With Australia’s CPI increasing by 7.8% over the year to December 2022 there has been a wave of forecasts that the peak of inflation is now behind us. The implication is that we can now relax, and normal markets can resume. The truth is that investors, and particularly retired super fund members are not likely to relax, nor should they.

The biggest inflation spike in 40 years has sent a shock through investment markets around the world. 2022 was the first time in nearly three decades when both equities and bond investments lost money. There has been a collective sigh of relief with signs that the December numbers will be the peak in inflation.

However, whether 7.8% is the peak is not the question that will matter most to the members of a super fund. The critical question is what inflation is going to be in the coming years, and how they manage the risks around adverse scenarios. If inflation stayed at 7.8% p.a. it would take less than 10 years for the value of a retiree’s income to halve. If it falls back to, say, 2.5% p.a. the 28 years it would take to halve the real value of a retiree’s income would be manageable. The risk is that is doesn’t fall back as far, or as quickly, as markets are hoping. Averaging 5% p.a. will cut the half-life period to 14 years and will be problematic for investors trying to generate income that keeps up with the cost of living

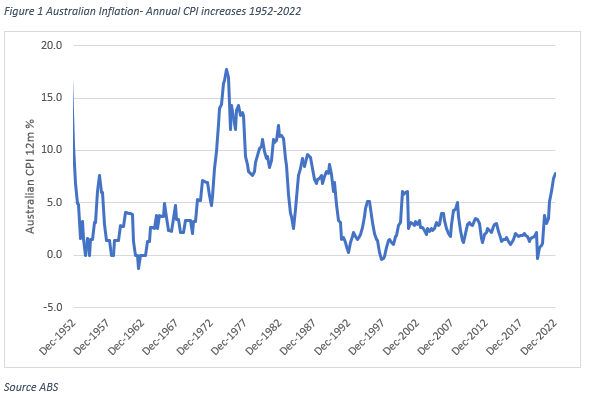

It would be great if we were certain that inflation would quickly return to the low-inflation environment of the past 30 years. However, we can’t be certain and historically it hasn’t usually been quick, as the figure shows. RBA Governor Phil Lowe recently declined the opportunity to provide a forecast to parliament of when low inflation would be restored.1 If the head of the RBA doesn’t know when it will happen how can anyone be confident in their expectations.

Retirees will suffer from an extended period of higher inflation, but they don’t need to accurately predict the path of inflation to mange the risk. If the inflation spike proves to be transitory than long-term investments, such as a typical growth portfolio should provide similar real returns to history and there is nothing else to do. However, if inflation takes time to come back down, the damage to a retiree’s lifestyle from inflation can be dramatic. The gap between nominal and indexed government bonds is currently 2.33% p.a. (3.30%- 0.97%) suggest that markets are expecting a quick return to low inflation.2 Markets are not priced for inflation to take any time to return to the low settings of recent history. If it does take time, markets are likely to react adversely.

To protect their lifestyle, retirees need a plan in case the benign forecasts are not realised. Thankfully, they don’t need to predict future movements in inflation and interest rates exactly. What they need to do is have (at least some of) their savings protected from inflation. There are several ways this can be done:

- Investments with a direct link to inflation such as CPI-indexed bonds

- Investments with an indirect link to inflation, such as infrastructure or property where the underlying income stream increases with inflation

- Income streams, such as defined benefit pensions or CPI-linked lifetime annuities, where the payments to a retiree are explicitly linked to inflation outcomes.

The Age Pension is automatically increased to inflation to preserve the quality of living for older Australians. Many members expect that their super will enable them to enjoy a lifestyle that is better than what the Age Pension offers. To preserve this benefit, the payments from super in retirement need to be able to keep up with inflation. With inflation a leading concern for retirees, members in a fund that provide an option to manage inflation are well-placed to potentially manage their inflation worries. For a generation of people who started their careers in the high inflation, rising unemployment of the 1970s, the lived experience emphasises these risks. Taking the ‘She’ll be right mate’ approach that markets are currently assuming won’t be much comfort for those who know the pain inflation can inflict.