Is my client grandfathered for residential care?

Is my client grandfathered for residential care?

Download the full article below.

As part of the aged care reforms, there are grandfathering (or legacy) arrangements for residential care and home care. Grandfathering arrangements for residential care are separated into accommodation payments and ongoing costs.

This article explains when clients will be grandfathered for residential care and the various scenarios where grandfathering does or doesn’t apply. References to grandfathered residents throughout the article do not include pre-1 July 2014 residents.

For further information about grandfathering for home care, see April Challenger Tech article “What fees apply to grandfathered home care recipients?”

Grandfathering for accommodation payments and ongoing costs

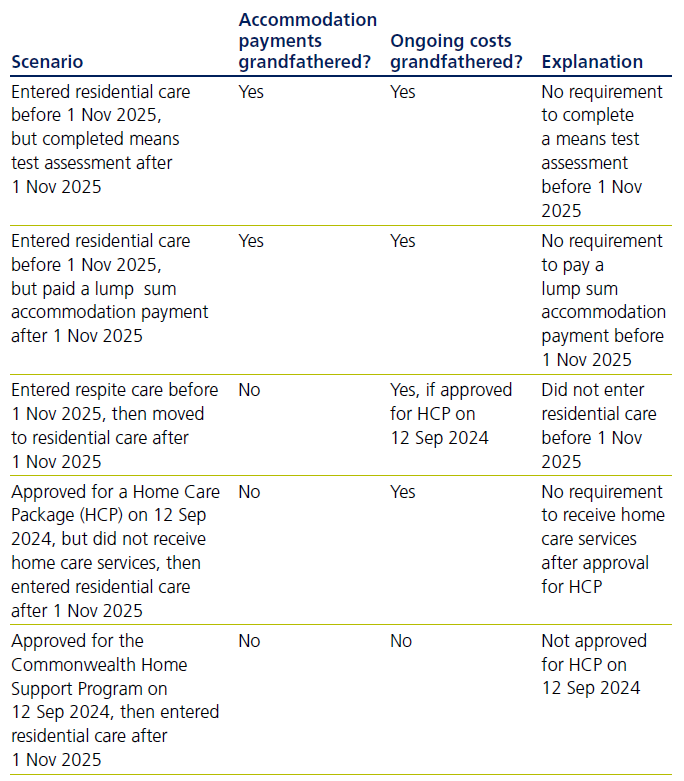

Individuals who entered residential care before 1 November 2025 will be grandfathered for accommodation payments and ongoing costs. Individuals who entered respite care or residential care through a multi-purpose service before 1 November 2025 will not be grandfathered unless they were approved for a Home Care Package on 12 September 2024 (see below).

Individuals who entered residential care before 1 November 2025 but were on a break from care on 1 November 2025 will be grandfathered for accommodation payments and ongoing costs if the break period was less than 28 days. Approved leave including hospital leave, social leave and emergency leave does not count towards the break period.

Individuals who were approved for a Home Care Package on 12 September 2024 and enter residential care on or after 1 November 2025 will be grandfathered for ongoing costs but not for accommodation payments (partially grandfathered). Individuals who were approved for the Commonwealth Home Support Program and not a Home Care Package on 12 September 2024 will not be partially grandfathered if they enter residential care on or after 1 November 2025.

Residents who are grandfathered for accommodation payments will not be subject to retention amounts or DAP indexation. Residents who are grandfathered for ongoing costs will be subject to the means-tested care fee instead of the hotelling contribution and non-clinical care contribution.

For further information about retention amounts, DAP indexation, the hotelling contribution and non-clinical care contribution, see Challenger Tech Aged Care Guide.

Will the following residents lose grandfathering?

Losing grandfathering for accommodation payments and ongoing costs

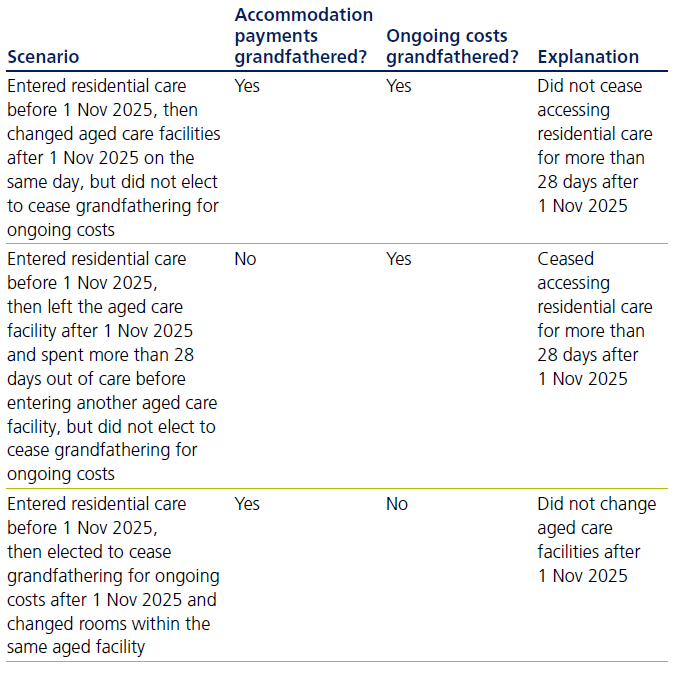

Grandfathered residents who cease accessing residential care for more than 28 days after 1 November 2025 will lose grandfathering for accommodation payments. Grandfathered residents can elect to cease grandfathering for ongoing costs at any time after 1 November 2025, however they cannot elect to cease grandfathering for accommodation payments.

