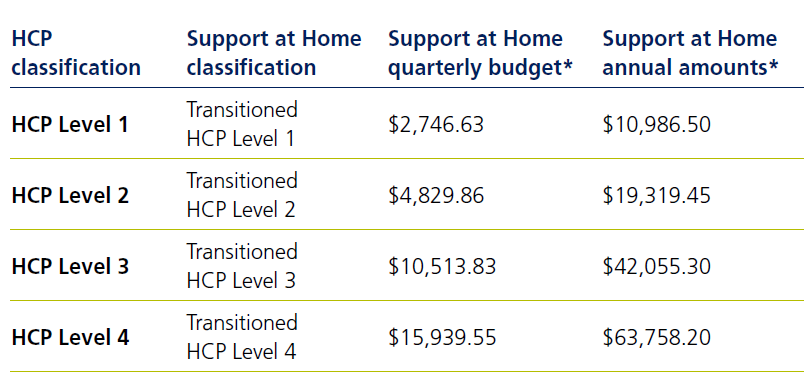

Existing recipients, including those who were in the National Priority System, as at 31 October 2025 were transitioned over to the new Support at Home program on 1 November 2025. Transitioned HCP recipients will continue to receive an equivalent level of funding (including supplements) as their previous HCP. Those who were waiting for an HCP to be allocated to them on 31 October 2025 will also receive an equivalent level of funding to their approved HCP when it becomes available.

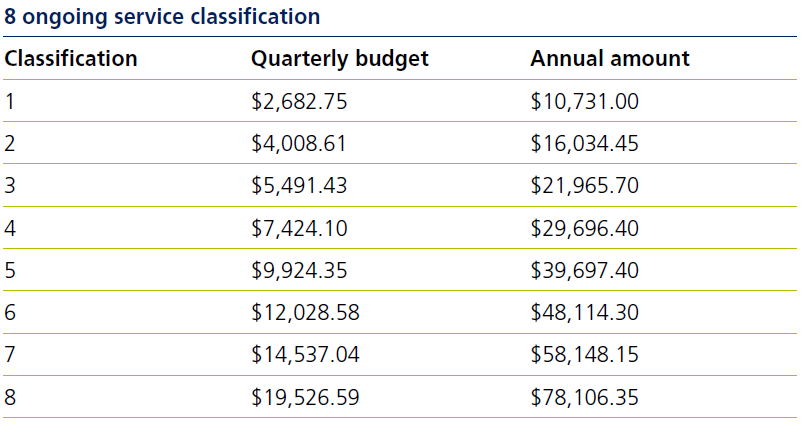

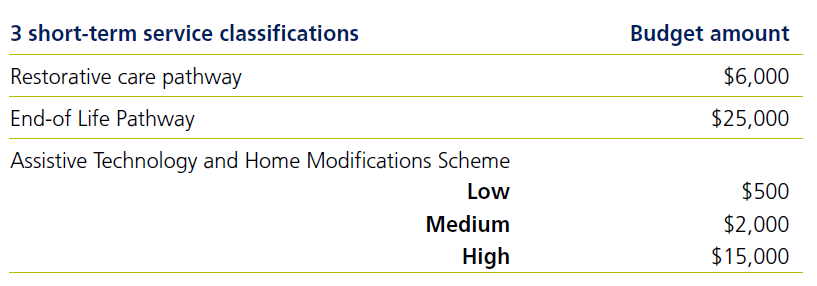

New recipients will have the following eight ongoing service classifications and three short-term service classifications.

10% of the quarterly Support at Home budget for ongoing services will be deducted from each recipient and pooled together in a care management account held by Services Australia. Care management refers to the activities required to plan, coordinate, monitor and review a participant’s home care services so they receive appropriate support in line with their assessed needs. The unspent budget for ongoing services will automatically carry over in the home support account to the next quarterly budget. The carryover amount will be capped at the higher of $1,000 or 10% of the quarterly budget for ongoing services.

Please refer to the Challenger Aged Care Guide for more details and understanding on care management and each of the three short term services.

The Support at Home program is structured around a defined service list, with both services and participant contributions linked to three broad service categories:

- Clinical supports – including nursing care, nutrition, allied health and therapeutic services

- Independence – including personal care, social support and community engagement, therapeutic services to support independent living, transport, respite, assistive technology and home modifications

- Everyday living – including domestic assistance, meals, and home maintenance and repairs.

Home care providers set their own prices for home care services. Providers cannot charge for entry or exit to the service, separate administration fees, travel fees, or claim for these expenses under care management activities. All costs to deliver the service must be included in the price for the service delivered. The Government will set price caps from 1 July 2026.