Grandfathered residents who elect to cease grandfathering for ongoing costs and change aged care facilities after 1 November 2025 will lose grandfathering for accommodation payments.

Will the following residents lose grandfathering?

Case study - Not grandfathered v partially grandfathered

For clients who enter residential care on or after 1 November 2025, it is important to check if they were approved for a Home Care Package on 12 September 2024 and partially grandfathered.

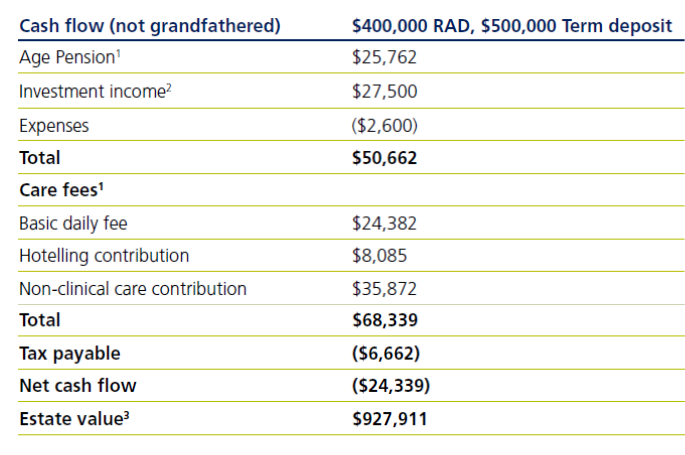

Susan is single, 85 years old, non-homeowner and has been approved for residential care. She was not previously approved for a Home Care Package on 12 September 2024. Her chosen aged care facility has an advertised accommodation price of

$400,000. She has $900,000 invested in term deposits, $50,000 in her bank account and $10,000 of personal assets.

Susan pays $400,000 as a refundable accommodation deposit (RAD) and keeps $500,000 invested in term deposits and $50,000 in her bank account. She will have $50 per week of other expenses while she is in residential care. What will be her cash flow and estate value in the first year?

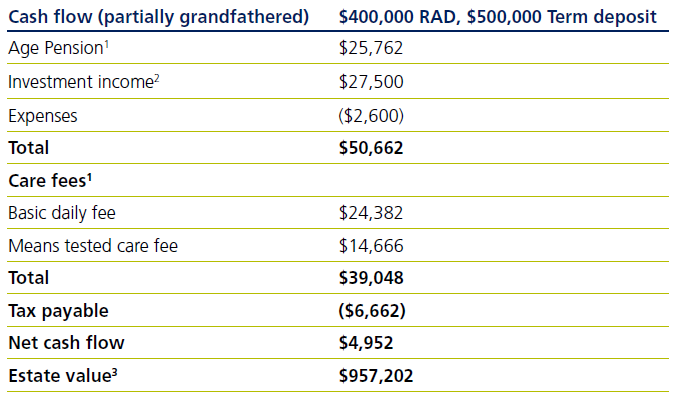

Susan will have a cash flow deficit of $24,339 in the first year and her estate value will be $927,911. What if Susan was previously approved for a Home Care Package on 12 September 2024 and partially grandfathered for residential care?

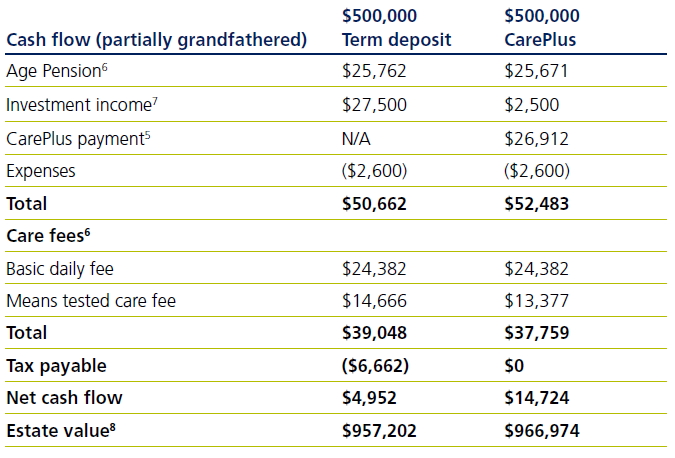

Susan’s cash flow would improve by $29,291 and she would have a surplus of $4,952 in the first year. This would also be reflected in her estate value which would increase to $957,202.