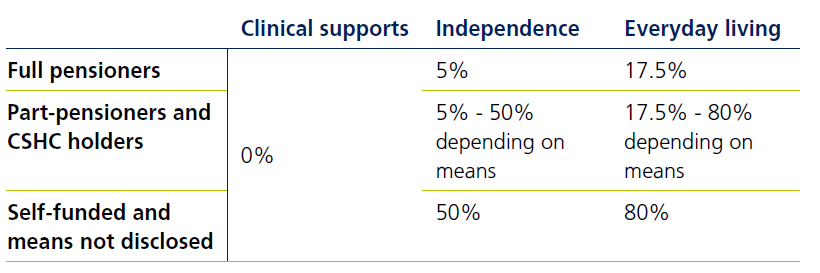

The participant’s contribution under Support at Home will be a percentage of the price for their home care services (subject to an indexed lifetime cap of $137,917.01). Clinical care is fully government funded. The percentage for independence and everyday living services will depend on the pensioner status and means of the participant for part pensioners and Commonwealth Seniors Health Card (CSHC) holders.

Where you have a client whose home care needs are met through a combination of Support at Home and private funding, they can maximise clinical care using Support at Home as the clinical care is fully funded with no participant contribution.

Providers issue monthly statements that outline the funding available, services delivered, contributions made by the participant and remaining funding available for a calendar month period.

Advisers may find it useful to review a copy of the statement provided to the client that shows how expenditure is allocated across the three Support at Home service categories (clinical supports, independence and everyday living). This can assist in identifying how much the client is currently spending in each category.

This information is particularly valuable when assessing the client’s ongoing cash‑flow requirements and when considering whether any investment or funding strategies may be appropriate to meet their home care contribution obligations. Once these details are available, Challenger’s Aged Care Calculator can be used to determine the client’s applicable home care fees and to model projected cash flows for up to 10 years, supporting more informed and proactive advice.

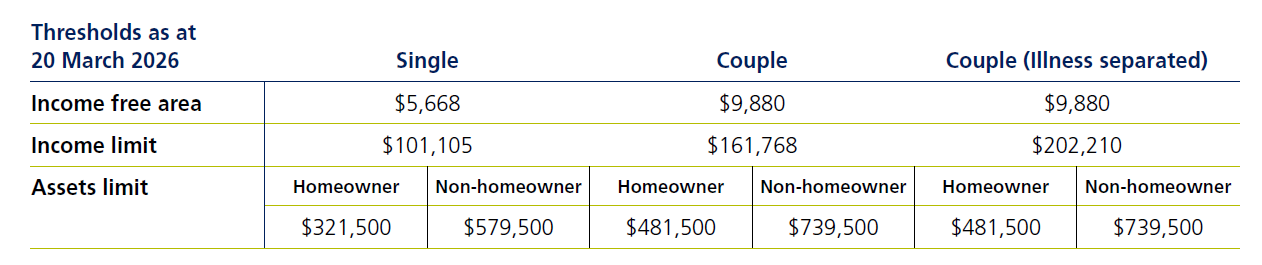

Means testing

Support at Home recipients may have a participant contribution, which will be a percentage of the price for home care services. The percentage will depend on the home care service category and the pensioner status and means of the recipient.

Participant contributions are determined via an assessment of the recipient’s income and assets by Services Australia or DVA. Assessable income and assets for the purposes of participant contributions are the same as those assessed for Centrelink/DVA. If the recipient does not provide their income and assets information to Services Australia/DVA, they are considered ‘means not disclosed’, and their contributions are set at the maximum level.

For part-pensioners and CSHC holders, means testing (both income and assets) applies in order to determine the percentage of participant contribution.

Percentage of participant’s contribution (part-pensioners and CSHC holders) is calculated as follows:

Step 1: Income reduction amount = (annual assessable income - income-free area) x 50% (round to nearest dollar)

Step 2: Assets reduction amount = (assessable assets - assets-free area) x 7.8% (round to nearest dollar)

Step 3: Maximum reduction amount = (income limit - income-free area) x 50% (round to nearest dollar)

Step 4: Input contribution rate = (Greater of Step 1 and Step 2 / Step 3) x 100

Step 5: Percentage contribution

– Independence = Step 4 x 0.45 + 5% (rounding to 2 decimal places)

– Everyday living = Step 4 x 0.625 + 17.5% (rounding to 2 decimal places)

Example:

Dave and Inara are a couple, both age 80 who own their home and have $700,000 in cash and term deposits. They have been approved for Support at Home with an ongoing service classification 6.

Their assessable income and assets for Centrelink/DVA purposes is $20,626 and $700,000 respectively. Their participant contributions are calculated as follows:

Step 1: Work out the income reduction amount

($20,626 – $9,880) x 50% = $5,373

Step 2: Work out the assets reduction amount

($700,000 - $481,500) x 7.8% = $17,043

Step 3: Work out the maximum reduction amount

($161,768 - $9,880) x 50% = $75,944

Step 4: Work out the input contribution rate

(Greater of Step 1 and 2 / Step 3) x 100 = $17,043/$75,944 x 100 = 22.44154

Step 5: Work out the percentage contribution

Independence (Step 4 x 0.45 + 5%) = 22.44154 x 0.45 +5% = 15.10%

Everyday living (Step 4 x 0.625 + 17.5%) = 22.44154 x 0.625 + 17.5% = 31.53%

If Dave and Inara’s home care services are broken down as follows:

- Clinical supports (including 10% care management) of $10,000 p.a. each

- Independence services of $15,000 p.a. each

- Everyday living services of $20,000 p.a. each

They will each pay $0 for clinical supports, 15.10% ($2,265 p.a.) towards the costs of independence services and 31.53% ($6,303 p.a.) towards the costs of everyday living services. This means the government will fully fund their clinical supports, fund $12,735 p.a. toward their independence services and fund $13,694 p.a. towards their everyday living services.

Advice considerations:

Means testing opens up opportunities for clients to strategise through use of asset and income test effective strategies. Given the system is designed to ensure that higher participant contribution applies to people with higher means, strategic advice can play a significant role to not only help reduce the care expense but also maximise their pension entitlements to help improve their cash flow outcomes.

A gifting exemption of $10,000 in each financial year or $30,000 over a 5-year rolling period is allowed from means test assessment. Amount gifted above these thresholds are treated as a deprived asset subject to deeming from the date of gifting. A gifting amount greater than $10,000 can be considered to potentially increase their future Age Pension in 5 years’ time. However, any such considerations to improve their pension entitlement and reduce their care expenses should consider the trade-off of loss of capital, which may have a greater negative effect on their longer-term retirement goals.

Clients can bring-forward certain expenses which they have planned for in future like home renovations, travel, prepaying funeral expenses or purchasing funeral bonds. As the principal home is an exempt asset, a value addition or renovation to their home will also be exempt. Prepaid funeral expenses or buying a burial plot, irrespective of their value, is exempt from assessment. Funeral bond or funeral fund purchases are exempt up to a value of $15,750 (from 1 July 2025) and applies to a client who is single or to each member of a couple as long as both the members have a separate investment.

Allocating a portion of a client’s portfolio to products like Challenger’s Lifetime Annuity (Lifetime Annuity) or Challenger CarePlus (CarePlus) can help optimise your client’s cashflow and can provide a regular income for your clients’ lifetime regardless of how investment markets perform or how long they live. CarePlus is designed for people receiving or planning to receive government subsidised aged care services. CarePlus is comprised of two components - CarePlus Annuity and CarePlus Insurance.

The assets test assessment of the annuity portion of CarePlus is only assessed at 60% of the purchase price until the day they turn age 85, or for a minimum of five years. After this, the assessment further reduces to 30% of the purchase amount for the rest of the person’s life. The income test assessment is assessed at 60% of the annual payment.

Case study 1 – Lifetime Annuity

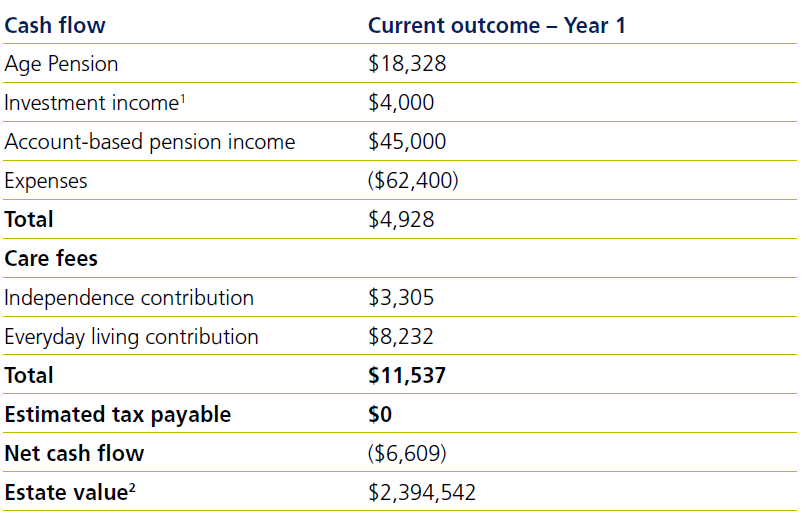

Conan (age 82) and Mora (age 75) are a couple living at home worth $1,500,000 and have $100,000 in cash and term deposits (earning 4% interest p.a.). Mora also has an account-based pension of $750,000. They have living expenses of $1,200 per week. Conan has been approved for Support at Home with an ongoing service classification 6. His service agreement shows the services he plans to access and are categorised as follows:

- Clinical supports (including 10% care management) of $10,000 p.a.