Effectiveness of Challenger CarePlus for grandfathered clients

Challenger CarePlus (CarePlus) is a combined lifetime annuity (CarePlus Annuity) and life insurance policy (CarePlus Insurance) which can be purchased by clients who receive or plan to receive Government subsidised aged care services. CarePlus Annuity provides guaranteed regular payments for life and CarePlus Insurance provides a guaranteed death benefit, up to 100% of the amount invested, payable to nominated beneficiaries or the estate in the event of the client’s death4.

CarePlus works effectively with Centrelink and aged care means testing to reduce assessable assets. 60% of the CarePlus Annuity purchase price is assessed until age 85 (with a minimum of 5 years) and then 30% is assessed thereafter. If the client is Age Pension age or over at the time of investment, the greater of the CarePlus Insurance premium and surrender value is assessed.

CarePlus works effectively with tax to reduce assessable income. CarePlus Annuity receives a deductible amount which reduces assessable income from the regular payments. The deductible amount is calculated as the CarePlus Annuity purchase price divided by the client’s life expectancy at the time of investment.

Susan invests $500,000 in CarePlus with $50,000 remaining in her bank account. CarePlus will make regular payments of $26,912 per annum5 and pay a death benefit of $500,000.

Susan’s cash flow will increase by $9,772 and she will have a surplus of $14,724 in the first year. This will also be reflected in her estate value which will increase to $966,974.

For further information about the effectiveness of CarePlus for clients who are not grandfathered, see November 2025 Challenger Tech article “Effectiveness of CarePlus from 1 November 2025”.

1Centrelink and aged care rates and thresholds as at 20 March 2026

2 Term deposit and bank account assumed interest rate of 5%

3 Retention amount of 2% deducted before the RAD is refunded to the estate

4 Stamp duty (1.5% of CarePlus Insurance premium) will be deducted from the death benefit for SA residents

5 Challenger Aged Care Calculator 01/06/2026, 85 year old female, NSW resident, nil adviser fees

The information in this article is current as at 1 June 2026 unless otherwise specified and is provided by Challenger Life Company Limited ABN 44 072 486 938, AFSL 234670 (Challenger, our, we), the issuer of the Challenger annuities (Annuity(ies)), the issuer of CarePlus Annuity and CarePlus Insurance, together referred to as Challenger CarePlus and Challenger Retirement and Investment Services Limited ABN 80 115 534 453, AFSL 295642 (CRISL). The information in this article is general information and is intended solely for licensed financial advisers or authorised representatives of licensed financial advisers, and is provided to them on a confidential basis. It is not intended to constitute financial product advice. This information must not be distributed, delivered, disclosed or otherwise disseminated to any investor, without our express prior approval. Investors should consider the applicable Annuity Target Market Determination (TMD) and Product Disclosure Statement (PDS) available at challenger.com.au and the appropriateness of the applicable product to their circumstances before making an investment decision. This information has been prepared without taking into account any person’s objectives, financial situation or needs. Neither Challenger and/or CRISL, nor any of its officers or employees, are a registered tax agent or a registered tax (financial) adviser under the Tax Agent Services Act 2009 (Cth) and none of them is licensed or authorised to provide tax or social security advice. Before acting, we strongly recommend that prospective investors obtain financial product advice, as well as taxation and applicable social security advice, from qualified professional advisers who are able to take into account the investor’s individual circumstances. Each person should, therefore, consider its appropriateness having regard to these matters and the information in the TMD and PDS for the applicable Annuity before deciding whether to acquire or continue to hold the product. A copy of the TMD and PDS is available at challenger.com.au or by contacting our Adviser Services Team on 13 35 66. Any examples shown in this article are for illustrative purposes only and are not a prediction or guarantee of any particular outcome. Age Pension benefits described in this article will not apply to all individuals. Age Pension outcomes depend on an individual (or couple’s) personal circumstances and may change over time. This article may include statements of opinion, forward looking statements, forecasts or predictions based on current expectations about future events and results. Actual results may be materially different from those shown. This is because outcomes reflect the assumptions made and may be affected by known or unknown risks and uncertainties that are not able to be presently identified. Challenger and CRISL relied on publicly available information and sources believed to be reliable, however, the information has not been independently verified by Challenger and CRISL. While due care and attention has been exercised in the preparation of this information, Challenger and CRISL gives no representation or warranty (express or implied) as to its accuracy, completeness or reliability. The information presented in this article is not intended to be a complete statement or summary of the matters to which reference is made in this article. To the maximum extent permissible under law, neither Challenger, CRISL, nor its related entities, nor any of their directors, employees or agents, accept any liability for any loss or damage in connection with the use of or reliance on all or part of, or any omission inadequacy or inaccuracy in, the information in this article.

Related content

Stay informed

Sign up to our free monthly adviser newsletter, Tech news containing the latest technical articles, economic updates, retirement insights, product news and events.