- Independence services of $15,000 p.a.

- Everyday living services of $20,000 p.a.

Conan’s clinical supports are fully funded by the government. However, he will need to contribute 22.03% ($3,305 p.a.) towards the costs of independence services and 41.16% ($8,232 p.a.) towards the costs of everyday living services. Conan and Mora’s current cash-flow - $100,000 invested in term deposits and $750,000 in an account-based pension

Under the current cashflow, Conan and Mora are in a deficit and will be required to draw additional income from their account-based pension in order to meet their cash flow requirements. Given their available level of assets this deficit is likely sustainable.

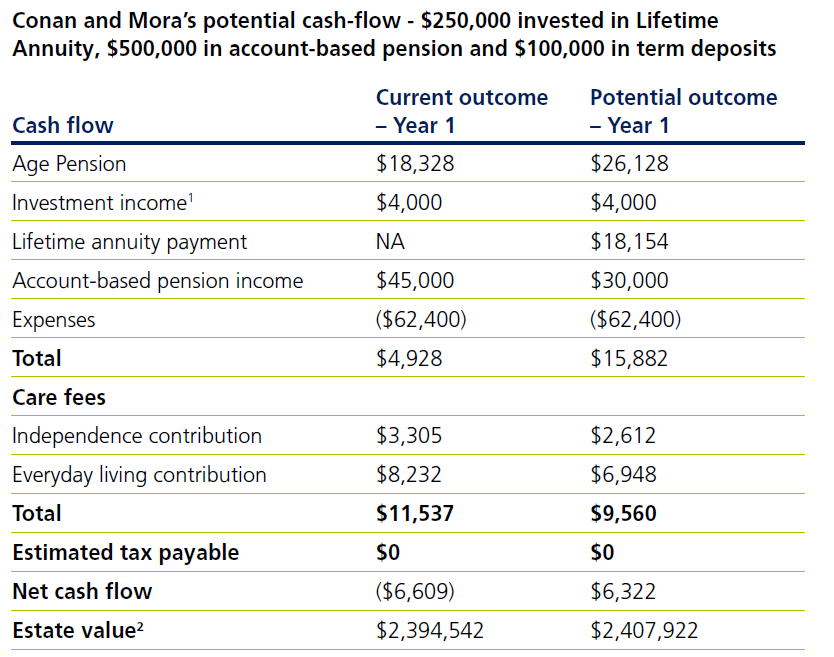

However, this deficit can be improved by reducing Conan and Mora’s assessable assets. A little under 30% allocation to a Lifetime Annuity3 invested for Mora can help improve their cashflow and estate outcomes. With $250,000 allocated from Mora’s account-based pension to a Lifetime Annuity, Conan and Mora’s Age Pension entitlement will increase to $26,128 p.a. and total participant contributions reduce to $9,560 p.a. as a result of the decrease in assessable assets from the concessional assets test assessment of Lifetime Annuity. Conan and Mora’s cash flow will also improve by $12,931 in the first year as compared to having all their savings invested in term deposits and account-based pension. Furthermore, Conan and Mora’s estate will also improve to $2,407,922 at the end of the first year.

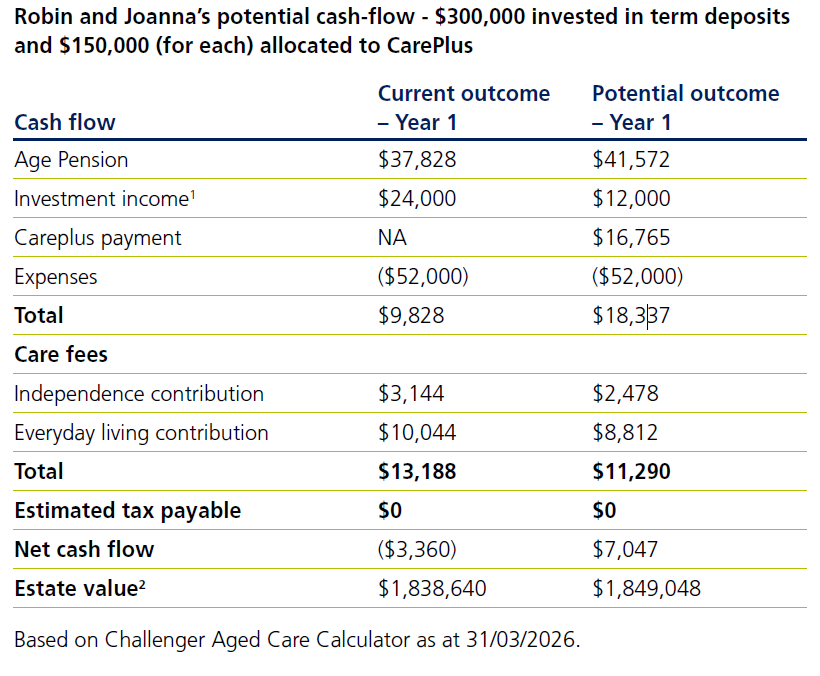

Case study 2 - CarePlus

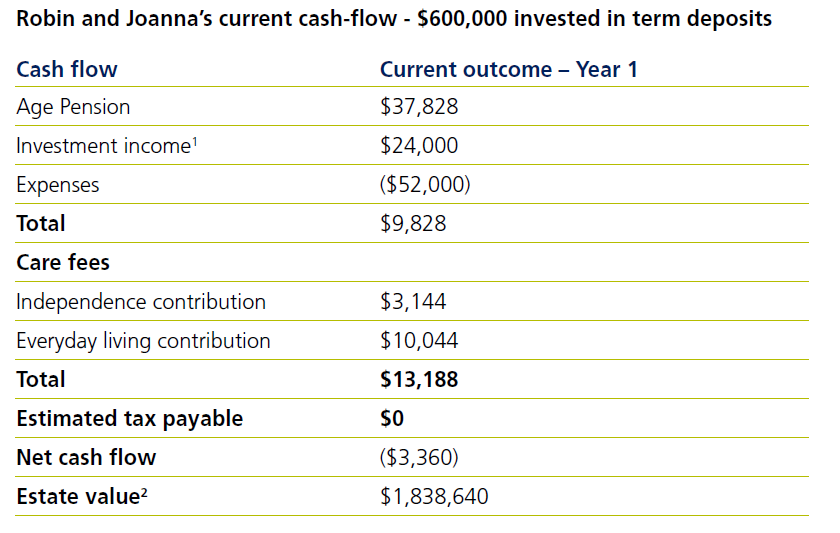

Robin and Joanna are a couple, both age 80 who own their home worth $1,200,000 and have $600,000 in cash and term deposits (earing 4% interest p.a.). They have living expenses of $1,000 per week. They have been approved for Support at Home with an ongoing service classification 6. Their service agreement shows the services they each plan to access and are categorised as follows:

- Clinical supports (including 10% care management) of $10,000 p.a. each

- Independence services of $15,000 p.a. each

- Everyday living services of $20,000 p.a. each

Robin and Joanna will need to contribute 10.48% ($1,572 p.a. each) towards the costs of independence services and 25.11% ($5,022 p.a. each) towards the costs of everyday living services. This means the government will fully fund their clinical supports, fund $13,428 p.a. toward their independence services and fund $14,978 p.a. towards their everyday living services.

If Robin and Joanna invests entirely in cash and term deposits, they will have a cash flow deficit of $3,360 in the first year and their estate will be worth $1,838,640 at the end of the first year. A 25% allocation (each) to CarePlus can help improve their cash flow deficit to a cashflow surplus.

With $150,000 each allocated to CarePlus, Robin and Joanna’s Age Pension entitlement will increase to $41,572 p.a. and total participant contributions will reduce to $11,290 p.a. as a result of the decrease in assessable assets from the concessional assets test assessment of CarePlus. Robin and Joanna’s cash flow will also improve by $10,407 in the first year as compared to having all their savings invested in term deposits. Furthermore, Robin and Joanna’s estate will improve to $1,849,048 at the end of the first year.

1 Term deposit earning 4% p.a.

2 Estate value includes capital growth of 3.5% on the home.

3 The annuity is invested for Mora as Conan cannot invest in a Lifetime Annuity because he has been approved for Support at Home. A Challenger Lifetime Annuity cannot generally be purchased by clients living in a residential aged care facility or if they have a My Aged Care assessment approval that specifies that they are eligible to move into a facility.

Related content

Stay informed

Sign up to our free monthly adviser newsletter, Tech news containing the latest technical articles, economic updates, retirement insights, product news and events.